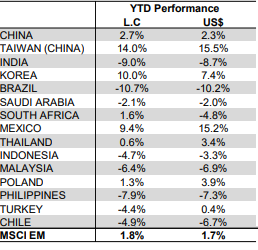

When compared to other Equity Emerging Markets, India’s absolute and relative returns have stalled since late November 2022 as global investors have moved back into Technology focused markets such as Korea and Taiwan post-China’s step change in their Covid zero policy (see Fig 1).

Fig 1: Emerging Market YTD performance through to the end of March 2023

Looking back in time, 1991 was an important year for India when the economy was liberalised post the balance of payments crisis. Economic growth had averaged roughly 4% in the three decades prior to 1991 and has averaged roughly 6% since.[1] India can often be viewed by outsiders as being chaotic and risky, but underneath the surface there is a steady passage of reforms in progress. Morgan Stanley has estimated that over the next decade, India will become the world’s third largest economy. With a forecast annual growth rate of 6.5%, its GDP is forecast to double over the next 10 years from US$3.4 trillion to US$8.5 trillion.

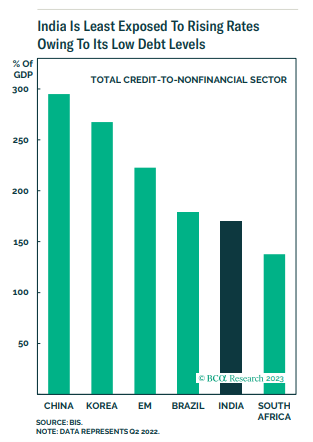

Although like most economies globally, GDP growth in India may come under some pressure in 2023. However India does have less of an exposure to the global rate cycle due to two reasons:

- Restrained debt levels when compared to other Emerging Markets which have private sectors which are heavily leveraged. See Figure 2.

- Slowing trade will prove to be a headwind for export dependent markets. India has lower dependence on goods exports when comparted to many other emerging markets.

Figure 2: India has lower exposure to rising rates, when compared to other Emerging Markets

The question therefore going forward, where is India different to other economies over the next few years. There are four points of difference to highlight:

- Pre-General Election Spending

- India becoming an alternative supply chain

- Low reliance on exports and high dependence of consumption

- Increasing domestic consumption

General elections are due in India next year. A pre-election spending uptick is expected, as the government prepares for key state elections due in 2023 as well as the general election which is due in mid 2024. The pre-election spending boost is not unique to the current election cycle. It has been the norm since the turn of the century in India, where every government that has been re-elected has resorted to this strategy of increasing government spending in the run up to the voting period. The fact that India showed unusual fiscal restraint in 2022 means that the equity markets should welcome this potential stimulus in a world where governments globally have fiscally restrained in the last 6-12 months.

The global pandemic combined with recent geopolitical events have driven both corporates and governments to shift supply chains permanently. The pandemic increased and changed the importance towards ‘just in case’ over ‘just in time’ logistics and not having a significant reliance on one country. Headlines like the below from Bloomberg on 13th April 2023 continue to highlight this theme as ‘Apple Triples India Iphone Output to $7bn in Shift from China’[2]. To add to this, the pandemic has also only enhanced India’s attractiveness as the office to the world as technology has improved for employees to work from any corner of the globe. Combine this with new developments such as government incentives – which are allowing India to gain traction as a factory to the world as well. Investment in services and manufacturing will come from foreign direct investment and a large increase in private domestic investment.

While the first two drivers are unique to India, the world wide theme of the current green energy transition should also bode well for India. The difference for India is that both its energy consumption and energy sources are changing simultaneously in a disruptive fashion. India’s energy needs are still growing and therefore legacy capacity using fossil fuels will not be destroyed as it transitions to an increased share of renewables. India’s per-capita energy consumption is likely to rise significantly in the coming decade, with two-thirds of the incremental supply coming from renewable sources. This should positively impact India’s terms of trade, entail a significant amount in terms energy capex, eventually reduce headline inflation volatility as the imported energy share of GDP declines. Creating new demand for solutions such as electric vehicles, cold-storage chains, and green hydrogen-powered trucks and buses.

To add to this consumer discretionary spending is gaining share in total consumption. India’s income pyramid offers unique breadth of consumption, with the top end spending like the richest in the world and the bottom end still relatively poor. The number of households earning in excess of US$35,000/year is likely to rise fivefold in the coming decade, to over 25 million. The implications are that GDP is likely to rise significantly over the medium term, there will be a discretionary consumption boom and which has the potential for the Indian equity market to outperform its peers.

Unfortunately, for investors attracted by the Indian growth story, the market has always looked expensive. Today it looks excessively so. But that could have been said at many times during the past 25 years.

The 25 year average trailing P/E multiple is 20x, which is roughly where the market is trading at the moment. Going forward, it could be possible for this multiple to trade higher than its historical average as investors get greater confidence in medium term growth.

Over the coming years, there are some additional potential catalysts for India’s financial markets, which could really assist the growth of the economy and hence drive further investment into the equity market. In particular there is the potential that India is included in the global bond indices, which would naturally benefit significantly large inflows, improving liquidity and most likely driving debt finance cheaper. As mentioned earlier, 2024 is an election year in what is a complicated political system, if a majority government was elected it would most like assist in driving India’s growth strategy forward.

Investing in India and the broader subcontinent is not without risks and potential market volatility. Population growth, fragile borders, water shortages, climate changes and an increase in inequality are all key challenges. For those looking to get access to the Indian equity market, it isn’t quite as straight forward when compared to developed markets. But nonetheless, there is a suite of options available through ETFs (Exchange Traded Funds), managed funds and ADRs (American Depository Receipts) trading in the US for some of India’s largest companies. If you wish to discuss further at all, please feel free to get in touch with Mason Stevens

[1] Source: The World Bank, data to end of 2021

[2] Source: Bloomberg, 13th April 2023

The views expressed in this article are the views of the stated author as at the date published and are subject to change based on markets and other conditions. Past performance is not a reliable indicator of future performance. Mason Stevens is only providing general advice in providing this information. You should consider this information, along with all your other investments and strategies when assessing the appropriateness of the information to your individual circumstances. Mason Stevens and its associates and their respective directors and other staff each declare that they may hold interests in securities and/or earn fees or other benefits from transactions arising as a result of information contained in this article.