Australian RMBS is an extremely well-performed asset class both in terms of credit performance, but also the return available for the credit risk taken. No tranche of an Australian RMBS has ever passed a loss to bondholders at any ratings grade according to S&P including sub-investment grade. Ratings agencies note how conducive the Australian Mortgage market is to securitisation and compare it extremely favourably versus other jurisdictions like the US for example. Deep analysis is done on each pool by rating agencies, as it comes to market and is then monitored through the life of the transaction. The spreads available are at multiples of similarly rated Bank debt providing a clear opportunity to enhance portfolio returns and current pricing is compelling with RMBS spreads near their COVID wides.

AU RMBS Overview

Residential Mortgage-Backed Securities (RMBS) are interest-bearing debt securities secured by discrete pools of Residential Home Loans. RMBS bonds (or notes) in Australia are secured by first ranking full recourse mortgages over the underlying properties. An SPV (trust) is established to have legal ownership of the mortgages and is segregated and bankruptcy remote from the originator (e.g. Westpac, Suncorp or Liberty). Investors in RMBS are not reliant on the mortgage originator for their returns, but the credit quality and home valuations of the underlying properties.

The SPV uses a structure that apportions risk to different note holders in much the same way that a Bank issues various tiers of capital. Banks issue shares that have the most variable returns and losses accrue here first. Hybrid Notes are next in order of losses followed by Tier 2 Subordinated Notes, then Wholesale borrowings including Senior Bonds and then Deposits. The least risky of all bank issuance are Covered Bonds where the bondholder not only have the resources of the bank to ensure they are repaid, but also a pool of underlying mortgages.

In an RMBS structure, there are also typically 5 or more layers of risk known as credit tranches with the most risk remote bearing AAA ratings (three notches stronger than the Big 4’s senior rating) followed by other Investment Grade tranches and then Sub Investment Grade tranches. The most junior (and lowest rated) tranche would be the first to suffer losses if the mortgage pool was to have a sequence of defaults and home sales at a loss. The bottom tranche is often known as the Seller Note as it is often held by the originating entity which gives confidence to other bondholders that they still have an economic interest in the pool.

The legal environment in Australia is particularly welcoming for RMBS investors, with Standard & Poor’s noting that:

- Australian law provides for full recourse to borrowers on residential mortgage loans (lenders will actively pursue this right if necessary). This affects a borrower’s credit-risk consciousness and payment behaviour through the loan term, and largely limits the decision to default on affordability factors rather than on the borrower’s equity in the property.

- The Australian legal environment is relatively more creditor friendly and offers a stronger enforcement regime than the U.S. This reinforces the more conservative credit culture among Australian borrowers.

- The absence of tax deductions on Australian loans secured by owner-occupied homes motivates borrowers to make partial repayments when possible, resulting in a rapid amortization of loan balances and increasing borrower equity in their homes.

- The archetypical Australian residential mortgage pool has lower risk features than the archetypical U.S. pool.

- The originate-to-distribute model that was popular in the aggregation of mortgage loans for securitization in the U.S. has not been a strong feature in Australia. Most originators in Australia typically assume various roles in transactions and are thereby closely aligned by their interests to the performance of the RMBS transactions.

As a result, there has never been a loss on any Australian-rated RMBS-rated tranche including both Investment Grade and Sub Investment Grade bonds. Any weakness in the performance of the underlying borrower base has been captured by the structural and credit enhancements before they were severe enough to cause bondholders to write down their capital values.

The Australian RMBS market is broken up into subsectors and RMBS issuers offer pools of mortgages with similar characteristics:

- Prime (ADI and Non-ADI): prime pools are of the highest quality borrower.

- Non-conforming may include a wider range of borrowers including those with:

- adverse credit histories,

- low or no documentation where many of the borrowers are self-employed,

- or an SMSF.

Each trust has its own individual risk characteristics depending on geography, borrower type (e.g. individual vs company), loan to valuation distribution, seasoning, owner-occupied or investment, interest only and quality of borrower (to name a few).

Australian RMBS are sold at spread levels far in excess of most other forms of equivalently rated issuance. AA-rated RMBS notes will often be available at 2.0 to 2.5 times the spread available for major bank senior paper rated two notches lower. Both the banking system and RMBS issuers are correlated to the Australian housing market, yet the structured nature of RMBS means they provide an extremely generous margin uplift for the risk.

Rating and Tranching Methodology

As noted above, every trust is tranched for varying credit risk tiers (seniority) and tenor (weighted average life). The mortgage pool is shared by all tranches, but each tranche will have distinct risk hierarchy and often distinct repayment expectations. Forms of credit enhancement (CE) varies between trusts and can include hard CE (each note with hard CE has other notes that are subordinated to it within the capital structure), Lenders Mortgage Insurance (LMI), trust income (excess spread), credit reserves and owners’ equity.

Although RMBS legal maturities can be 30 years long, very few mortgages remain outstanding for their whole term as householder are easily able to refinance if they wish as well as discharge when they sell their home for any reason. All structures have issuer calls and these prepayments and calls effectively reduce the tenor on the bonds to approximately 3-5 years in most cases depending on issuer.

The main risks associated with RMBS include adverse property prices, increasing unemployment and mortgage rates (which broadly move with the RBA cash rate). The credit tranching methodology is driven by the amount of support is required for a tranche to achieve the rating grade sought. Because the losses are passed sequentially through the trust from the lowest-rated tranche to the highest, each tranche has an interaction with the ones above and below it in terms of sizing and maturity.

It should be noted that in the past the AOFM has supported the AU securitisation market by participating in AAA notes through the GFC period. In addition, much of the AAA-rated RMBS is repo eligible which helps in providing overall market liquidity. These are all market pricing measures because no S&P-rated tranche in Australia has ever passed a realised loss to bondholders including throughout the GFC.

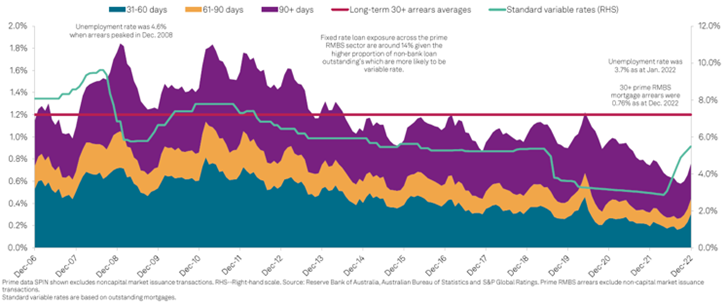

Arrears Cycle

Prime Arrears Are Rising But Still Well Below Long Term Averages

Source S&P Global

Arrears are correlated to the economy and most specifically the unemployment rate. In March 2023, unemployment is near historic lows at 3.5% although it is forecast to rise by many economists including the RBA. The robust structures that support noteholders are sized to support the transaction through its whole lifecycle and as noted, even in times of much higher unemployment these measure have proven to be robust.

S&P Methodology

The rating agencies in general have undertaken huge changes to their methodology since the GFC where they were largely criticized for rating US MBS deals too high for the given risk. The rating agencies now have a robust methodology and have applied regional nuances for each country where applicable. In order to determine the rating and amount of credit enhancement required for each tranche, S&P compares every pool to the “archetypical” Australian residential mortgage pool. They then make adjustments to the subordination requirements by applying a series of factors for different characteristics. These factors increase subordination and CE levels for riskier loans giving more protection to noteholders.

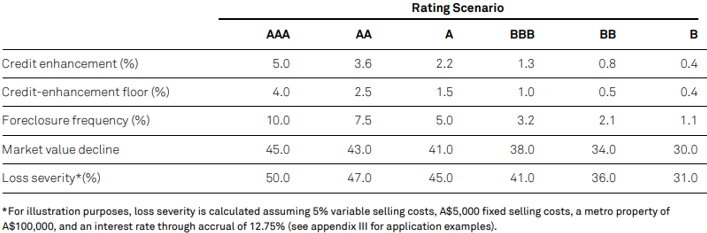

S&P begin their modelling process at the ‘AAA’ rating level, by ensuring a minimum floor of credit enhancement accords to the estimated loss that the archetypical pool of mortgages will likely incur, under scenarios of extreme economic stress in Australia. The table below shows the characteristics of that archetypical Australian Pool. The lower the rating level, the lower the Credit Enhancement required for the rating.

Key Credit-Enhancement Components for the Archetypical Pool by Rating

Source S&P Global

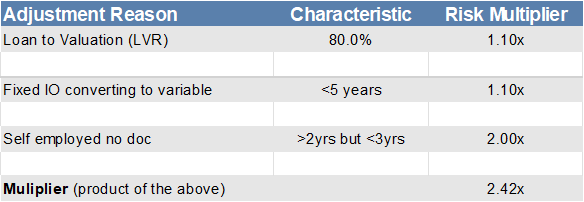

Below is an example of the S&P methodology to assess a self-employed borrower who has a loan to valuation rating of 80% and an interest only fixed period of less than 5 years, after which the loan reverts to floating. Each of the characteristics below is “weaker” than the archetype criteria meaning the risk for this borrower is a multiple of the typical loan. The credit support required for this loan is a multiple of 2.42 times meaning the credit enhancement required for the loan must increase by a factor of 2.42x.

In reality, adjustments to credit-enhancement levels for the actual pool reflect the extent to which the underlying loans and the pool have stronger or weaker credit characteristics than the archetypical loan pool examined on a loan-by-loan basis.

S&P Frequency Foreclosure (Default Rate) Adjustment Process (Example)

Source: S&P Global

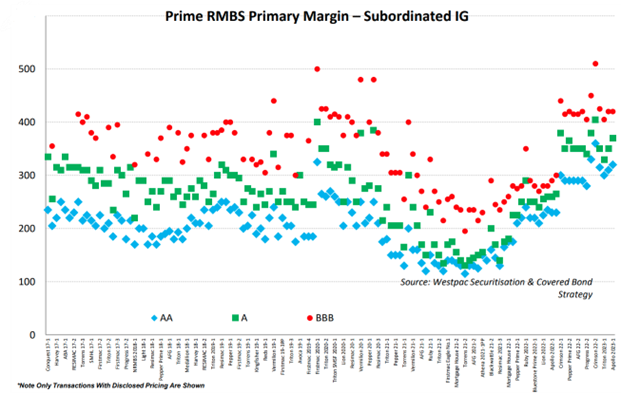

Recent Relative Value

Somewhat due to the fear of the fixed rate mortgage cliff, broader weakening in regional financials globally and the 350bps of RBA cash rate hikes since May-22, RMBS is currently priced at similar levels that were seen in the depths of the COVID selloff in 2020. When compared to other financial issuance the relative value is compelling.

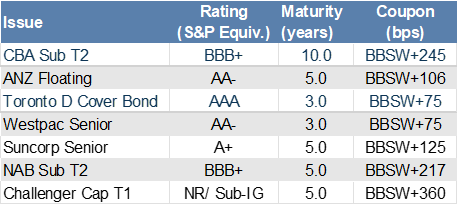

Per below a recent deal issued by Suncorp (Apollo 2023-1) saw a 5.5yr (to call date) AA rated note issued at 320bp over BBSW; compare this to a Tier 2 subordinated issue (rated BBB+) by CBA in March which was a 10yr (to call date) issued at 245 over BBSW. That is a 75bp pickup for a higher rated note. Further the Apollo is secured versus T2 not secured. Another point to make is that many major bank hybrids currently trade around the 300 mark which are BBB- equivalent.

Many can understand not going down to a BB in this environment given the risks, however at a AA rating level of the structure it seems hard to ignore.

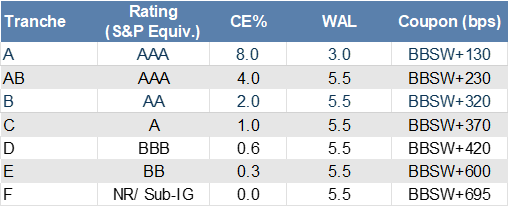

Suncorp Apollo 2023-1 RMBS

Source: Bloomberg

Recent AUD Primary Issuance – Financial Issuers

Source: Bloomberg

The views expressed in this article are the views of the stated author as at the date published and are subject to change based on markets and other conditions. Past performance is not a reliable indicator of future performance. Mason Stevens is only providing general advice in providing this information. You should consider this information, along with all your other investments and strategies when assessing the appropriateness of the information to your individual circumstances. Mason Stevens and its associates and their respective directors and other staff each declare that they may hold interests in securities and/or earn fees or other benefits from transactions arising as a result of information contained in this article.