Investors who took the decision to de-risk their portfolio in 2021 by investing in fixed-rate bonds have seen unwelcome revaluation losses in their portfolios. These transitionary “losses” are almost totally related to opportunity cost rather than any likelihood they won’t get their agreed interest and principal by maturity. This can be disconcerting, but opportunity cost only means a loss if the asset is sold before the term of the original investment or defaults rather than market price movements.

Standard & Poor’s continue to have a benign view of defaults for 2022 (remaining below long-term averages), and there have been negligible investment-grade defaults in the last 10 years. Although the term “defensive” might feel strained at the moment, these legacy bonds will still most likely deliver the income investors agreed to, and what is more the principal will be returned in full. The defensive nature of the allocation is this contractual requirement for the borrower or bond issuer to repay you in full is unlike equities or other market-based investments.

Given that interest rates globally were low for long periods there was little room for rates to go down and at some point these low rates would “normalise” upwards. Investors looking to add income certainty to their portfolio are now in a much better position than only a year ago but there is always the question of whether rates can go higher still. The value of certainty of returns should not be dismissed and no matter whether rates rise even further than the market has already priced in, the income offered at today’s pricing is worth considering.

Interest rate markets are particularly adept at adjusting quickly to future rate expectations. The Reserve Bank has flagged that they feel the neutral base rate of interest is in the 1.6/2% range meaning the current 11am rate is still at emergency settings. In the clamour to quantify how much the RBA would need to raise rates to avoid an inflationary spiral, markets have already priced in rate hikes to 4% by June of 2023. At that pricing the average Australian mortgage will be priced at over 6.25%.

If this market prediction comes to fruition without causing a significant slowdown in the economy and drop in house prices we would have to see significant growth in wages and salaries to keep pace. A more likely view (endorsed by respected commentators like Bill Evans the Chief Economist of Westpac) is that the RBA will have to pause well before that level to allow effects of early tightening to work through the economy and avoid a dramatic reduction in consumer confidence.

Many confidence measures are already heralding a softness and lack of resilience. Although the lowest paid will be receiving a Minimum Wage boost of 5.2%, the governor of the Reserve Bank is urging employees and employers alike to keep wage growth to only 3.25% “for the good of the economy.” The market is still pricing in a very aggressive stance from the RBA and this brings the opportunity to bring some income into the portfolio at far higher yields than in recent history.

Higher interest rates are designed to drive demand lower taking some of the heat out of inflationary pressures. The higher rates force consumers to put off some consumption in order to pay the mortgage. The fine line a central bank runs is choking off demand just enough to stop inflation getting out of control without causing companies to pare back on hiring and investing or simply passing on higher borrowing costs to consumers.

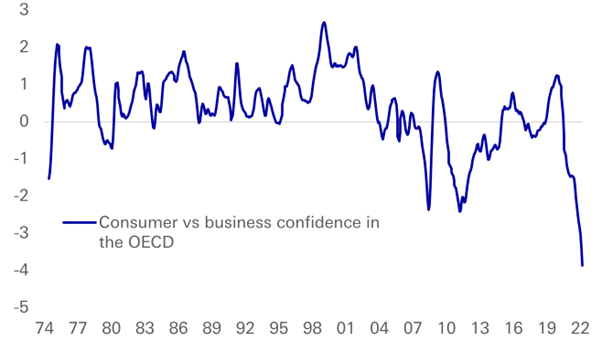

Key measures of future activity are business and consumer confidence data. Businesses currently feel much more sanguine about the future than consumers, in fact they have never seen such different prospects. The danger is businesses come closer to the consumer who are reporting the lowest levels of confidence in decades, even before the full effect of rate rises is felt.

Deutsche Bank, OECD, Haver Analytics

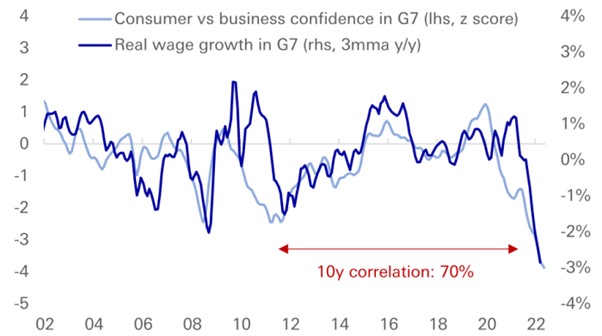

So the heavy lifting in this economic cycle seems to have already been passed to consumers who have taken the brunt of economic headwinds via falling real wages.

Deutsche Bank, OECD, Haver Analytics

Rate rises as sharp as those already baked into the market will do nothing but damage consumer confidence even further. A troubled consumer could accelerate the timing of the next economic downturn, usually a precursor to falling not rising interest rates.

Cash left on the sidelines in the hope of attracting better rates in the future has certainly been a good strategy for the last few months. The market has moved rates to a level more attractive than those seen for years. A known income and confidence of capital return should be a comfort and perfect timing is rare. On a risk-adjusted return basis Fixed Income can now play a leading role after being a bit player for the better part of a decade.

The views expressed in this article are the views of the stated author as at the date published and are subject to change based on markets and other conditions. Past performance is not a reliable indicator of future performance. Mason Stevens is only providing general advice in providing this information. You should consider this information, along with all your other investments and strategies when assessing the appropriateness of the information to your individual circumstances. Mason Stevens and its associates and their respective directors and other staff each declare that they may hold interests in securities and/or earn fees or other benefits from transactions arising as a result of information contained in this article.