It’s been only two months since we last wrote about the RBA, though the outlook for Australian rate markets could not look any more different.

Tuesday’s shock announcement underscored what can be viewed as a pivotal turning point in the mentality and approach of the RBA, where the RBA has now transitioned into “inflation-fighting mode” – seeking to “front load” rate hikes and chart out a more aggressive path to neutral interest rates.

This shift in thinking came with the intention to unwind pandemic over stimulation, as well as to contain faster than expected inflation, particularly so in the last month, with rising energy costs, continued supply chain disruptions from the Russia/Ukraine war, and higher commodity prices to blame.

“Higher prices for electricity and gas and recent increases in petrol prices mean that, in the near term, inflation is likely to be higher than was expected a month ago.”

– Governor Phillip Lowe

Importantly, this upside surprise came in advance of any definitive data reaffirming this view – a far cry from the RBA who had continually cited the importance of seeing both inflation sustainably within the 2-3% bracket, and evidence of commensurate wages growth before shifting their policy path.

Whilst Tuesday’s hike could just signal an acceleration of future hiking plans, where we likely see a lower terminal rate as inflation is contained sooner (with a potential for a pause in September/October) – it necessitates a paradigm shift in the way we view the intentions and methodologies of the RBA in achieving their mandates.

As a result, we must carefully review the short, but albeit impactful statement released by the RBA, in order to understand how future meetings may play out.

“Patient” A Thing of the Past

The RBA’s patient and measured approach to the setting of interest rates is now but a distant memory – where it’s focus has shifted towards regaining credibility and highlighting to the market that it is serious about returning inflation within the target band of 2-3% by 2024.

In order to achieve this objective, they’ve shifted a reactive approach, waiting for data prints and providing forward guidance on any future material moves in interest rate trajectories, to a more proactive, forecast approach based on a range of data points, but also their view on inflation and the labour market.

Important to this shift has been the RBA’s view that the Australian economy is resilient, and that labour markets are strong and capable of withstanding more aggressive rate hike timelines.

“The Australian economy is resilient, growing by 0.8 per cent in the March quarter and 3.3 per cent over the year. Household and business balance sheets are generally in good shape, an upswing in business investment is underway and there is a large pipeline of construction work to be completed.”

“The labour market is also strong. Employment has grown significantly, and the unemployment rate is 3.9 per cent, which is the lowest rate in almost 50 years.”

–Governor Phillip Lowe

Whilst the impetus of the inflationary impulse falls largely outside of the Australian economy (where the Australian yield curve will be unable to materially influence global energy and commodity prices and supply chain disruptions), it follows the same path of many of our G10 peers who have sought to control inflation through a monetary policy-imposed destruction of demand.

What wasn’t mentioned within the monetary policy announcement was the importance of our AUD to the RBA – given its first mandate is to maintain “the stability of the currency of Australia”.

A more protracted period of a slow, but steady approach to rate hikes, would’ve seen further widening of interest rate differentials, and a greater impact on households through imported inflation (where domestic input costs are already growing) – adding to the inflationary impulse at the consumer level over the short-medium term, and justifying in part the need to react to the actions of other central banks.

New Year, New RBA?

Now that we know the change in attitude for the RBA, we can look forward to future meetings with a renewed perspective on what the terminal interest rate is, and how quickly the RBA will seek to get there.

The RBA have yet to reveal any specific plans, though they did claim that they would continue to do “what is necessary to ensure inflation in Australia returns to target over time”.

This means that we will likely see another rate hike of between 40-50bps in the coming meetings, or at least, a continuation of 25bp rate hikes until we either see one, or a combination of the following:

- Signs of receding inflation, both domestically and globally

- Rising unemployment, or a lack of wage growth as reflected through WPI or the RBA’s business liaison program

- A material decline in household consumption

What Are Markets Saying?

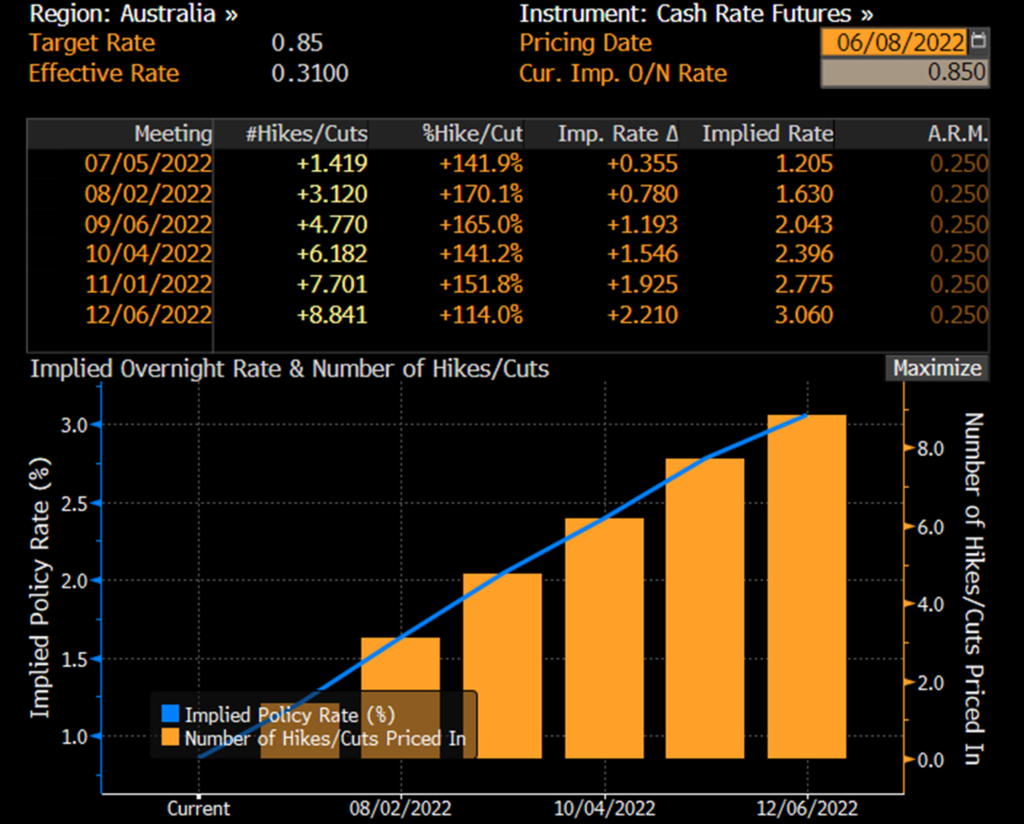

Whilst most economists and sell-side firms see rates reaching between a range of 1.8%-2.1% by year-end, and for terminal rates to end up slightly higher than this, markets are pricing a much more aggressive path for the RBA.

Futures markets see the RBA reaching a policy rate of 3.06% by year-end – equating to an additional 2.21% in hikes, or just under 9, 25bp hikes in the remaining 6 meetings.

Source: Bloomberg, as at 8/6/22

Moreover, futures pricing sees an expected policy rate of 4.01% by September 2023 – a scantly believable concept given where we are now, and the macroeconomic picture ahead.

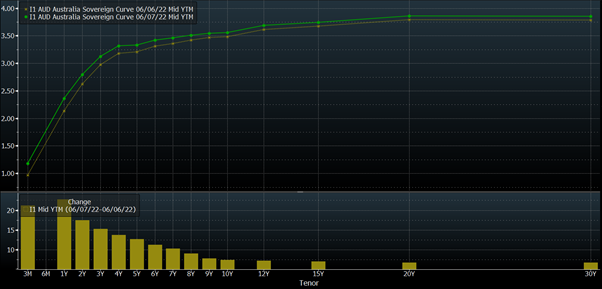

When we look to yield curves, we saw repricing throughout the curve on Tuesday, with all tenors rising between 7-22bps – with the majority of the move occurring in the front end.

Chart 1: Australian Yield Curve on 6/6/22 (yellow) and 7/6/22 (green)

Source: Bloomberg, as at 8/6/22

Whilst reaching such yields may seem unlikely for now, upcoming data releases will tell the tale on the steepness of interest rate hike timelines, where this will likely be determined by the decision on minimum wages (1 July), Q2 CPI (27 July), and Q2 WPI (17 August).

If the RBA is right, and inflation tends towards its forecast of a 2-3% range next year, it reduces the need for the RBA to reach the terminal rate of ~3.7% forecast by the market and will see a shift in yields downwards.

As has been the case over the past few months, investors must apply extra caution when taking on interest rate duration within their portfolios – where volatility will remain within the capital prices of fixed-rate bonds (primarily within the longer end) for some time to come.

The views expressed in this article are the views of the stated author as at the date published and are subject to change based on markets and other conditions. Past performance is not a reliable indicator of future performance. Mason Stevens is only providing general advice in providing this information. You should consider this information, along with all your other investments and strategies when assessing the appropriateness of the information to your individual circumstances. Mason Stevens and its associates and their respective directors and other staff each declare that they may hold interests in securities and/or earn fees or other benefits from transactions arising as a result of information contained in this article.