Competitive people like to outperform, they can’t help themselves. Naturally, then watching financial markets gyrate attracts curious and competitive minds.

Positioning themselves for the dopamine rush that outperformance provides had been easier, up until the start of this year. It was so easy it became an acronym – FAANG, except you, had to fit M in somehow for Microsoft.

These high-growth technology companies were spending and borrowing at ever-increasing rates in a race for dominance, whilst their funding costs were falling at the same time as interest rates fell.

It could be argued that the speed of changes that technology companies were forcing on the other parts of the economy and their impacts on the labour force are a major contributing reason as to why interest rates kept falling, in turn making their race easier.

That changed at the start of this year, as the bond market got the wobbles and bond prices fell. Equity markets questioned the price they were willing to pay for that growth and the switch to Value stocks became the dominant equity flow.

The Bloomberg chart below shows two ETFs – Vanguard’s SP500 Growth (VOOG: NYSE) performance over 1 yr against Vanguard’s Value Fund ETF (VOOV: NYSE).

Source: Bloomberg

The chart is normalised to a 100 base so we’re charting pure performance not ETF prices. While the switch to value paid for a while this year – if you didn’t pick it, you haven’t missed out.

As soon as bond prices stabilised – triggered by the fear the Delta variant of COVID 19 was going to dramatically change world growth outlooks for the worse – exposure to the mega tech companies became the preferred allocation again. Pull this chart back five years and you get the picture why pulling out of mega tech is dangerous.

Source: Bloomberg

As we head into the last quarter of 2021 are we going to see a repeat of the first quarter’s playbook?

The chances are high, we have been in a long bull market, valuations are extreme and while interest rates are still low the bond market has rolled over again as vaccination rates globally mean life is starting to return to normal.

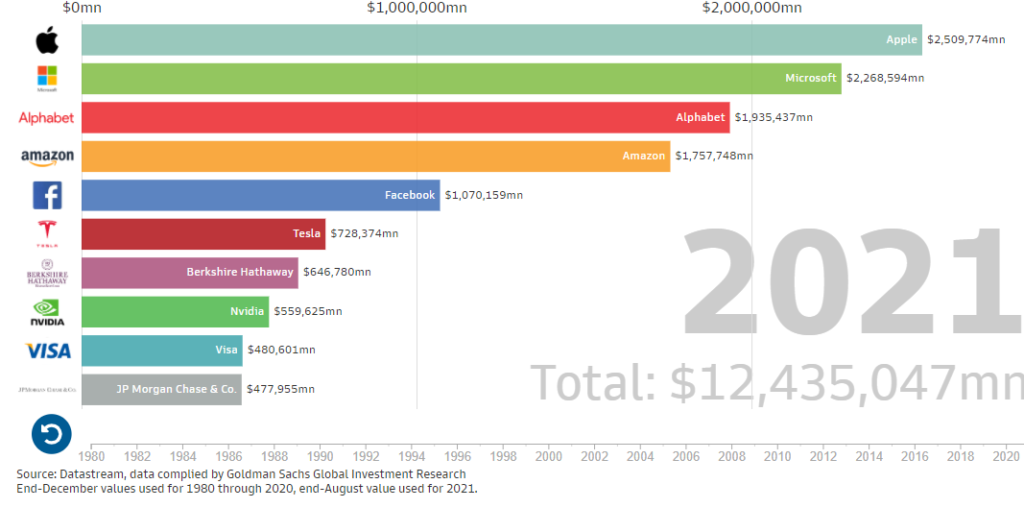

If you look at the below slide from Datastream, showing the largest stocks by market capitalisation in the SP500, its now FAAMG in the top 5.

Their dominance is complete, their stock performance is now largely the market performance.

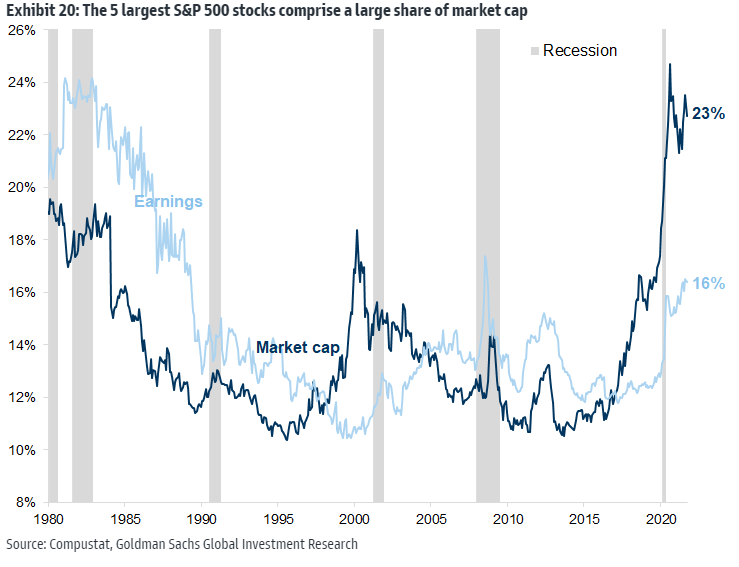

The current concentration of these market leaders as a percentage of market cap is extreme but not unusual when looking back in history when other industries drove growth. If you’re looking to outperform like active managers will be, then you will be lightening exposure and that pace will pick up if bond yields continue to rise.

Currently the risk-free rate of return as measured by the US Government 10-Year Yield is approx. 1.53%.

It’s jumped over 20bps over the last 5 sessions and most investment banks see that figure rising, Citibank are looking for that yield to push to 2 percent by year-end.

If that’s the case the momentum for the switch to Value from Growth stocks will continue. It’s hard to go higher when you’re already at the top.

This is not to say equities are not going to continue pushing higher in the face of rising interest rates, it’s just the focus will change again for a while. The chart from Goldman Sachs below highlights the recent acceleration of their stock price against earnings contribution.

That gap has become a bit extreme so there is room again to look for value.

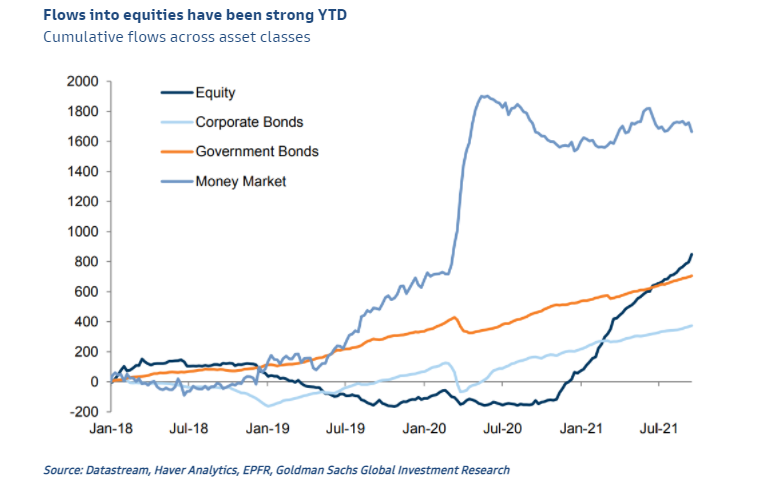

Flows into equities year to date have been strong as can been seen from the Asset flow chart below.

Given no one is expecting a dramatic shift in major central bank policy in the near term it’s hard to see that shift from higher-risk equities slowing over the longer term.

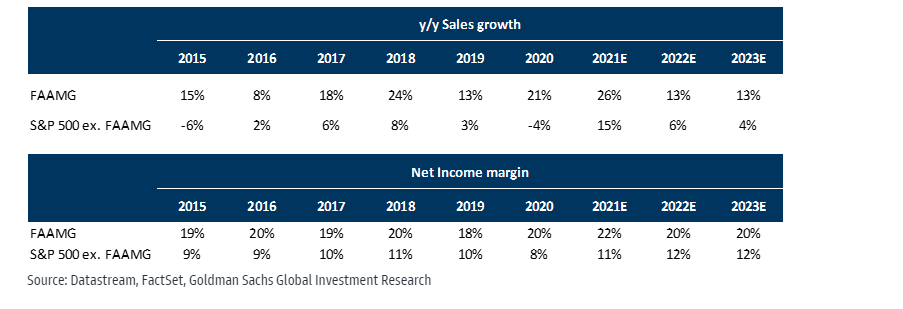

Earnings continue to grow but the pace for mega-tech is also slowing.

The margins these companies maintain and the moats to competition from continued reinvestment into research and development will continue to protect their position, but not their forward valuation.

While we go through periods where the bond market starts factoring in higher inflation for a longer less transitory period, then the allocations may change but Tech weightings will remain high because their contribution to index earnings overall continues to climb.

Regulation would appear the greatest threat to their dominance.

Anyone who has had exposure to the Chinese competitors to these companies can attest. Given the structure of democratically elected representatives spread over two houses of government – with each member holding differing concerns relevant to the people, he answers to- then that pace of change in regulation will be slower than it has been in China.

If you’re uncomfortable with the short-term outlook, then a longer time horizon will make you feel comfortable with your asset allocation to equity. Citibank’s estimates for earnings next year for the SP500 show just over 9% growth.

There will be periods of higher volatility and market pullbacks.

Positioning in sectors like FAAMG can get extreme and valuation opportunities in other sectors may become compelling but the domination of the technology sector and its impact on our daily lives is only picking up pace.

From a stock picker perspective, the opportunity will be picking the emerging companies within the space and less so concerns for the sector.

The views expressed in this article are the views of the stated author as at the date published and are subject to change based on markets and other conditions. Past performance is not a reliable indicator of future performance. Mason Stevens is only providing general advice in providing this information. You should consider this information, along with all your other investments and strategies when assessing the appropriateness of the information to your individual circumstances. Mason Stevens and its associates and their respective directors and other staff each declare that they may hold interests in securities and/or earn fees or other benefits from transactions arising as a result of information contained in this article.