The February Australia results period has now come to a close. Heading into the earnings season investors were curious to see whether companies would finally start to show signs of stress from the rapid increase in rate rises by the RBA, or whether companies would still be doing better than expected as highlighted in the US earnings season just passed.

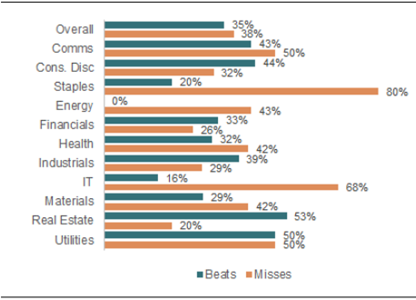

Across the market results were quite mixed, with corporates reporting EPS beats of 35% and misses of 38% when compared to consensus forecasts. Other metrics such as sales, PBT (profit before tax), and DPS (dividend per share) were also mixed in terms of beats and misses using a +3/-3% beat/miss level. The below chart shows the % of EPS beats and misses on the overall market and sectors:

Chart 1: Result EPS beat/miss on overall market and sectors

Source: Barrenjoey Research estimates, Factset, Visible Alpha

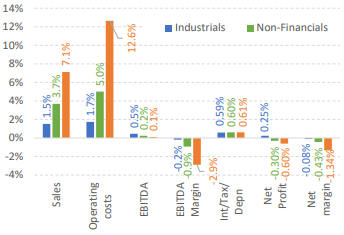

One theme that was quite noticeable across the entirety of the earnings season, was the contrast between the top and bottom-line results. Companies across the board saw strength at a the top line (revenue), with 75% of sectors seeing upgrades to revenue for FY23. This strength has been supported by a few areas; inflation and pricing power, households continuing to spend due to higher savings rates post the Covid lockdown period, a weaker AUD, recovering migration and finally stronger company balance sheets which have supported financing more capex.

Despite the strength seen with revenues, all bar one sector (healthcare) saw margin forecasts revised lower. These downgrades to margin forecasts were due higher costs – operating costs grew at an average of 14% YoY, which is a new post pandemic high. As can be seen in Chart 3, in terms of sectors the bulk of these revisions are seen in the commodities sector which are falling from record levels.

Chart 2: Stronger sales & weaker margins

Source: MST Marquee, Company data, Factset

Chart 3: Margin forecasts

Source: MST Marquee, Company data, Factset

The majority of companies did note that while they have experienced higher costs, they do believe that input costs have peaked and are starting to ease a little given the falls in commodity prices and improved supply chains. Companies did also mention that labour costs are an exception to this with wages still rising as labour shortages continue to prove a challenge, particularly in the mining and construction space.

Barrenjoey once again tracked what they call “PEAD” (post earnings announcement drift) to see which companies have produced positive relative returns post announcement and which have been negative. Over the total market they noted 49% of companies presented positive PEAD while 57% presented negative PEAD. This skew to negative PEAD was largely seen in the ASX ex100 companies, with 61% producing a negative PEAD vs the ASX100 where it was an even split between positive and negative PEAD.

Post earnings season brokers have provided their views on certain sectors/factors. Goldman Sachs feel that with the headwinds of a slowing economy and higher rates ahead, investors should look at the valuation dispersion between defensive/growth stocks and value/cyclical stocks as they believe this will continue to normalise given cyclicals trade at a discount to the market. Barrenjoey have a defensive tilt in their portfolio and are underweight banks because of the evidence pointing towards net interest margins (NIMs) peaking. They are also wary of consumer and housing exposures due to the delayed effect of tightening on earnings. They’re more cautious of REITs given the recent outperformance of the sector despite broadly unchanged bond yields.

Overall, companies have once again been far more resilient than expected which is shown by the fact that 2023 EPS estimates increased by 0.1% compared to the long-term average of -0.7%. The majority of companies reported in-line results – with some having pre-released their results. Moving forward from here, the outlook still remains uncertain as businesses continue to battle with stickier than expected inflation and the magnitude of 10 consecutive rate rises with the potential for further rises yet to come.

The views expressed in this article are the views of the stated author as at the date published and are subject to change based on markets and other conditions. Past performance is not a reliable indicator of future performance. Mason Stevens is only providing general advice in providing this information. You should consider this information, along with all your other investments and strategies when assessing the appropriateness of the information to your individual circumstances. Mason Stevens and its associates and their respective directors and other staff each declare that they may hold interests in securities and/or earn fees or other benefits from transactions arising as a result of information contained in this article.