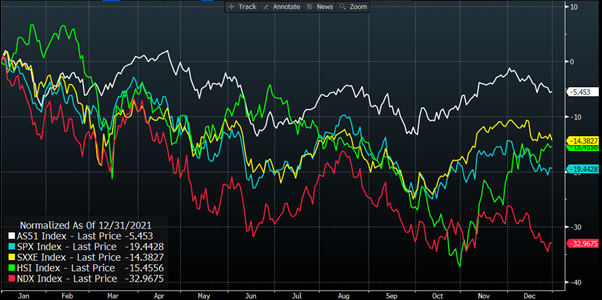

2022 started with some major equity indices near their all-time highs and the vast majority of central banks entertaining record low interest rates. However, over the past 12 months, we have seen the geopolitical and economic landscape significantly change. Geopolitical issues have come to the fore with the Russia-Ukraine war, inflation has ramped up over the course of the year, the UK has had a tumultuous time with politics and China has modified its Covid-19 policy and is allowing the economy to re-open. All of these factors have contributed to the major global indices finishing the year weaker. The Nasdaq fall (32.97%), the S&P 500 fall (19.44%), the STOXX 600 fall (14.38%), the Hang Seng fall (15.46%) and the ASX200 finish the best out of those indices but still down (5.45%).

Walkthrough of year

Russia-Ukraine

Inflation was a growing theme at the start of the year, these inflation concerns were then exacerbated by Russia invading Ukraine in late February. When Russia invaded the Ukraine questions around global supply chains and logistics came to the fore. The invasion heaped pressure onto the oil and natural gas supply chains given both nations contribute to the energy market, and it also put pressure on soft commodity supply like wheat.

Inflation & Central Banks

The effect of the Russia-Ukraine war was seen quickly with energy and food prices surging, bringing inflation into the spotlight across global economies, which raised questions on how economies would cope. Energy and food prices were large drivers of inflation early on and energy has continued to be a key metric in the inflation prints, however they weren’t the only drivers as shelter inflation ramped up as well.

Central banks across the globe slowly began to change their tune off the back of the impacts of the war as inflation began to get out of control and where quantitative easing (QE – the purchasing of securities from the open market to reduce interest rates and increase the money supply) was in place, this was removed. We then saw central banks begin to raise interest rates as they looked to tame inflation.

Over the remainder of the year we saw central banks ramp up the speed at which they hiked rates as they realised the magnitude of the task, leaving many people to witness some of the fastest rate rising cycles in their lifetimes. This put significant pressure on financial markets and consumer confidence decreased as recession fears grew. This led to equities spiralling downward through to the end of June before recovering a little after financial year end as the market started to believe there was a larger chance to avoid recession than previously mentioned. This view was relatively short lived as the Federal Reserve Bank (The Fed) lifted expectations for interest rates and became more aggressive with their voice in the public as they became very focused on returning to their target band for inflation, no matter the cost for households.

UK & their politics

The UK had their fair share of inflationary concerns throughout the year; however, this wasn’t the only talking point. At the beginning of September Boris Johnson’s resignation was effective and this saw Liz Truss become the second PM for the year. Later in September UK assets fell sharply off the back of a controversial UK mini-budget announcement which went against party consensus on managing the economy by containing unfunded tax cuts on top of the energy price plan announced earlier in the month. This mini budget resulted in the Bank of England stepping in to try and calm markets as well as PM Liz Truss removing her chancellor and replacing him with Jeremey Hunt who quickly reversed the decisions made by his predecessor. Not long after this, PM Liz Truss was under further pressure before she finally resigned leaving her as the shortest serving UK PM in history.

China

China’s reopening post the pandemic (or lack of) has been well documented and put companies listed on the Hang Seng under significant stress over the course of the year. Sentiment was incredibly bearish as concerns mounted around the impact further lockdowns would have on the economy. This led to the Hang Seng being the worst performing major index at the end of October (down ~37%). Then came November and things changed drastically.

News headlines began to circulate that China was going to shift away from its strict covid-zero policy and move to a more dynamic policy that enabled the reopening. A lot of these headlines were unsubstantiated with Beijing often releasing statements to counter these headlines, however the market didn’t want to believe Beijing – instead believing that “where there’s smoke, there’s fire” and that we would see this shift away from Covid-zero. This saw a significant recovery in the Hang Seng with it rallying ~35% of the October low.

Outlook for 2023

The new year is beginning with concerns of a looming recession hovering over many global economies as central banks continue to tighten monetary policy into a global downturn meaning there could be further downward pressure ahead early in the year for equities.

The flip to this is that so far we’ve seen the labour market and corporate earnings remain surprisingly resilient despite the shift in the economic environment, meaning if central banks are able to tame inflation without triggering significant economic stress, then equities could have some positivity ahead.

The views expressed in this article are the views of the stated author as at the date published and are subject to change based on markets and other conditions. Past performance is not a reliable indicator of future performance. Mason Stevens is only providing general advice in providing this information. You should consider this information, along with all your other investments and strategies when assessing the appropriateness of the information to your individual circumstances. Mason Stevens and its associates and their respective directors and other staff each declare that they may hold interests in securities and/or earn fees or other benefits from transactions arising as a result of information contained in this article.