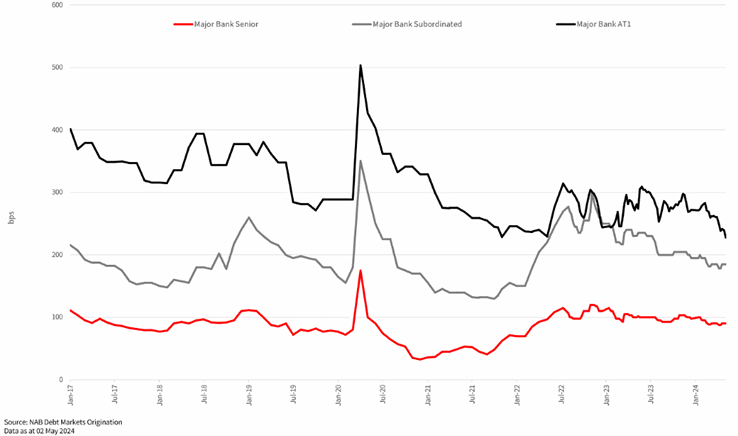

Movement in spreads

Hybrids (or ‘additional Tier 1’ ‘AT1’) as they are often referred to, sit at the bottom of a bank’s debt capital stack and one rung above common equity. They are designed to have characteristics of both debt and equity in the Australian market are often listed rather than OTC (‘over the counter’).

Australian bank debt ranges from Senior to Subordinated, to AT1 and as trading margins move these securities will usually maintain a similar average spread from each other to justify the additional risk. The below chart shows the moves in spreads over the past seven years. There is a fairly constant spread between Senior Debt and Subordinated (T2) over this period but you can see that this spread has reduced significantly in recent times for AT1 and to a lesser degree in T2.

AT1, Tier 2 and Senior Unsecured debt

A general rule of thumb previously has been that AT1s should trade roughly 100bps wider than T2 but that is clearly not the case currently. Some put this down to how high benchmark rates are at the moment and so investors are happy to accept that level of overall return. Other factors are lack of issuance and high scaling in new deals, retail investors limited access to OTC bonds higher up the capital stack and the benefits (perceived or realised) of franking credits.

Whatever the reason it is hard to see value when the AT1 vs. T2 spread is around 50bp or less, as it is now. However, it is about access and retail investors can’t always get the OTC versions of AT1, which often trade wider than their listed counterparts, or other parts of the market such as T2.

This is where it can be beneficial to get more selective on which listed hybrids you choose, and which part of the curve (i.e. 1-2 yrs to call versus 5+ yrs to call) and which names offer better value.

For wholesale investors it is likely an easier decision but either way there are always other options to consider.

Regulatory update

In September last year APRA released a paper discussing the challenges of using hybrids securities and announced they would be doing a review of the instrument. Part of the discussion centred around access of the securities to retail investors and listing on the ASX rather than only OTC markets, as most other fixed income instruments are.

They are “concerned that AT1 capital instruments would not operate as originally intended due to certain design features and market practices”. The purpose of AT1s is to absorb losses in the instance of a crisis. AT1s are the riskiest part of the banks debt capital stack, yet they are the easiest single-name, direct fixed income instrument for retail investors to access. The political sensitivity of bailing-in the securities only to be written off as equity holders shortly later and potential backlash, would likely be too large for policymakers to action.

APRA has since called for feedback from investors and bank representatives, and has been gathering information on the split between wholesale and retail investors in primary deals. APRA intends to formally consult on any proposed amendments to prudential standards this year.

Initial data, from what we are aware of thus far, is that there is less retail ownership as a percentage of total outstanding volume that originally thought. However, the number in dollars is probably still quite significant and may not deter the intention of the review.

A common thought is that if APRA did repeal access of bank and insurance hybrids for retail, it would be likely to be applied on new issuance only, with existing securities potentially grandfathered. The obvious implication for such a ruling would mean that liquidity in the listed hybrids market would become even thinner than it already is.

Implications for a ‘new’ style of hybrid remain unclear, for example what would it mean for franking and other features such as convertibility into shares. Parts of the wholesale market have little need for franking and would prefer cash, as per any other coupon paying bond in the OTC market, one might even say they would demand it.

Rating upgrade

In April, S&P Global upgraded all Australian bank AT1s and T2 securities whilst the Issuer ratings of the big four were unchanged. The upgrade was related to an improvement of their Banking Industry Country Risk Assessment (BICRA) rating which focuses on financial industry strength and macroeconomic factors. This puts Australis’s rating of 2 (very low risk) in line with Canada and Singapore. The resulted change is a move in Australian Major bank AT1 ratings moving from BBB- to BBB. Noting of course that listed hybrids don’t officially have a bond rating. The move also saw major bank T2 get upgraded to A- (from BBB+). Macquarie’s OTC AT1 bond also saw a move into the investment grade band to BBB- (from BB+). Spreads have rallied 10-30bp since, with a new investor base across life insurance and less rating restrictions overall helping the move tighter.

Issuance

Recent listed hybrid deals continue to be well bid. As a result we are seeing most new hybrid issuance pricing at the lower end of the indicated pricing range and new money being significantly scaled.

One of the most recent new deals was SUNPJ in which Suncorp came to market to raise $300m at a margin of 2.80% to 3.00%. This had firm demand in excess of $1.2bn and the deal was upsized to $360m and priced at 2.80%. New money was scaled back to 16% across the book. Prior to this, CBA redeemed their PERLS XI (CBAPH) without a new PERLS transaction. It is worth noting that they did issue two new AT1s at the end of last year to prefund.

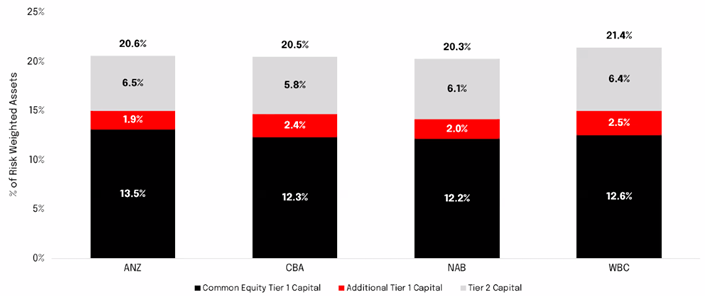

The chart below shows the current ratios of the Australian Major banks.

Source: NAB (CBA Basel III Pillar 3 Capital Disclosure reports as at 31 December 2023. NAB, WBC, ANZ Basel III Pillar 3 Capital Disclosure report as at 31 March 2024)

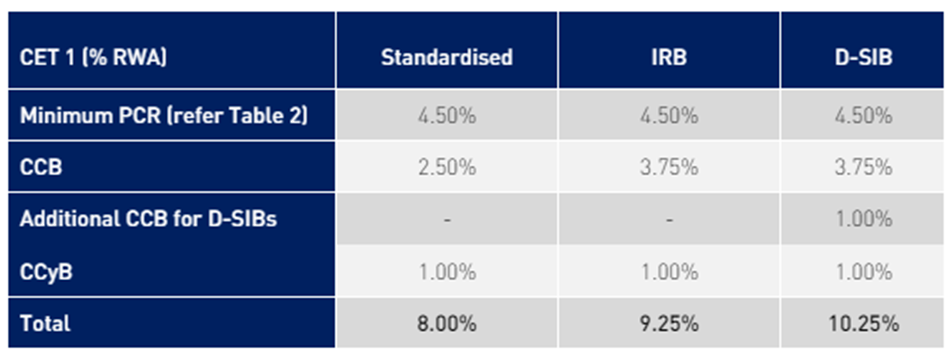

APRA currently requires minimum CET1 for the major banks of 10.25% which includes the capital conservation (CCB) and cyclical (CCyB) buffers as they are domestic systemically important banks (DSIBs). In addition total capital targets for the banks are 18.25% by 2026 which includes Tier 2 and AT1 of ~1.5%. When comparing the requirements with the current levels it is apparent that the major banks are well above their required levels. This reduces any immediate need to issue fresh AT1 capital and allows them to be more opportunistic with issuance.

Source: APRA APS110 Capital Adequacy

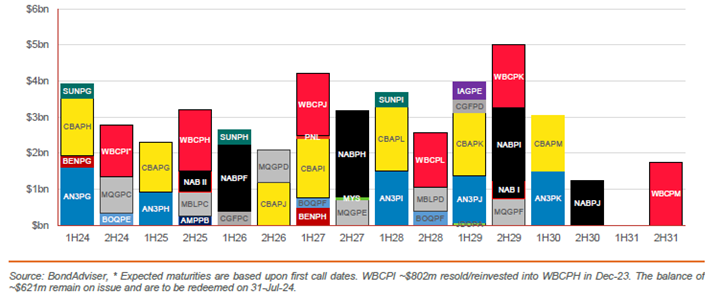

Upcoming maturities

The below chart provides indications of the upcoming maturities based on first call dates.

We have already seen AN3PG, BENPG CBAPH and SUNPG called. The next call date is WBCPI which has a call of 31 July 2024 followed by BOQPE on 15 August 2024.

The banks have been very cautious to space out their issuance to avoid having to come to market too frequently and avoid large maturity walls.

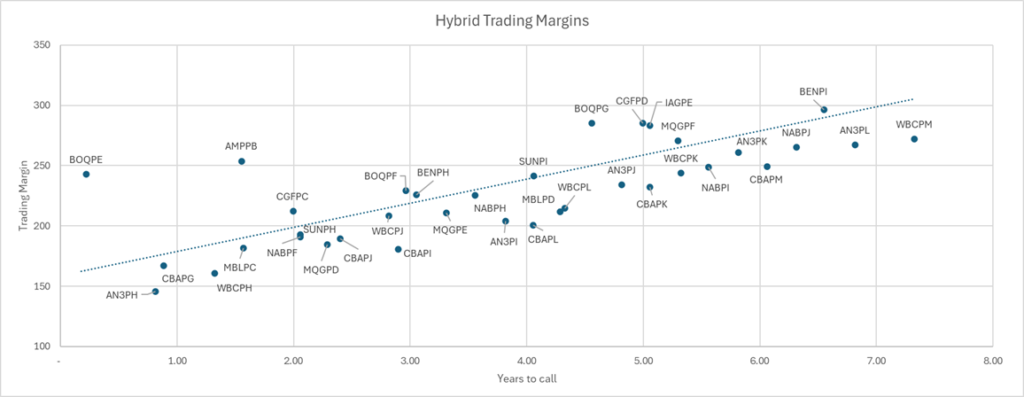

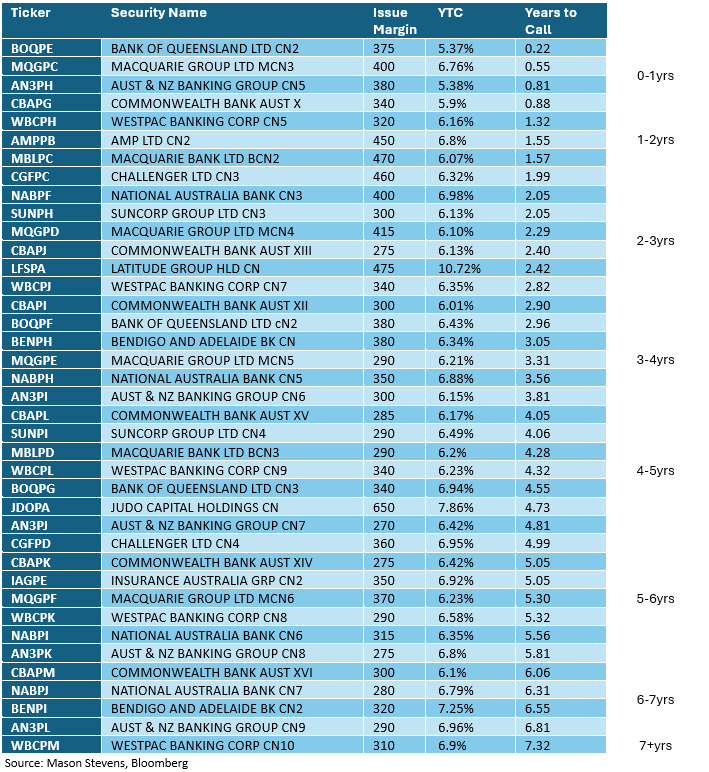

Hybrids relative value

The chart below is a snapshot of the trading margins (TM or spread) over the relevant swap rate to each call date of the indicated hybrids. Normally the regional banks would trade at a premium to the major banks, depending on the risk appetite of the market at the time. The insurers (e.g. IAG and SUN) also trade with a premium to the banks and can provide a good option for those that can get comfortable with the credit. Some investors prefer the insurers to regional banks and can benefit up to 50bp or more versus the major banks.

Source: Mason Stevens, Bloomberg

Another way to think about the relative value is to look at the short end versus the long end of the curve and especially when looking at the all in yield. Currently there are a number of hybrids trading around in the 5% to low 6% of yields (see YTC, yield-to-call), which some may say, doesn’t compensate the investor for the risk. For investors that still like the sector and are hold to maturity investors, one way to approach this would be to sell some of the short end names and buy into longer dated parts of the curve and reclaiming a more appropriate return of high 6% yields.

For more sophisticated investors there are a number of alternatives that are available for example in T2, e.g. CBA, WBC and Lloyds, where running yields of mid to high 6% can still be achieved, without the risk of hybrids.

Please feel free to reach out to the Fixed Income Desk at Mason Stevens to find out more.

The views expressed in this article are the views of the stated author as at the date published and are subject to change based on markets and other conditions. Past performance is not a reliable indicator of future performance. Mason Stevens is only providing general advice in providing this information. You should consider this information, along with all your other investments and strategies when assessing the appropriateness of the information to your individual circumstances. Mason Stevens and its associates and their respective directors and other staff each declare that they may hold interests in securities and/or earn fees or other benefits from transactions arising as a result of information contained in this article.