Today I wish to channel Chubby Checker’s 1960s hit Limbo Rock.

As government bond yields head towards recent lows and some countries (ergo: Australia) are at all-time lows, it’s time to explore the possibility of long-term bond issuance as a benefit to the Australian public, funding infrastructure with ankle-high hurdle rates.

The topic is somewhat mundane, but as other countries are issuing ultra-long bonds (30 years or more) to secure funding and minimise costs to their taxpayers, Australia sits on the sidelines.

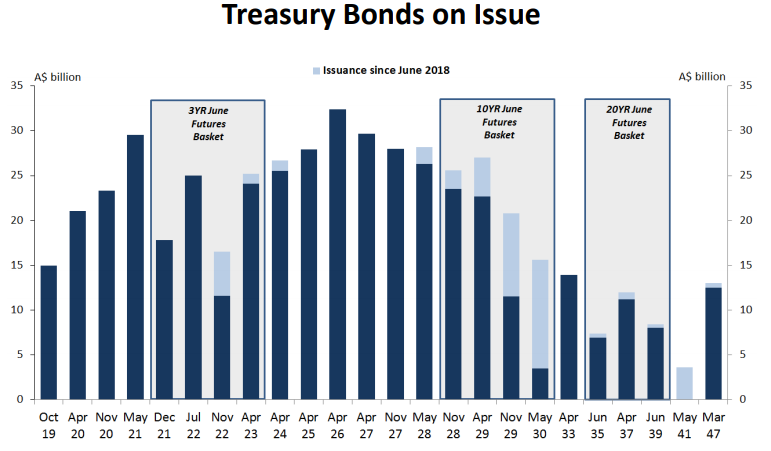

The Australian Office of Financial Management (AOFM), the department of the Treasury that issues Australian’s government debt, has just over 540 billion AUD of debt on issue, not including State and Local government debt. With a material portion of this rolling over in the next 3-5 years (see graph from AOFM website below), the AOFM has the ability and opportunity to lock in low rates for future generations.

Source: Australian Office of Financial Management (AOFM)

Let’s analyse the benefits for all of us:

Locking in low rates

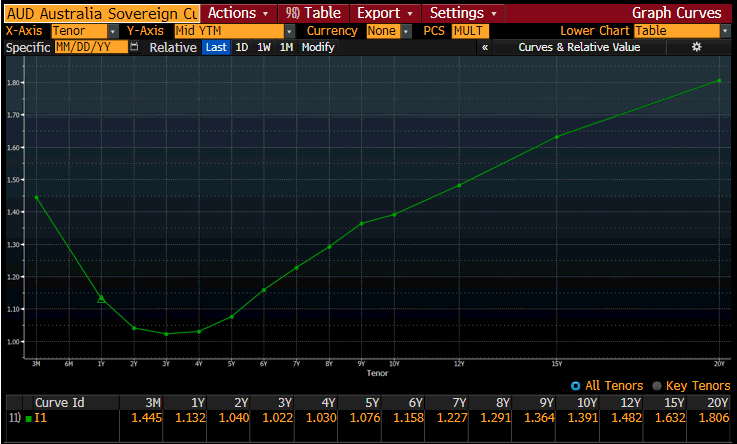

The easiest argument is the most salient. Issuing bonds 30-50 (or possibly 100 years) locks in a super deal for the Australian tax payers. Consider that the current benchmark Aussie 10y government bond is at 1.39% and the 20y is at 1.79%. Consider that since Federation, the average Australian 10y bond yield has been over 6%.

Today’s yields can go slightly lower, but can go much, much higher!

Source: Bloomberg

Locking in low rates may be self-validating

Selling long term debt can be seen as a directional bet on markets – that you’re hedging the risk of higher rates by locking in lower costs on a significant share of government debt. One would argue that it’s in tax payer’s best interest to lock in fixed costs for interest outlays as this can allow for more forward thinking and stable tax policy.

I can foresee the possibility of a fiscal/government debt catalyst for the next crisis. While G10 nations have a remarkable privilege to run budget deficits, at some point this may change. Locking in low rates is a hedge against a hypothetical future debt crisis.

Asset to Liability matching

My last argument for issuing long bonds is derived from an old axiom of financial theory – you maximise efficiency and minimise cost by matching the duration of assets and liabilities. This can be a very in-depth topic, but I’ll keep it short: a low yielding 50 year government bond may be the ideal way to fund a 50-100 year bridge, port or railyard – rather than a 10 year loan rolled over 5-10 times.

Countries that have already taken advantage of lower rates in the last two years:

50 year bonds

Canada (CAD) 3.0%

Italy (EUR) 2.9%

Britain (GBP) 2.6%

France (EUR) 1.9%

100 year bonds

Mexico (EUR) 4.2% >> not a typo, was issued in EUR rather than MXN

Ireland (EUR) 2.4%

Belgium (EUR) 2.3%

Summary

The world is moving this way as seen by the numerous countries above extending the tenor of their government borrowings. Governments, insurance companies, state treasuries, local councils, multi-national development banks; all have long liability profiles as they build and develop the world for generations to come.

Next week we’ll extend this argument and discuss how we can take advantage of this for investment.

The views expressed in this article are the views of the stated author as at the date published and are subject to change based on markets and other conditions. Past performance is not a reliable indicator of future performance. Mason Stevens is only providing general advice in providing this information. You should consider this information, along with all your other investments and strategies when assessing the appropriateness of the information to your individual circumstances. Mason Stevens and its associates and their respective directors and other staff each declare that they may hold interests in securities and/or earn fees or other benefits from transactions arising as a result of information contained in this article.