As always, the quarterly US earnings reports are very closely watched for how the global economy is fairing. The combination of near full employment, higher than normal personal saving rates and an increased demand post the COVID 19 pandemic, theoretically should all bode well for the strength in the economy. With the S&P500 up 7.7% and Nasdaq up 16.9% so far this year, the equities market currently has some good momentum, but the question is, can this continue? It should be noted that the rally has been narrow, with Apple, Microsoft and Meta explaining more than half the S&P’s return this year. With interest rates having been at close to zero at the beginning of last year, many are interested to see what impact close to 500bps of rate hikes by the Federal Reserve Bank has had.

With almost 75% of S&P500 companies having reported so far, the average EPS surprise has been +7% (which is more than historical averages). 71% of firms have beaten consensus EPS expectations by more than a standard deviation of analyst estimates, well above the long-term average of 46%. Surprisingly strong results, highlighting that perhaps the global rate tightening cycle is yet have some impact. To this stage and probably as expected, large caps have fared well with Tech seeing strength more recently. Consumer facing stocks have seen a wide range of results, with some companies reporting a downshift in consumer spending overall (Verizon, UPS) but others have been successful at pushing through price increases (McDonalds, Chipotle, Mondelez). Perhaps this highlights that consumers are not so focused on cutting back in certain segments. A surprise to many is that Homebuilder sector earnings have confirmed an acceleration in sales activity in the past few weeks. Providing hope for a market acceleration in 2H23, alongside relatively steady guidance from corporates. While the quarter has been stronger than expected thus far, mentions of tougher macroeconomic conditions and overall caution remain prevalent.

Revisions are starting to be made to EPS estimates for quarters in the back half of the year, but these estimates have fallen less vs nearer quarters. Many market watchers are looking closely at this earnings season to see what the outlook is for the rest of 2023. In previous earnings seasons, some companies had been quite reluctant to give a guidance range. Yet so far this has not transpired in any significant way. Estimates for 2023 S&P earnings have fallen ~4% YTD. Revisions downward have been the most material for Financials, Energy, and Consumer Discretionary. Communication Services and Staples have seen estimates revised upward.

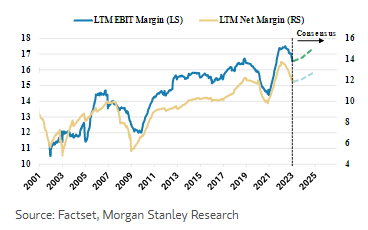

Sales for 1Q23 are expected to grow 5% for the S&P 500. Considering inflation is forecast to be broadly in line with this level, consensus is pricing flat to a small increase in real growth. The lower sales at the index level are primarily driven by lower single digit growth in Healthcare, Tech and Energy, which make up 38% of Sales. Looking at annual figures, Financials, Staples, and REITs are expected to lead 2023 sales while Tech and Discretionary are expected to lead in 2024. Consensus expects margins to trough in 1Q and recover in 2H23 (See Figure 1). Margins have fallen from 2022 peak levels, but the key debate is whether 1Q is really the trough. One of the concerns for central banks at the moment is the higher than expected wage increases, driven by tightness in the labour market. Looking at net margins YTD, Commercial & Professional Services and Communication Services lead with positive revisions while Pharma, Semis, and Autos have seen negative revisions

Figure 1: Margins are f/c to trough in 1Q 2023.

Overall, it has been a good earnings season so far. While inflation remains sticky – and perhaps to some extent because of it – corporate earnings and margins have fared better than expected. Both sales and margins have exceeded expectations and S&P 500 EPS growth is now tracking at -4% y/y, vs. a consensus estimate of -7% before the season. The direction of analyst EPS revisions has also continued to improve. That said, the market is forecasting very little EPS growth in the US through to end 2024. With valuations in line with long term averages, the combination does not offer much return for the risk in the face of 5% risk free US dollar cash return.

The views expressed in this article are the views of the stated author as at the date published and are subject to change based on markets and other conditions. Past performance is not a reliable indicator of future performance. Mason Stevens is only providing general advice in providing this information. You should consider this information, along with all your other investments and strategies when assessing the appropriateness of the information to your individual circumstances. Mason Stevens and its associates and their respective directors and other staff each declare that they may hold interests in securities and/or earn fees or other benefits from transactions arising as a result of information contained in this article.