Global markets are currently stuck in an almighty game of tug of war, with many market participants holding disparate outlooks in the face of rising economic uncertainty, multi-decade high inflation prints, and the impending tightening of monetary policy from developed market central banks.

This topsy-turvy nature of equity markets should come as no surprise as investors battle with the ever-present concern of the detrimental effects of rising inflationary environments.

There’s currently no shortage of headlines around the future actions of central banks, with many stakeholders continually increasing their forecasts on rate hike timelines over the next 2 years.

As a result of high inflation, many have begun to question how the imminent central bank rate hikes will affect consumer spending sentiment.

Banks will always draw the eyes of investors upon earnings results as they are uniquely positioned to provide perspectives on both the domestic and global economic backdrop.

Many other companies can shed light on supply and demand or consumer sentiment within their industry. However, banks are unique in this thanks to their ability to discuss consumer and business sentiment across the market. They can do because they are money centres giving them insight into demand for borrowing.

Not only do they provide the above, they also provide a scope of what lays ahead in the earnings season as they are at the heart of economic activity.

In today’s note we will summarise what we learned from the banks’ earnings season.

What did we learn this earnings season?

Once the dust settled and markets were able to look at the results of banks more broadly, two key themes emerged: strength in consumer banking deposits as well as growth in credit and debit spending.

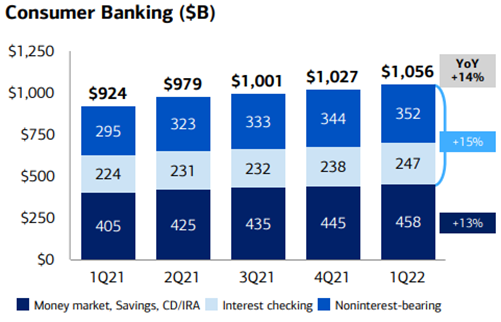

Consumer banking deposits showed positive momentum as the upward trend in average deposits continued. The below chart from the Bank of America highlights this.

Source: Bank of America 1Q22 Earnings Presentation

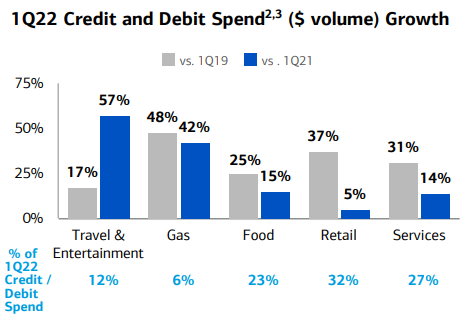

Credit and debit spending were also positive across the banks.

Wells Fargo & Co (WFC:NYS) reported an increase in credit card revenue of 6% YoY. JP Morgan Chase & Co (JPM:NYS) echoed this with their results as they reported an increase of 21% where we saw really strong credit card spending in both travel and dining, albeit not a huge surprise as we continue to peel back Covid-19 restrictions. Bank of America (BAC:NYS) continued the theme citing an increase in credit card spending of 15% YoY.

The below chart shows the improved credit and debit spending for the Bank of America for 1Q22 compared to both 1Q19 and 1Q21.

Source: Bank of America 1Q22 Earnings Presentation

The higher credit and debit spending along with increasing consumer banking deposits signals that sentiment is still positive despite inflation headwinds.

Shifting our gaze across toward business spending, looking at the Morgan Stanley Business Conditions Index (MSBCI) is a good place to start. The MSBCI is a monthly survey which acts as an economic barometer, it measures general analyst sentiment over an array of components.

Last month’s survey came in at 44 which indicates spending was in contraction (a score of 0-50 indicates contraction, 50-100 indicates expansion). While this doesn’t necessarily look great, when we look at it more closely and drill down into the components inside the survey, we are able to see that there was positive momentum for capital expenditure across businesses as well as increased hiring plans.

Wells Fargo & Co saw their commercial business remain positive with middle market banking revenue up 8% YoY as a result of higher deposits and loan balances.

So, what is the outlook ahead?

JP Morgan remains optimistic for the economy in the short term as consumer and business balance sheets, as well as consumer spending are all remaining at healthy levels.

Looking further ahead; Jamie Dimon – CEO of JP Morgan, sees significant headwinds due to the challenges associated with geopolitical and economic challenges due to high inflation, supply chain issues and the war in Ukraine.

Citi (C:NYS) reiterated this view on a call they held last week where they discussed the US banks. They stressed that the path ahead was full of uncertainty as a direct consequence of the continuing geopolitical issues surrounding the war in the Ukraine as well as the uncertainty relating to the timeline of the Fed rate hikes.

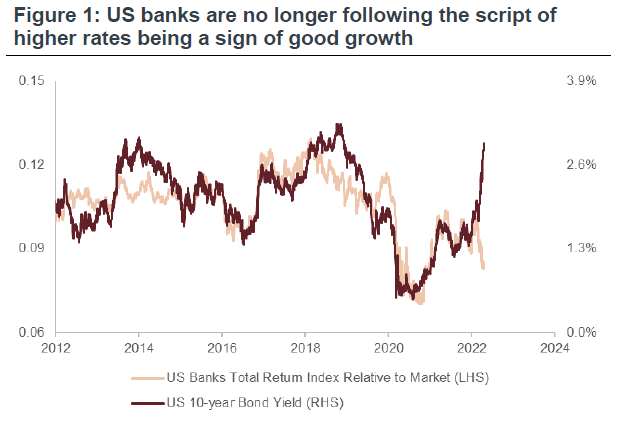

Historically bank performance has been positively correlated with bond yields as investors have viewed inflation and higher rates as positives for economic growth and bank earnings. In the past few weeks and months, we have seen yields rise sharply, however banks have underperformed casting doubt over the short-term future on how to play banks.

The below chart from Barrenjoey shows how the path of US Banks total return index relative to the market has diverged from its historical pattern with respect to the US 10-year bond yield.

Source: Bloomberg, Barrenjoey Research estimates

From an investment perspective the concerns around the war in the Ukraine were particularly emphasised, as JP Morgan analyst Mislav Matejak pointed out that investors wanted to avoid banks with material legal entity and higher levels of lending exposure to Russia, with Citi being named as one of the names with the largest exposure there.

Citi’s view on investing was to stick to names with strong balance sheets with a particular liking for Wells Fargo & Co (WFC:NYS) as well as Morgan Stanley (MS:NYS). This is reiterated by JP Morgan with their buy ratings on the likes of Morgan Stanley (MS:NYS) and Bank of America (BAC:NYS)

If you’re looking for wider exposure to the sector then the BetaShares Global Banks ETF (BNKS:AXW) or the iShares U.S. Financial ETF (IYF:ARC) could be of interest as it invests in many of the names mentioned above.

The views expressed in this article are the views of the stated author as at the date published and are subject to change based on markets and other conditions. Past performance is not a reliable indicator of future performance. Mason Stevens is only providing general advice in providing this information. You should consider this information, along with all your other investments and strategies when assessing the appropriateness of the information to your individual circumstances. Mason Stevens and its associates and their respective directors and other staff each declare that they may hold interests in securities and/or earn fees or other benefits from transactions arising as a result of information contained in this article.