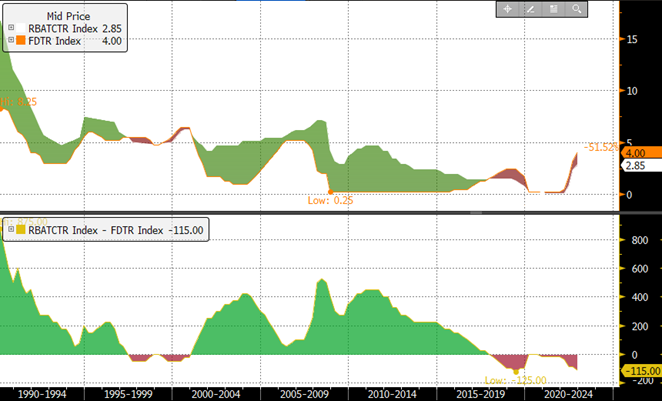

In the last 30 years, Aussie interest rates have often been higher than US rates. Looking at the chart below, for the lion’s share of that time the Aussie 11am Cash Rate was significantly higher than the US Fed Funds rate. History suggests that it is when the US is hiking that Australia has lower cash rates and conversely Australia seems slow to ease compared to the US Central Bank. During this hiking cycle Australian rates have been persistently lower than the US Fed Funds rate.

Figure 1: AUD 11am Rate (RBACTR) v US Fed Funds Target Rate (FDTR) and spread since 1990

Source Bloomberg

For much of that time a key aim of monetary policy was defending the AUD against the multiplier effect of a lower currency in inflation of imported goods. In recent years Australia has run a trade surplus rather than the heavy deficits of those earlier times so currency defence has been less in evidence. On a trade weighted basis our currency has looked relatively stable through the Covid and post- pandemic era. As there is less focus on currency effect, the RBA can focus on other factors.

One key reason for Australian rates tending not to rise as fast as US is that most of the financing in Australia is done on a floating rate basis and the majority of the US is done as fixed rate. The speed that the rate changes affects disposable income or free cashflow is much quicker when interest bills are adjusted on a monthly or quarterly basis. Although this is well understood the market will often “overprice” the yield for Australian bonds relative to their US counterparts.

Despite fears that Australian interest rates must be higher than the US in order to protect the currency and have an appropriate risk premium, it is clear that the RBA is aware of the key differences in the effectiveness of their policy actions relative to the Fed. The markets have also come to understand this, underpinned by a strong current account surplus that is shielding Australia from the currency impacts that have affected Europe and the UK amongst others. There the high USD pushed commodities that are priced in USD even higher on a domestic basis. The risk premium that used to apply to Australian Bond yields is dissipating.

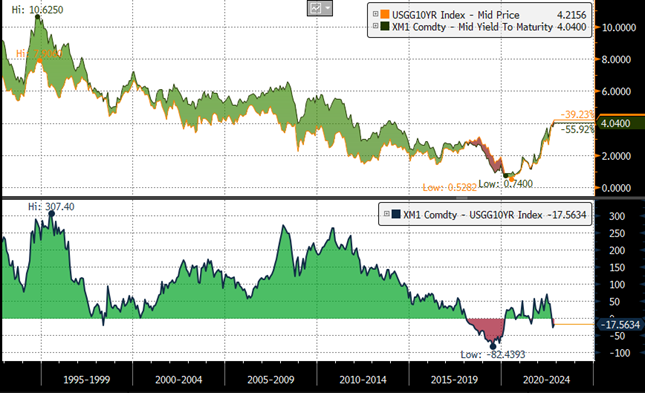

Bond markets set pricing based on expectations that are anchored by the current rate. The steepness of either a positive or negatively shaped yield curve reflects the market’s expectation of the future path of interest rates. Figure 2 shows that in recent years Aussie bond yields have remained lower than US bond yields. This cycle is unusual because in hiking cycles historically Aussie yields had been higher than US yields.

Figure 2 – Australian 10 Year Bond Yields Vs US 10 Year Bond Yields 1992-2022

Source Bloomberg

The cost of borrowing in Australia is having an effect on confidence as well as current spending. There is a sense that market pricing is nearing the terminal rate needed to get inflation back in the target band. The need for even higher rates is an open question but leading indicators suggest the effect of the increases is having the desired effect and bond yields may be near their peak. For this reason building duration exposure in AUD now has a profile that does not require rates to go lower to achieve an acceptable return but will benefit if they do.

As the US hiking cycle is not yet at an end it is difficult to buy into the US bond market at current levels. There is no doubt the Fed is indicating that pricing in the market needs to adjust to a higher terminal rate and potentially a longer pause before the need to cut rates to avoid choking the economy. Markets have reacted to the most recent Fed hike and statements from the FOMC Chair Jay Powell by taking USD rates higher in expectation of the need for rates to stay high for longer.

Notwithstanding this continuation of the cycle, it is clear that once an easing expectation comes into markets there will be more room for US Bonds rates to reverse than there has been for 15 years. The desired outcome of tightening is to reduce demand and that will mean Fed funds will have to drop. When markets come to that point we expect to see the US Bond yields to drop more than the Australian curve. As the economy approaches that point there will be excellent opportunities to add US duration as an outright allocation with an inverse correlation to an economic slowdown with a yield double the Fed’s inflation target for the first time since 2007.

The views expressed in this article are the views of the stated author as at the date published and are subject to change based on markets and other conditions. Past performance is not a reliable indicator of future performance. Mason Stevens is only providing general advice in providing this information. You should consider this information, along with all your other investments and strategies when assessing the appropriateness of the information to your individual circumstances. Mason Stevens and its associates and their respective directors and other staff each declare that they may hold interests in securities and/or earn fees or other benefits from transactions arising as a result of information contained in this article.