The world changed last week, and not just because of the US election.

Pfizer announced a COVID-19 vaccine that is looking to be over 90% effective in stage 3 clinical trials.

The market also knows that many other COVID-19 vaccines are targeting similar treatments, and this means that more vaccines and global deployment is a 2021 agenda, rather than 2022.

Stocks were bid higher.

Bond yields rose (prices down).

Gold sold-off.

Credit spreads tightened.

Real interest rates rose.

The yield curve steepened.

The USD ticked up.

All. At. Once.

Let’s target gold, real interest rates and the USD today – three assets that are all interlinked – and discuss implications for investment.

Pent up demand

There is an incredible amount of pent up demand in the economy (“slack”) because of the events of 2020, something that may change in 2021.

This year, across the globe, people have postponed weddings, holidays and special occasions, and there’s latent demand for leisure, travel, thrill-seeking and joy out there.

Much as the 1918/1919 pandemic was followed by what is now known as the “Roaring Twenties,” we might be looking forward to a Roaring Twenties of our own (though our debt load is substantially higher, comparatively).

This is why markets are rushing to interpret a COVID-19 vaccine, return of employment and resumption in consumptive activity into financial asset prices.

Assuming as well that the latest vaccine news is predictive of an imminent viable vaccine distribution in Q1 2021, investors and corporates are reacting now to set themselves up for success.

Real interest rates

Real interest rates are nominal interest rates that have been adjusted to remove the effect of inflation.

They reflect the REAL cost of funds to a borrower and the REAL yield a lender or bond investor receives.

Real interest rates reflect a time preference for current investments over future investments.

Real interest rates are leading indicators of investment flows and are a financial market gauge of risk appetite.

US real interest rates turned negative this year as investors sought safe-haven bonds for capital protection during COVID-19’s impact in H1 and Q3.

You may ask why an investor would accept a -1% p.a. real return on their funds over a 10-year period?

The reason was that -1% p.a. was deemed a safer investment than possibly more negative returns buying other financial assets such as equities.

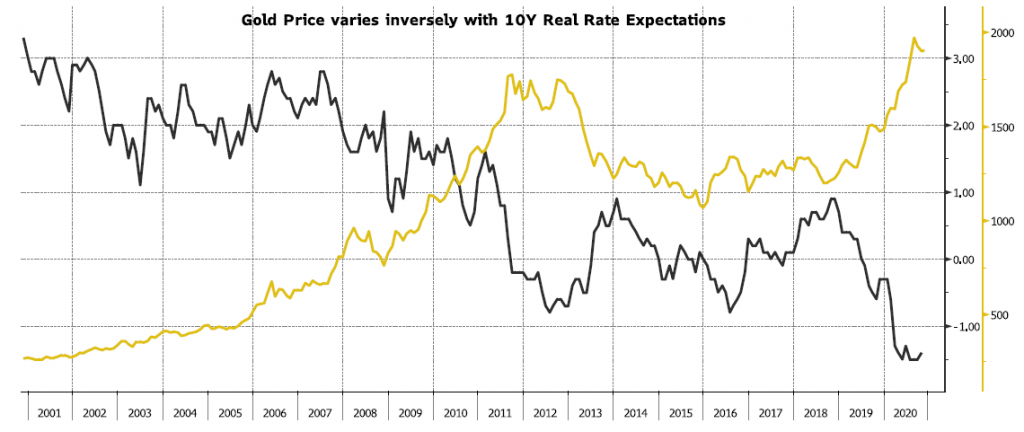

Real interest rates (black line) have just begun to tick-up since last week’s vaccine news, which could well be the inflection point for seeing higher real interest rates.

Source: Territory Funds Management

Gold

You may notice in the above chart that there’s a long-standing inverse correlation between real interest rates and gold prices (based in USD).

I.e. when real interest rates decline, gold increases.

Gold and real interest rates have had this relationship as the shiny golden metal was deemed a store of value and wealth, when real interest rates were declining.

Gold was also bid this year due to historically large government deficit spending that eroded the value of money/currencies.

This narrative was mainstream where a “Blue Wave” result from the US election would’ve resulted in larger budget deficits than what a Red Wave or split Congress would produce.

The facts have now changed post-US election and markets are pairing back bets on US government deficits and future spending, forming a ceiling for gold prices in the near-term, and a base for the US dollar (USD).

US Dollars

For the currency watchers out there, it’s very interesting that while US real interest rates have moved higher, the USD hasn’t.

The US dollar’s value is closely linked to the time value of USD cashflows. Hence, interest rates and currency valuations are intertwined.

Below, I chart 10y US real interest rates (similar to the above chart) versus the USD index (yellow) to show how the relationship has decoupled.

Is this a breakdown in the relationship or is the USD set for a rally?

Source: Bloomberg

To answer this, we need to delve into the sentiment and positioning data that is the backdrop to any trade.

While we know USD has been out of favour these last 6-10 months, investors are betting on further USD downside to come, though the structural backdrop has improved. The below chart shows currency positioning, highlighting investors are net short USD (red bars).

Source: Refinitiv, HSBC

To me, I think it’s too early to call a bottom in the US dollar, though I am ready for an inflection similar to what’s occurring with real interest rates and gold. However, I am ready to change my mind if more fiscal stimulus is approved than expected.

A world with a COVID-19 vaccine

The Pfizer vaccine news last week marks a profound shift in financial markets, where pent up demand that will be let out during 2021 also marks renewed optimism for the future.

As investors, we were profoundly pessimistic this year with Australian bushfires dragging growth, COVID-19 stalling personal and business lives, and international civil unrest in the USA and Brexit still being negotiated.

Much of these concerns have ameliorated and we will start seeing more optimistic outlooks.

The views expressed in this article are the views of the stated author as at the date published and are subject to change based on markets and other conditions. Past performance is not a reliable indicator of future performance. Mason Stevens is only providing general advice in providing this information. You should consider this information, along with all your other investments and strategies when assessing the appropriateness of the information to your individual circumstances. Mason Stevens and its associates and their respective directors and other staff each declare that they may hold interests in securities and/or earn fees or other benefits from transactions arising as a result of information contained in this article.