As someone born in the 1980s, I’m classified as a Millennial and share the common complaint among 30-40 years old’s that domestic property in Sydney within 30-45 minutes of Sydney CBD is highly unaffordable, where it’s nigh impossible to save enough money to keep up with the rate of growth of Sydney property prices when cash accounts yield such low returns.

This has seen many of us move along the risk curve, out of cash accounts and the “safe” compounding they used to provide, requiring return above and beyond investment grade fixed income as well.

I.e. if property is appreciating 8%+ per annum, then 0-1% in cash or 2-4% in fixed income doesn’t quite fit the brief, and there’s only so much of your income you’re able to save.

A strategy that I’m fond of is what I call the “Housing Basis Trade”, where we invest a portion of our housing deposit savings into domestic and/or global property markets, where our objective is to keep up and hopefully outperform the returns of the local property market.

Where for example, if Sydney or Melbourne property prices rise by 15 or 20% in 2021 and a further 10% in 2022, hopefully, our investment will have a similar or better return.

This has the pro/con that if domestic property prices fall – while not expected, is possible – the investment will show a relative result as well.

This is why the theoretical approach still maintains a suitable cash balance that will retain its value if property prices fall, balanced by the capital growth approach of the property beta.

We can implement this strategy several ways:

- Invest in passive strategies that seek to replicate our housing indices

- Identify geographies of the domestic market that may outperform the area we’re looking to buy

- Identify types of property that may outperform the area we’re looking to buy

- Identify fund managers with skill or “edge”, who can outperform the area we’re looking to buy

- Or a combination of the above

In regards to today’s note, I wish to focus on the second and fourth strategies for implementation, where actively managed international property exposure may provide positive basis above and beyond domestic.

International Property

It’s largely beyond doubt by now that Australians allocate a portion (or most) of their investable capital to property, where the lion’s share of this allocation is to domestic property.

This makes sense for a lot of investors because they know the local market best (the term is “home bias”), the regulation and taxation, and can physically inspect the properties as well.

From a theoretical standpoint, Australia’s property market is a small part of the global property market (less than 3%), and as such, investors should have some exposure to global markets as well.

According to ATO data from FY 2019/2020, Australian superannuation accounts had on average ~10% exposure to domestic real estate, and less than 0.1% exposure to international real estate.

This goes to show that there’s a wide universe out there, that many are not utilising.

Investment Thesis

The economic disruption associated with social distancing will continue to subside over the coming months and years, as economies re-open and we return to some form of social and economic normality (pre-COVID normality).

Already in Australia we’re seeing travel restrictions lifted that allow for international transit, something that’s been in place for some other nations for months already.

This is happening whilst government stimulus is still on-going for the majority of the developed world, and while central banks are continuing to provide liquidity and maintain historically low borrowing costs.

In aggregate, these are the fundamentals that allow for increased international market participation, as well as asymmetric opportunities because of the winners-losers of the COVID-19 pandemic.

Technology and Social Change

In our morning missives of late we’ve focused on technological adaptations that are empowering investors, consumers and businesses, creating “disruption” within industries.

COVID-19 sped up an already existing trend, where these cohorts have further embraced technology in quick fashion, using scale to enhance their utility.

In practice we’re seeing this create return differentials between retail, office, logistics, transport, data centres, life science, health and storage property prices, where the nature of retail and office specifically has changed since the pandemic.

Moreover, storage and logistics has become vogue areas of investment, where we’re seeing tailwinds emerge that will see these areas outperform in years to come.

Inflation Protection

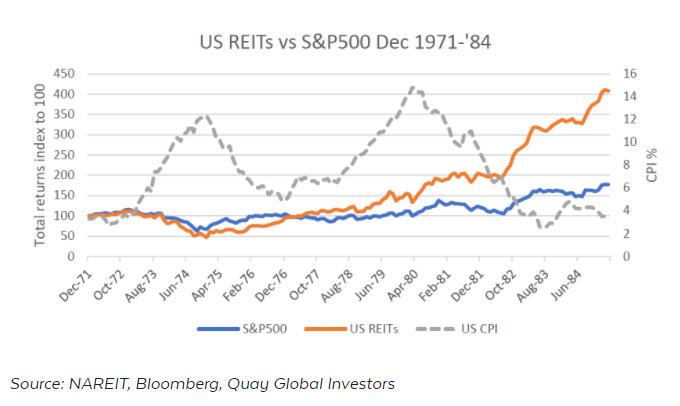

I’m a personal fan of the analysis of Chris Bedingfield at Quay Global Investors’, where Chris has written several articles this year about the outperformance of global property during periods of high inflation, and cites the following chart from the 70s and 80s:

In a recent missive published in August, the Quay team detail global property’s reaction to rising inflationary pressures, where even moderate inflation will drive up the replacement cost and residual value of a global property investment.

Moreover, while a disinflationary environment (CPI less than 2% p.a.) can be beneficial for equities over property, a higher inflation impulse sees property outperform.

This is entirely relevant to the Housing Basis Trade, where increases in goods and services pricing (inflation) will erode the purchasing power of our cash balances, where we hope the property related investment will maintain and hopefully increase its value in real (ex-ante) terms.

Avenues for Investment

There are multiple options available to an investor seeking to replicate the Housing Basis Trade.

The strategy I personally prefer – that only takes into account my risk appetite and objectives and is by no means advice for your own portfolio – is to outsource the investment management of the global property exposure to sophisticated fund managers with intimate knowledge, experience, information and access to opportunities I do not personally have.

Much like how investors outsource the management of their fixed income investment to my team at Mason Stevens, we can do the same for property as well.

As already mentioned, the Quay Global Real Estate Fund is available (APIR: BFL0020AU) at a low minimum investment, that seeks to provide total return of CPI +5% p.a. (as at 30-Sep-2021).

Quay’s strategy has identified areas within the US, Canadian, UK and EU property markets that can potentially outperform our domestic property market.

A somewhat similar but also different international property fund is the Resolution Global Property Securities Fund (APIR: WHT0015AU), which seeks to outperform the FTSE EPRA/NA REIT Index. Given this target return objective, we can be reasonably assured the fund will have a high correlation with global property prices, where ResCap have repeatedly outperformed this benchmark.

Also within the active and managed fund space is the AMP Capital Global Property Securities Fund (APIR: AMP0974AU), which like ResCap targets to provide gross return above the FTSE EPRA/NA REIT Index, which it has managed to do over nearly every time period back to its inception in 2007.

On the passive side of things, we have both the VanEck FTSE International Property (Hedged) ETF (ASX: REIT) and the SPDR Dow Jones Global Real Estate ETF (ASX: DJRE).

VanEck’s REIT provides a replication of the FTSE EPRA/NA REIT Index and a much lower management cost than the managed fund listed above.

SPDR’s DJRE seeks to replicate the Dow Jones Global Real Estate Securities Index, that while similar, has some differences.

Closing Remarks

If we bypass the home bias that many of us exhibit, there’s certainly opportunities in global real estate markets that can add value to portfolios, and potentially provide returns above and beyond domestic real estate.

Investors can enjoy the diversification aspects compared to international equities, as well as avoid the correlation that the ASX exhibits to the domestic REIT market.

In terms of the Housing Basis Trade, there’s many strategies that can be implemented that can be utilised to keep up with the stellar domestic property market, where investors can gain access at a far lower minimum investment via ETFs and managed funds.

The views expressed in this article are the views of the stated author as at the date published and are subject to change based on markets and other conditions. Past performance is not a reliable indicator of future performance. Mason Stevens is only providing general advice in providing this information. You should consider this information, along with all your other investments and strategies when assessing the appropriateness of the information to your individual circumstances. Mason Stevens and its associates and their respective directors and other staff each declare that they may hold interests in securities and/or earn fees or other benefits from transactions arising as a result of information contained in this article.