Welcome to the first day of freedom for NSW residents – where today marks one of the first steps for our largest state’s return to normality.

In lieu of this, lets discuss a segment of the re-opening trade – specifically regarding those companies concerned with domestic and international travel.

The domestic and international travel sector will be the last to recover from the COVID-19 pandemic – owing to government restrictions and societal fears of contracting COVID-19.

When looking at the biggest players within these spaces, a trend is clear –the largest companies are those within the “sharing” economy.

Both Airbnb (NASDAQ: ABNB) and Uber (NYSE: UBER) have revolutionised their respective industries with their unique business models, decentralising the provision of services from companies to individuals.

The sharing economy has come as somewhat of a revelation, where individuals are able to temporarily or permanently earn extra income through utilising their vehicles and homes, creating more robust and intertemporal balances between supply and demand.

For Airbnb, they have been able to build out the new industry of alternative accommodation, where consumers have greater selection and personalisation, and (usually) at cheaper prices compared to more traditional business models.

Uber on the other hand has drastically changed the trajectory of the transport industry, through their provision of efficient, convenient and cheap mobility products – spanning personal transportation, food delivery and now freight.

Both stocks offer unique exposures within the entire re-opening thematic – where they have the potential to deliver significant long-term growth prospects as the sharing economy continues to expand, as well as benefitting from the short term pick up in revenues as our levels of mobility increase both within and between countries.

As the first of a series of “re-opening” notes we will cover this week, today we will take a look at international exposures to the travel industry, through the lens of two sharing economy giants – Airbnb and Uber.

Airbnb – The Ultimate Travel Stock

When it comes to the re-opening trade, Airbnb sits within the sweet spot of being in the midst of a growth phase which should continue to reap rewards into the long term, as well as being exposed to the short term pick up in revenues as governments around the world loosen domestic and international travel restrictions.

It has a strong and easily understandable investment narrative, which carries significant importance in today’s markets – where it is one of the primary drivers of the sharing economy and is responsible for disrupting the hotel industry.

Within their accommodation product line, their business model is simple, and with minimal overheads compared to the traditional accommodation businesses.

They take between 14-16% of each booking, but don’t have to provide the majority of the services performed by motels and hotels, and instead only have to provide a marketplace connecting homeowners and travellers, customer service and insurance.

Whilst they haven’t been able to deliver a profit over a sustained period, Airbnb have sought to prioritise fostering a strong community of hosts and enhancing brand awareness through marketing campaigns.

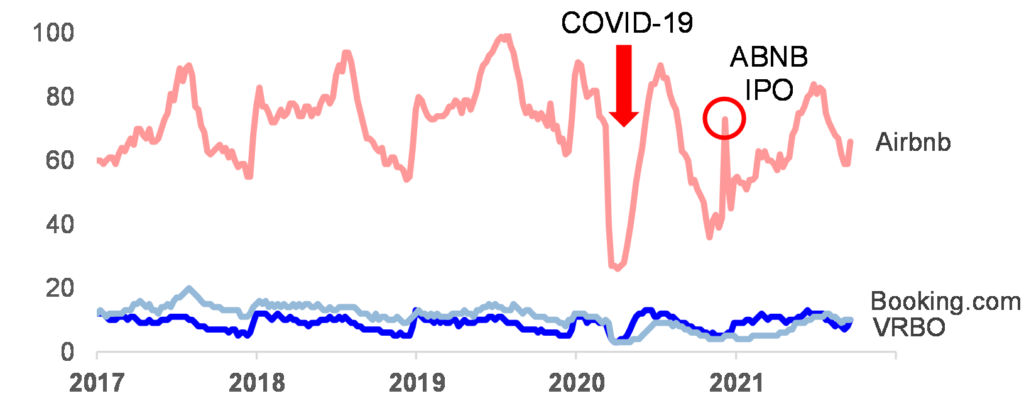

This has paid off – reflected through their market dominance within the alternative accommodation industry, where Airbnb is able to receive significantly more web traffic than its main rivals, Booking.com (NASDAQ: BKNG) and VRBO (NASDAQ: EXPE).

Google Trends – Searches for Airbnb, Booking.com and VRBO

Source: JP Morgan

When looking at Airbnb’s current market capitalisation of just over USD$105billion, it might seem a little expensive when considering this is greater than both Hilton (NYSE: HLT) and Marriot (NASDAQ: MAR) combined.

Source: Bloomberg

However, when you take a step back and consider that Airbnb’s total addressable market is USD$3.4 trillion (JP Morgan 2021) – where if Airbnb can make up 1% of this figure, this would equate to $34billion in annual revenue.

If you use Airbnb’s most recent adjusted EBITDA margin of 16% and put a decent multiple on it – it doesn’t seem that expensive.

Moreover, in their Q2 earnings report, Airbnb surprised to the upside, reporting quarterly revenue of USD$1.3bn, which was up 299% YoY, and 10% higher than Q2 2019 levels.

In the near term, Airbnb’s financial performance should continue to improve, as restrictions are removed and societal attitudes towards travel normalise, with there being minimal threat of competition given Airbnb’s unrivalled brand awareness in the space, and the higher number of potential homes available.

Its long-term prospects will be driven by the extent to which the accommodation industry transitions from more traditional means, to new alternative options – something which will be increasingly more likely as people look to avoid the confined and potentially infectious walls of densely populated hotels.

However, the most likely factor to scupper the Airbnb growth story is regulation, where it currently sits within the grey area of short-term rental accommodation – with inconsistent and ambiguous laws and regulations which could potentially change on a whim.

Cities like New York have banned rentals within shared buildings for less than 30 days, however the enforcement of such regulation is often dependent on complaints from neighbours.

Moreover, other cities have imposed caps on the number of days per year an Airbnb can be operated, like the Greater Sydney area where unhosted listings are limited to 180 days per year.

As housing affordability becomes more of a pressing societal issue, the imposition of greater restrictions on metropolitan listings could hurt Airbnb’s bottom line and will serve as its greatest existential threat.

Uber – Driver Supply Issues, But Growing Profitability

Uber’s ridesharing model has transformed the transportation industry, spawning new means of mobility across personal transport, food delivery and freight.

As economies re-open and people gain greater confidence in travelling more frequently, ride sharing applications will continue to increase revenues as pent-up consumer demand is released.

Within Uber’s most recently released CYQ3 guidance and CYQ4 outlook, it was revealed that the company was profitable in both July and August and will reach EBITDA breakeven for Q3.

This run of profitability came as somewhat of a surprise to the market, given the critical evaluations which investors have always had regarding the inability of Uber to turn a profit in the past.

This came off the back of continued margin expansion, and growth in bookings – particularly within the mobility product line.

Assisting this growth was the introduction of Uber Pass – which is a paid subscription that offers users discounts on rides and delivery, accounting for 25% of gross bookings within the delivery segment in Q2.

Source: Bloomberg

Much like Airbnb, Uber has gone through a phase of extensive marketing outlay, in order to build its customer base and develop greater brand awareness.

Through now having a more extensive product ecosystem – where it is able to offer personal transportation, food/grocery delivery and freight, customer retention is able to occur at a greater rate, where each customer also spends more money on the app.

This ecosystem should continue to grow in the coming years, as Uber moves towards developing a “super app” much like Grab’s, where it could also offer banking services.

However, Uber still has its problems, with driver supply issues in recent months in the US impacting its bottom line – with many drivers opting not to return to the app after months of lockdowns – a situation which is likely to also occur in Australia and other countries yet to fully re-open..

Moreover, regulatory burdens have and will continue to impact Uber as regulators attempt to ascertain whether Uber drivers are contractors, or employees.

The distinction is important, as if Uber drivers are to be classified as employees, they would be entitled to minimum wages, annual leave, pension/superannuation entitlements and much more.

The classification of Uber drivers as employees in March of this year in London will cost Uber an estimated total of US$500m, and with Uber’s win in California’s Prop 22 being deemed unconstitutional, further pain would be incurred should a similar outcome to London occur in California.

Sharing is Caring

The sharing economy is poised to benefit from broader economic re-opening, as people have greater mobility and more positive attitudes towards travel domestically and internationally.

As with most innovations, the sharing/gig economy will be impacted by regulatory overhand, as policymakers try to understand the best way to manage these developing markets.

However, as an international exposure to the travel and mobility industry – both Airbnb and Uber offer exposure to the short-term benefits from economic re-opening, as well as long term growth prospects.

In the coming years, their fates will be determined by the extent of regulation, as well as the inclination of consumers to move away from traditional products.

If they fall on the right side of regulation, they might even end up making consistent profits – however we will have to wait and see whether this ends up occurring.

The views expressed in this article are the views of the stated author as at the date published and are subject to change based on markets and other conditions. Past performance is not a reliable indicator of future performance. Mason Stevens is only providing general advice in providing this information. You should consider this information, along with all your other investments and strategies when assessing the appropriateness of the information to your individual circumstances. Mason Stevens and its associates and their respective directors and other staff each declare that they may hold interests in securities and/or earn fees or other benefits from transactions arising as a result of information contained in this article.