Banks are regularly looked at as a barometer for economic expectations, with their earnings viewed as a key signpost to investors across the globe.

This US reporting season is no different. With all eyes firmly on the banks to see what clues they can provide the market on how the economy is coping, post the flurry of recent rate rises in this latest cycle as central banks try to curb inflation.

Back in April when we received the earnings for 1Q22, we wrote a note (link) highlighting how the market was full of uncertainty thanks to the high inflationary environment and questions surrounding how it would be tamed.

Since then, there has been a shift in headlines with a growing focus now being placed on the possibility of a global recession and just how the consumer is handling the impact of rising interest rates.

This week we saw the last of the banks report their earnings and financial markets were finally able to fully digest the news and what may lay ahead for the economy.

A mixed bag

This batch of earnings for the banks saw a mixed bag, with some companies missing estimates, while others having strong beats depending on their business mix.

When drilling down, there were some trends across all the banks, from consumer spending remaining seemingly strong to investment banking revenue being lower on the back of poor conditions.

Revenue from consumer and small business banking, lifted strongly across most banks, with this mainly due to the fact that deposit balances remained strong, coupled with a higher interest rate environment.

Across the board, we saw little surprise in the fact that revenue attributed to wealth management as well as investment banking was lower as asset values had been wiped by poor financial market performance.

While the revenue component of the banks’ earnings draws some attention, most of the focus is placed upon what the banks are seeing in terms of the domestic and global economic backdrop. This can be seen by looking at consumer and business spending.

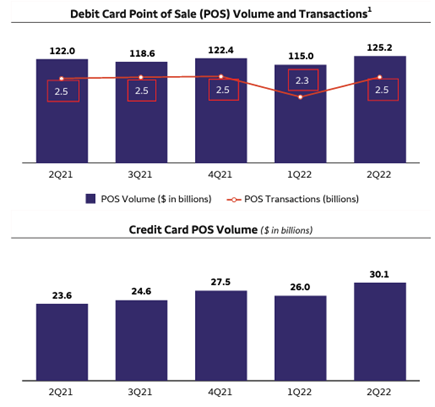

Many of the major banks reported strong consumer spending, with JP Morgan’s Jamie Dimon stating that “In Consumer & Community Banking, combined debit and credit card spend was up 15% with travel and dining spend remaining robust. Card loans were up 16% with continued strong new account originations.” Bank of America’s Brian Moynihan mirrored this stating, “Our U.S. consumer clients remained resilient with continued strong deposit balances and spending levels,” with their combined credit/debit card spend up 10% YoY. Finally, Wells Fargo also echoed this strength in spending with debit and credit card POS Volume and transactions higher (see Chart 1)

Chart 1: Wells Fargo Debit & Credit Card POS Volume & Transactions

Source: Wells Fargo 2Q22 Financial Results

While consumer spending remained strong from a debit and credit card spending perspective, the banks noted that consumers are continuing to worry about the longer-term outlook with home lending volumes well down.

This impacted the banks revenues largely with JPM noting their home lending revenue was down 14% QoQ thanks to the lower volume of originations, as well as lower margins and tighter loan spreads. Bank of America also increased their provisions for credit losses as a result of the dampening macroeconomic outlook. However, JP Morgan’s Jamie Dimon noted that “Commercial Banking loans were up 7% on strong new loan originations”.

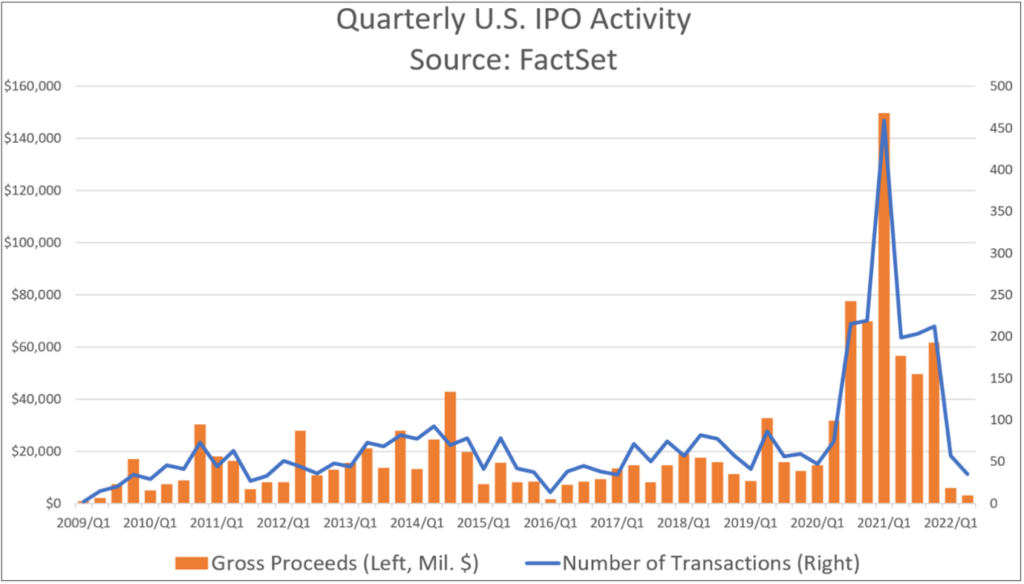

In terms of underperforming segments, the banks saw their heaviest downturns in the investment banking fees space. Again this wasn’t a surprise to the market as the past quarter hasn’t seen many deals come to market this year, in fact, the first half of 2022 represented the weakest 6-month period for US IPOs since 4Q16-1Q17 – a far cry from the dizzying heights of 2020-21 (see below in chart 2)

Chart 2: Quarterly U.S. IPO Activity

Source: Factset

FactSet data showed that 1073 companies IPO’d in 2021, raising $317 billion, whereas the first half of 2022 totalled just under $ 9 billion across 92 companies.

Stormy clouds or sunny skies ahead?

Whilst the banks have broadly performed better than expected this earnings season, their outlook for the economy isn’t as convincing. Off the back of Goldman Sachs’ results, we saw them announce that they would be slowing their rate of hiring and reducing certain professional fees going forward. CFO Denis Coleman attributed this to “the challenging operating environment” where they “are closely re-examining all of our forward spending and investment plans to ensure the best use of our resources.”

In JP Morgan’s results, they announced that they would be halting their share buyback. Dimon said that they temporarily suspended the buyback as a result of the recent stress tests and in order to quickly meet the higher requirements that an already scheduled GSIB increase has brought about.

Overall, the commentary from the US banks highlights they believe that consumers are well placed to deal with the challenging economic environment going forward, however they are still acting very cautiously to ensure they remain able to serve clients in these challenging times.

Financial markets are absorbing the news from the US banks and developing a slightly more optimistic near-term outlook; however, they are simultaneously echoing a more cautious nature over the longer term thanks to the uncertain macroeconomic environment we are currently living in. Consumer and investor cash levels are higher than normal, but this is keeping them well positioned to remain nimble and able to act accordingly to any further changes that the economy throws at them.

The views expressed in this article are the views of the stated author as at the date published and are subject to change based on markets and other conditions. Past performance is not a reliable indicator of future performance. Mason Stevens is only providing general advice in providing this information. You should consider this information, along with all your other investments and strategies when assessing the appropriateness of the information to your individual circumstances. Mason Stevens and its associates and their respective directors and other staff each declare that they may hold interests in securities and/or earn fees or other benefits from transactions arising as a result of information contained in this article.