“I’m an easy read but I ain’t no open book,

Got a knack for making things harder than they look”

Luke Combs (2019)

Something the RBA is particularly good at is making their balance sheet transparent so that market watchers such as ourselves can analyse their activity to pull the levers of monetary policy.

The RBA’s website publishes weekly updates of the Bank’s balance sheet, which contains data regarding their investment portfolio, the break-down of deposits by government, banks and foreign central banks, as well as their open market transactional data.

It is quite overwhelming at first – but given the RBA’s impact on our local money market and financial markets – as well as the end of 2019/20 financial year looming – I think it’s the right time to read the tea leaves.

Impact on Federal Budget

It’s important to note that the RBA can pay contributions to the Federal government – usually done once per year around EOFY.

The size of this contributory “dividend” is a negotiation between the RBA and the government and based upon the operating profit of the RBA.

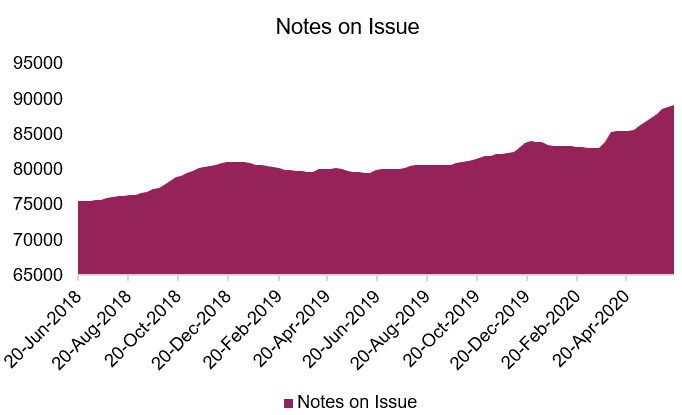

In particular, the operating profit of the RBA is significantly improved by an increase in the amount of bank notes on issue – the cash that is circulating around the physical economy and used in payments for goods and services.

“Seignorage”, or the issuance of bank notes, is $9.1bio AUD higher as at 17 June 2020, than this time last year.

This is almost pure profit for the RBA and will reflect in a high contribution to the operating profit of the Bank, and potentially support a significant dividend to the Federal Budget.

From the Federal Budget point of view – RBA dividends are not forecast or included in outlooks, so would be a “surprise” boon to the Budget outcome.

Source: RBA, Mason Stevens

RBA support for domestic markets

The RBA’s overall balance sheet is $86bio higher than last year, increasing from $185bio to $271bio.

This increase is largely due to a $46bio increase of Exchange Settlement balances (bank deposits held at the RBA), and a $35bio increase in government deposits due to an increase in tax receipts.

The increase in government deposits will continue to build into EOFY – as fiscal appropriations (grants etc.) commence in the new financial year, and usually sees ~40bio of approved spending flow into the economy over a 3-4-week period during July.

This build in the RBA’s liability profile sees a reflective increase in their asset book.

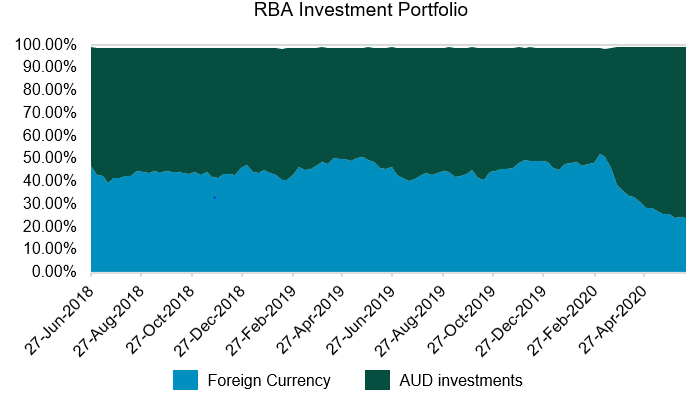

This manifests into Australian dollar investments, which are $106bio higher year-on-year.

It’s no secret the RBA has been supportive of local bond and money markets – and they have done so by rotating their existing investment portfolio (asset book) out of foreign securities towards AUD securities.

As such, foreign investments decreased by 21bio AUD year on year, and reflects the limited amount of FX intervention the RBA has been engaging in to raise foreign currency. i.e. they have been not selling AUD to buy USD, JPY, EUR, GBP – they’ve actually been selling these foreign currencies to buy AUD assets.

Source: RBA, Mason Stevens

“Off balance sheet”

The weekly Statement of Liabilities and Assets the RBA provides may lead us to the conclusion that the RBA has provided approximately $106bio of support for local markets over the last 12-month period – this isn’t the case – it is actually more.

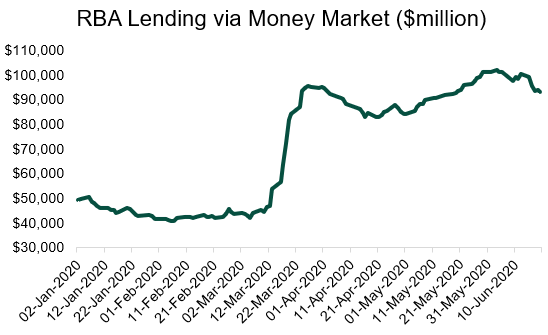

The above number does not increase the Open Market Operation facilities the RBA engages in through the “repo” market – secured lending – or its Quantitative Easing program.

These facilities are not recorded under the RBA’s balance sheet – they’re considered “off balance sheet”.

If we include these two other types of market operation, then the RBA has added an additional $56bio via repos, and ~50bio through QE, buying government and state government bonds in secondary markets.

Chart of the RBA’s lending via money market (repurchase agreements) below:

Source: RBA, Mason Stevens

Ergo, 106+50+56 = 212bio of support through open market transactions.

Summary

This RBA data is a timely reminder that the Bank is much more than just the author of the Overnight Cash Rate that garners most of the attention of mainstream and financial news media.

The Bank quietly pulls various levers on an intra-day and inter-day basis to finesse the plumbing and function of the Australian money markets, but also engages in supportive acts to allow the flow of credit from the banking system to the real economy.

On face value, the RBA is also able to contribute a significant profit to the Commonwealth Treasury which will be a boon given the Budget’s deterioration from COVID-19 related stimulus payments.

Lastly, we’ll likely see a large government contribution go Q2 and Q3 GDP as their appropriations hit the market and result in consumptive activity.

The views expressed in this article are the views of the stated author as at the date published and are subject to change based on markets and other conditions. Past performance is not a reliable indicator of future performance. Mason Stevens is only providing general advice in providing this information. You should consider this information, along with all your other investments and strategies when assessing the appropriateness of the information to your individual circumstances. Mason Stevens and its associates and their respective directors and other staff each declare that they may hold interests in securities and/or earn fees or other benefits from transactions arising as a result of information contained in this article.