“So shiny, my polyester girl”

Regurgitator [1997]

Real yields on 10-year US Treasuries hit -1% on Friday – a first for American history – indicating that an investor lending money to the US government (buying their bonds) would expect an after-inflation return of -1% p.a. for the 10-year period.

Ouch.

However, the rally in US bonds reflects investor’s readiness to pay-up for safe-haven assets as a surge in coronavirus cases threatens the country’s economic recovery.

Investors are obviously ready to receive a slightly negative inflation-adjusted returns, by buying Treasury bonds, rather than a perceived more negative return by buying other assets, thus deemed to be riskier.

Inflation-linked bonds

A real-yield is the inflation-adjusted yield of a nominal bond.

i.e. if you buy a bond at 2% nominal yield, and inflation is expected to be 1.5% for the same term, then your REAL yield is 0.5% (2 – 1.5).

However, there are specific bonds called “inflation linked bonds” or ILB, that are designed to help protect investors from inflation.

These ILBs are primarily issued by sovereign governments and are indexed to inflation, so that principal and interest payments rise and fall with the rate of inflation.

In the USA as well as Australia, these ILBs are linked to the Consumer Price Index (CPI), which was released last week in Australia and results found here.

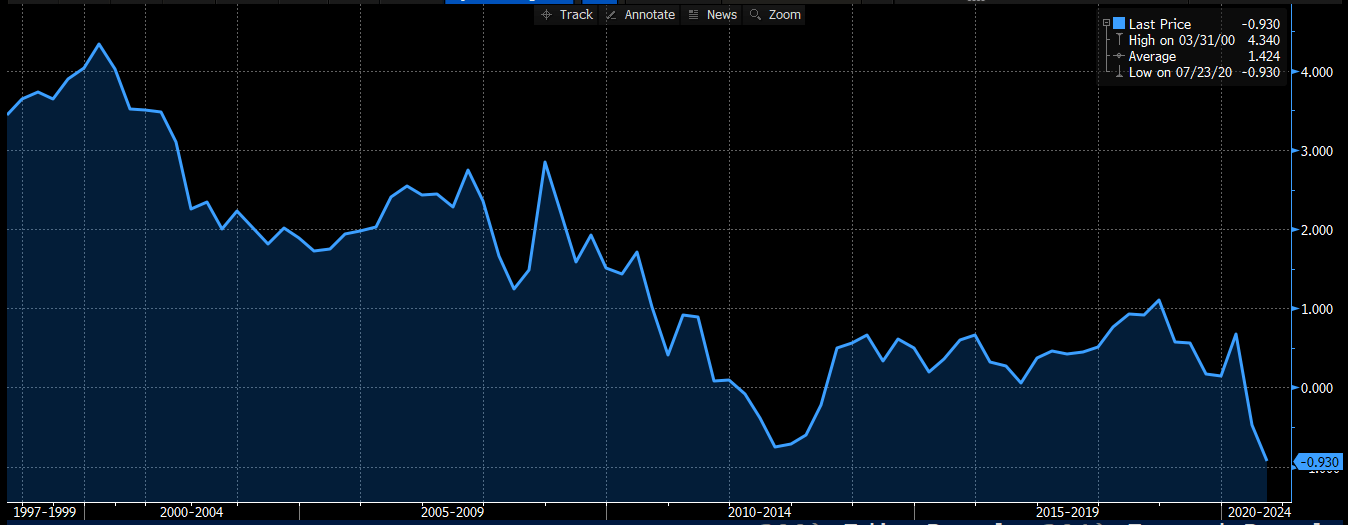

On Friday, the 10y ILB issued by the US Treasury traded at -1.0%, a first for the USA.

This compares to an average 1.4% real yield over the last 25 years.

Source: Bloomberg

Coupon Investing

Real-interest rates are a strong indicator for economies as they’re a key mechanism to price inflation expectations.

It’s no surprise that during COVID-19 there’s a demand deficit whilst no major reduction in supply, which leads to deflation.

Even last week, our ABS showed that Australian Q2 inflation was negative and the lowest result in 60 years.

In the USA, and most of the world right now, this is no different.

However, this also assumes that you’re a buy-and-hold investor and that inflationary pricing is accurate.

These two assumptions underpin real-yield and the inflation-linked bond market – and there is plenty of opportunity to trade-within the market as mis-pricings frequently occur.

In particular, I want to speak about buy-and-hold fixed income investors, who buy bonds simply for the income and not for capital appreciation.

Why buy Government bonds?

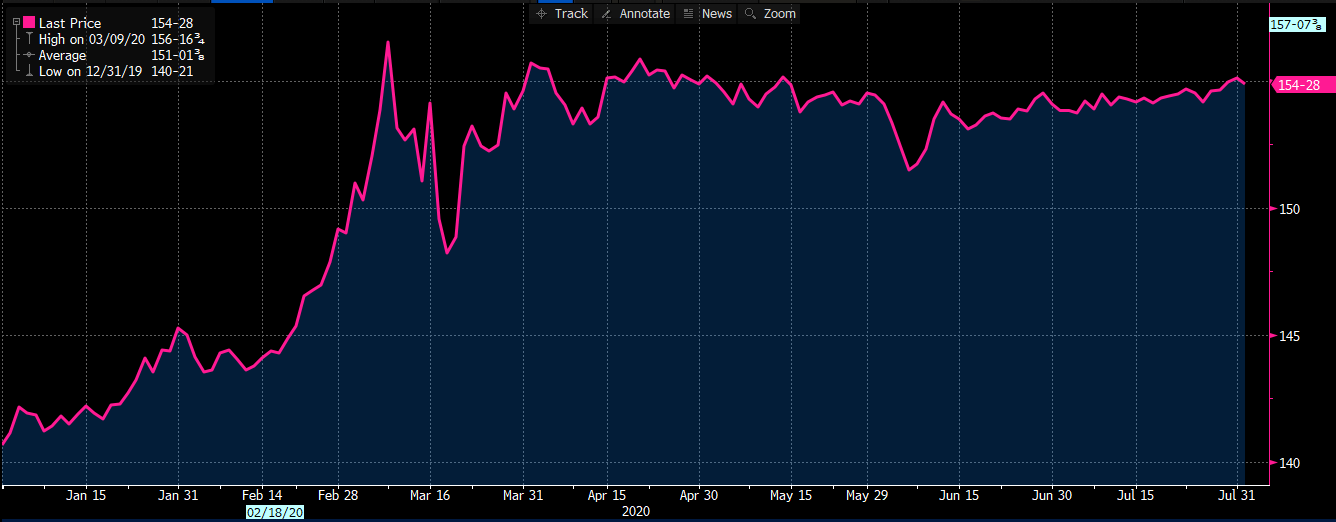

Whilst you may buy a 10-year US treasury and expect an inflation-adjusted return of -1%, you could make a similar case on 31 December 2019 when the real-yield was 0.04%.

However, if you bought the 10-year on-the-run US Treasury at the time, your security has appreciated +10% year to date.

Source: Bloomberg

And that is the answer – you buy safe-haven assets – even if they pay little to no yield– such as US Treasuries or gold – when you believe the price will go up.

Is the economy getting better or worse?

I write-this having seen the news of Melbourne City implementing increase lock-down restrictions and ponder whether we think the economy is going to improve from here or not.

Circling back to real-yields, there is a genuine market expectation for central banks to not raise interest rates for the next few years – 3 to 5 years – and the latest data releases show that economic activity is contracting.

US Federal Reserve Chair Jerome Powell said last week “the path of the economy is going to depend to a very high extent on the course of the virus and on the measures that we take to keep it in check.”

I believe that the future is uncertain and can fully appreciate investor rationale for buying safe-haven assets such as bonds and precious metals at this juncture.

The views expressed in this article are the views of the stated author as at the date published and are subject to change based on markets and other conditions. Past performance is not a reliable indicator of future performance. Mason Stevens is only providing general advice in providing this information. You should consider this information, along with all your other investments and strategies when assessing the appropriateness of the information to your individual circumstances. Mason Stevens and its associates and their respective directors and other staff each declare that they may hold interests in securities and/or earn fees or other benefits from transactions arising as a result of information contained in this article.