The market is now pricing in a cut to the Overnight Cash Rate (OCR) from 0.25% for the RBA’s October 6th meeting, with potential to change other policy measures as well.

Let’s take a look why.

The Australian Economy and Monetary Policy

RBA Deputy Governor Guy Debelle spoke on 22 September regarding the above topic, and started off rosily, showing how Australia has outperformed many other developed nations during 2020.

However, towards the end of the speech Dr. Debelle addressed “options for monetary policy”, where he stated outright:

“Given the outlook for inflation and employment is not consistent with the Bank’s objectives over the period ahead, the Board continues to assess other policy options.”

Option 1 – Additional QE

One such option mentioned is to buy bonds through quantitative easing further along the yield curve, supplementing the existing three-year target.

At present the RBA targets the 3-year government bond yield at 0.25%, in-line with the current RBA target overnight cash rate of 0.25%.

However, in practice, the RBA has also bought state government bonds and slightly longer dated government bonds (4 and 5y) to achieve their target of 0.25% yields on 3y govies.

The RBA is thus proposing buying even longer government bonds as well, possibly out towards 7-10 years.

Option 2 – FX Rate Intervention

Another option mentioned was direct foreign exchange-rate intervention.

Our Australian dollar is largely influenced by exports and imports, with the greater emphasis on exports given our abundance of natural resources.

As such, a higher AUD versus other currencies results in less export volumes, as weaker foreign currencies relative to a higher AUD buy less Australian goods.

By directly selling AUD to lower our currency’s value, the RBA would be making Australian exports more competitive.

Moreover, a higher AUD is also deflationary as it lowers the absolute price paid for certain goods and services in the Consumer Price Index basket.

i.e. if our AUD has risen relative to foreign currencies, when we buy a t-shirt from Amazon in the USA, the price will be lower in AUD terms. This lower price on goods and services is measured as a deflation in CPI figures.

Dr. Debelle was quick to say this would not be a prime option, as the AUD is “broadly aligned with its fundamentals,” so selling AUD in the open market may not be an effective policy option.

Option 3 – Lowering the Overnight Cash Rate but staying above zero%

The current RBA Overnight Cash Rate target (OCR) is 0.25%, while the Exchange Settlement Account (ESA) rate that bank deposits receive at the RBA is 0.10%.

Debelle gave little detail, but the OCR or the ESA rate can be both lowered further.

i.e. the OCR can be cut to 0.10% and the ESA rate to 0.05%, there is no fixed formula or ratio of what these rates need to be relative to each other.

Option 4 – Negative Interest Rates

The last option given was for a negative OCR.

Dr. Debelle reiterated similar comments to Governor Lowe’s past comments that negative interest rates have little emphasis of efficacy, and would likely encourage more savings as households seek to preserve the value of their savings, by saving more.

Market Reaction

The market’s reaction was that the RBA Board will likely cut the cash rate (option 3) and add additional QE (option 1), on 6 October when they next meet.

Specifically, the market is pricing in the RBA to

- cut the OCR from 0.25% to 0.10%

- lower the 3y government bond target from 0.25% to 0.10%

- lower the rate of the Term Funding Facility from 0.25% to 0.10%

Lastly, and open to more interpretation, the market is pricing the ESA rate will drop from 0.10 to 0.01-0.05% range, providing a significant incentive to buy bonds or lend to the private sector, rather than hold cash at bank.

Before we go further, we need to be clear, the cash rate cut will likely only be 0.1 to 0.15%, which does not move the needle in the grand scheme of home lending and loan growth.

Banks will unlikely move their lending rates much, if at all.

The effects will be felt in other areas of the economy and financial markets.

Implications – Bond Yields

Dr. Debelle’s speech prompted both Westpac and NAB economists to amend interest rate forecasts downwards, prompting bonds to rally and yields to lower.

For instance, our 10-year benchmark government bond got to 0.80%, the lowest level since April, in the depths of COVID amid safe-haven demand.

Shorter duration bonds such as those 3-years to maturity fell 4bp, below the RBA’s current target of 0.25% to 0.20%.

If new government bond yield targets are enacted in the next RBA meeting, we’ll likely see bond yields fall further.

Implications – AUD

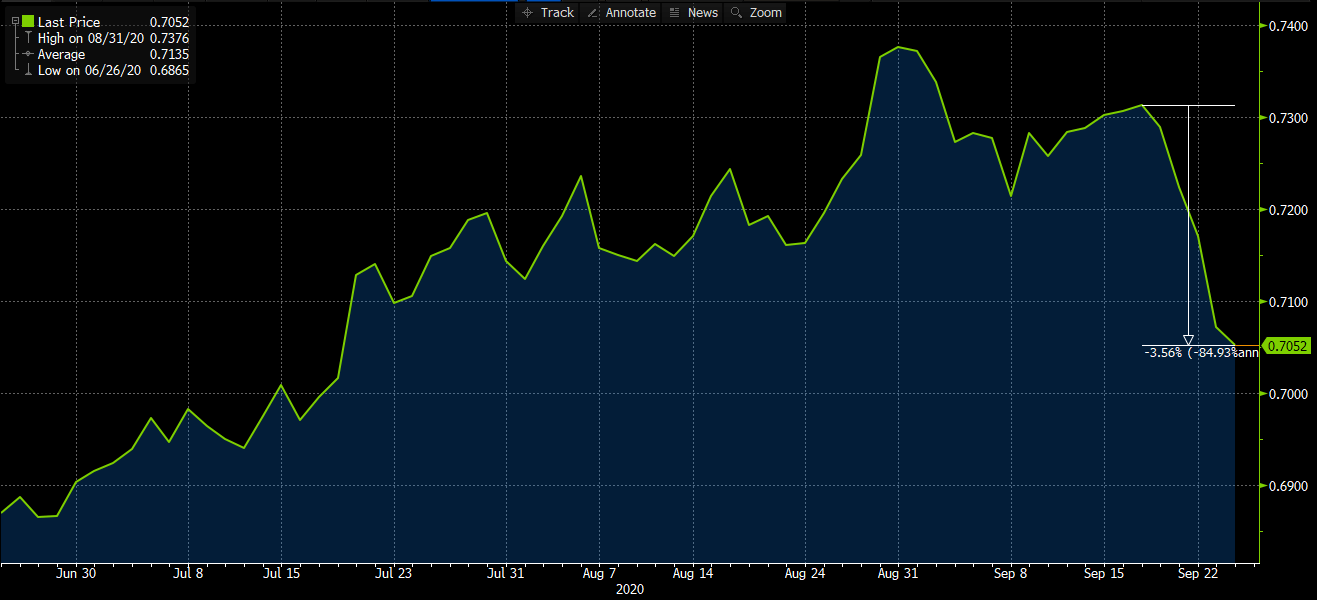

Guy Debelle’s speech along with NAB and Westpac rate cut forecasts prompted our AUD to sell-off against the USD and other currencies, graphic of AUD/USD below.

In AUD/USD case, the result was a 3.5% fall in the currency pair over 2 days.

Further dovish comments from the RBA may elicit further selloffs in our AUD, as well as a RBA Board decision on 6 October that is larger than the market expects – as outlined above.

Alternatively, if the RBA does not enact these changes in their October meeting, we may see a rally in the currency and a sell-off in the bond market due to the change in expectations, though the market will likely look through the result for the Board to make the changes in November.

Source: Bloomberg

Implications – Government Debt

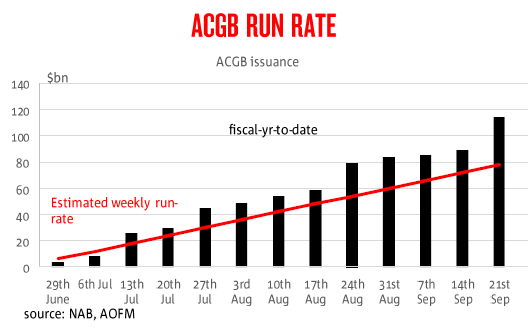

Taking into account the latest bond syndication last week, the Australian government has issued a total 114.5bln AUD of debt since July 1st, more than 40% through their total funding required of 240bln announced for the financial year.

i.e. AOFM is 48% through their target, 3 months into the year

This could be interpreted that AOFM will slow down in government debt issuance, or that there’s potential for this amount to grow further from 240bln to a higher total required.

It should be noted that these changes to bond yields do not materially change the debt servicing costs of the Commonwealth government, though this is decreasing slowly as existing debt matures and new debt is issued at lower rates.

Overall, interest expenses are going up because the volume of debt being issued is greater than the reduction in market interest rates – though we await the next Budget to see the Treasury’s figures.

Closing remarks

In their totality, the changes in interest rate forecasts will put slight downward pressure on yields, though minimal. We’re talking about a cash rate move from 0.25% to 0.10%, which is small in the grand scheme of our cash rate at 1.50% in May last year.

Likely this won’t change any large asset allocation decisions either, though some may take profit from the rally in fixed-rate bonds in sympathy to the news.

However, the noise associated will have consequences for our FX market and the competitiveness of Australian export businesses.

Cynically, I admit that the RBA may have already achieved part of their goal – as the AUD is now lower against other currencies, without having to make any formal policy decisions.

Lastly, I’m looking past the next 1-2 months where the Board will likely make some form of policy change to a period 2-3 years from now, as the current enaction of policy measures will be difficult to unwind. This all speaks to the RBA forecasting a lower for longer interest rate policy setting, where economic growth is sluggish, and unemployment remains elevated.

Given this macro-economic picture, bonds remain a defensive element to portfolios despite the lower overall yields – as real yields (adjusted for inflation) may prove to be higher than expected.

Equities will remain the growth allocation and valuation calculations may have room to go higher/further.

The views expressed in this article are the views of the stated author as at the date published and are subject to change based on markets and other conditions. Past performance is not a reliable indicator of future performance. Mason Stevens is only providing general advice in providing this information. You should consider this information, along with all your other investments and strategies when assessing the appropriateness of the information to your individual circumstances. Mason Stevens and its associates and their respective directors and other staff each declare that they may hold interests in securities and/or earn fees or other benefits from transactions arising as a result of information contained in this article.