The AUD/USD has appreciated by 33% since March 2020 and has brought foreign exchange (FX) risk into the forefront of the minds of investors looking at US equity and fixed income markets. We have discussed the factors which have driven, and will continue to drive the AUD in our currency outlooks here and here, as well as in Jesse’s recent piece on the state of the Australian economy.

What is sometimes overlooked by investors is the impact the AUD/USD can have on ASX listed company earnings. Australian equities can be impacted both positively and negatively from the extent to which they rely on international revenue streams, and the locations from which they source inputs.

Companies can apply a multitude of different hedging strategies and elect to implement either a partial or full hedge, both in terms of size and duration. Some companies may even choose to over hedge, should they require it for strategic or speculative purposes. As it is important to be aware of exactly what foreign exchange risks companies have, investors should take into consideration their hedging policies, and their subsequent FX exposures.

Today, I’ll go through the methods in which companies can hedge foreign currency risk, and those who will be positively and negative affected from the strong performance of AUD/USD.

Natural hedge

Companies can minimise FX risk through setting up a natural hedge, where resources are allocated to negatively correlated assets. This can involve paying expenses in the same currency as which you earn, or through choosing to borrow in the same currency from which you would collect revenue in. Natural hedges are often not perfect and can lead to more rigid business structures.

Financial hedge

Financial hedges involve the use of derivatives in the form of forward exchange contracts, FX swaps, cross currency swaps or foreign currency options to artificially reduce foreign exchange risk. The use of these derivatives can differ through both the scale, whether it is a partial or full hedge, and the time frame, in whether the hedge is supposed to protect against short term or long-term movements in exchange rates.

Positively affected – Consumer Discretionary

Whilst consumer discretionary stocks have been largely battered by restrictions related to COVID-19, the pain has been partially softened by reduced costs of imported goods. Companies with private label goods will benefit the most from a stronger AUD, such as Wesfarmers (WES), Adairs (ADH) and Premier Investments (PMV).

Companies such as Beacon Lighting (BLX), Nick Scali (NCK) and Myer (MYR) will also benefit due to importing a large proportion of their stock, with the weakening dollar bolstering profit margins.

These retailers will also be well positioned should consumers continue to spend more at the shops given their inability to travel. If the AUD/USD is able to remain at its current levels, consumer discretionary stocks which pay for imported goods in USD terms will be set up for a strong FY2021.

Negatively affected – Healthcare

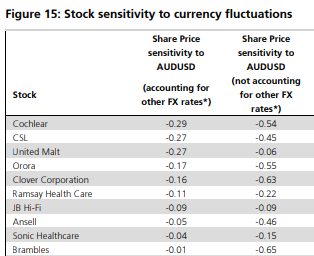

Our major healthcare stocks are all globally diversified, with CSL, Resmed (RMD), Cochlear (COH), Sonic (SHL) and Ramsay (RHC) all deriving over 50% of their revenue from overseas.

This relatively high sectoral exposure to foreign exchange risks is reflected through Cochlear and CSL ranking as the first and second most sensitive ASX shares to AUD/USD over the past 5 years by UBS. This ranking was calculated through taking a time series regression of betas to FX movements after accounting for equity market movements.

However, for a more optimistic outlook on the healthcare sector, please refer to Max’s well written note last week.

Cochlear (COH)

Cochlear has ranked by UBS as the most sensitive ASX listed share to AUD/USD over the past 5 years.

COH is particularly sensitive given it captures 49% of its revenue in North America, has most of its costs in AUD, and reports in AUD.

COH actively hedges against FX risk, however this is mainly focused on short term fluctuations, as opposed to long term movements in exchange rates.

CSL

CSL ranked as the second most sensitive ASX listed share to AUD/USD, with 55% of its revenue generated in the USA. CSL has more of a natural hedge, having US costs and borrowings to services given their extensive operational presence in the USA. CSL also reports in USD terms, however Australian investors will still be impacted by a strengthening AUD/USD through a lower AUD share price and lower dividends.

Negatively affected – Aristocrat Leisure (ALL)

Aristocrat Leisure is exposed to fluctuations in AUD/USD, deriving over half their revenue from their physical presence in the US. In FY20, AUD/USD was largely in ALL’s favour, increasing annual profit after tax and before amortisation by 3.5%, however the AUD/USD will likely put a dent in FY21 profits.

Neutral – Resources and gold miners

Resources and gold stocks such as BHP, RIO, Newcrest (NCM) and Evolution (EVN) have largely been unaffected by FX valuations, given the offsetting relationship between commodity prices and the USD, with commodity prices tending to rise with a weakening USD.

Should commodity prices continue to rise with a weakening USD, investors will be protected from FX volatility.

Outlook

As outlined in our previous currency outlooks, market forecasts for the AUD/USD are bullish, with monetary policy, fiscal policy, risk on sentiment and reflation narratives all pointing towards a weaker USD and a stronger AUD. This will make investors less likely to take on foreign currency risks and will also be important to consider when investing domestically in companies with international exposure.

Foreign currency movements won’t act as a leading influence on the valuations of USD earning Australian equities, however their potential impact is too big to be ignored.

The views expressed in this article are the views of the stated author as at the date published and are subject to change based on markets and other conditions. Past performance is not a reliable indicator of future performance. Mason Stevens is only providing general advice in providing this information. You should consider this information, along with all your other investments and strategies when assessing the appropriateness of the information to your individual circumstances. Mason Stevens and its associates and their respective directors and other staff each declare that they may hold interests in securities and/or earn fees or other benefits from transactions arising as a result of information contained in this article.