Times are rough, but we can make it,

We can work it out

How can we be lovers if we can’t be friends?

How can we start over if the fighting never ends?

Michael Bolton (1989)

This week is all about the RBA and GDP.

On Tuesday we had the RBA September meeting and then yesterday we had the Australian Bureau of Statistics (ABS) release Q2 2020 GDP figures.

Very exciting.

Today we will keep things short and sweet and speak to the facts underpinning the current state of the Australian economy and how our decline in economic growth is being softened by a monetary policy cushion.

Gross Domestic Product (GDP)

[all figures quarter on quarter change]

Gross domestic product or GDP is a measure of the change in economic activity from one period to another.

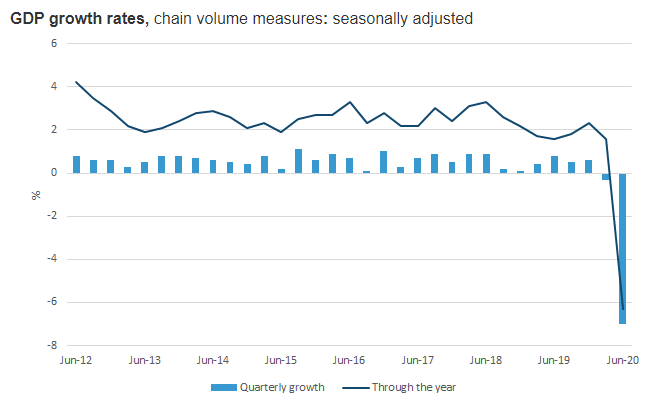

In the release of Q2 GDP figures yesterday, our level of economic output was negative – we produced LESS output than the previous period (Q1) and less than in Q2 2019.

The result was a 7% fall in economic activity from 31 March to 30 June 2020.

Source: Australian Bureau Statistics

This was intuitive, as the sheer volume of workers not working during this pandemic was going to produce a decline in economic activity.

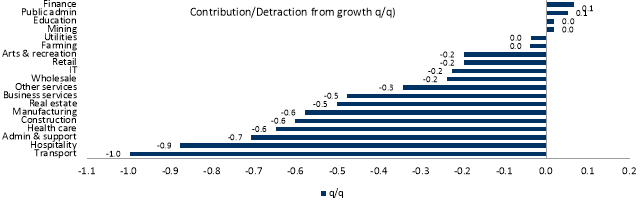

Household consumption declined 12.1%, which was 95% of the overall decline in GDP and was largely concentrated in a collapse by services expenditure (-17.6%).

Private demand was also negative at -6.8% and -4.8% fall in business investment.

Business also decreased their inventory levels which saw another -0.6% decline in activity.

Source: RBC Capital Markets, ABS

This result also cements that Australia has entered its first recession since 1991, two consecutive quarters of negative economic activity (Q1 and Q2).

Savings rate

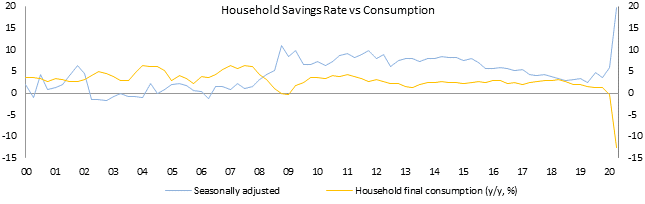

The national household saving ratio spiked from 6% to 19.8% – something we expected and have mentioned here and here.

This represents that Australian families are uncertain regarding their futures and are thus saving an increased portion of their income.

When we view less lagged data publications, such as APRA Monthly Banking Statistics, we know that this “precautionary savings” trend has continued in July and August, and will likely see a higher savings rate published in Q3 GDP, when it is released in November.

When the level of uncertainty decreases through declines in COVID-19 infection rates and businesses can return to more normal operations – this cash hoard may start to be spent as life returns to normal (maybe a new normal).

Businesses that rely on consumption expenditure will target this cash, appealing to households’ spending habits, whilst investment managers and wealth advisors will seek to manage these savings in new advisory or investment management opportunities.

However, as we analysed in our Study of Pandemics: historically “precautionary savings” remain elevated for some years as vaccines have not been quickly developed during past pandemics, and uncertainty remains high for several years.

Source: RBC and ABS

The RBA

The RBA met yesterday and kept current policy in place, while extending the Term Funding Facility (TFF), which I will get to in more detail shortly.

The Bank mentioned that the economy is being supported by substantial and coordinated policy from State, Commonwealth governments and the RBA.

Moreover, the RBA mentions that our public sector balance sheets are still in good shape, which allows for continued support.

One of the private sector support mechanisms is through Australia’s financial institutions, which maintain robust balance sheets and high levels of liquidity, also provided to them by the RBA.

Term Funding Facility (TFF)

The TFF was announced on 19 March 2020 as part of a package of measures from the RBA to support the economy.

Under the TFF, the RBA will offer three-year funding to authorised deposit-taking institutions (ADIs) (think banks, mutual banks, credit unions, building societies etc.) through repurchase (repo) transactions at a fixed pricing rate of 0.25% p.a.

The TFF has two objectives:

- Reinforce the benefits of the lower cash rate (0.25%) by reducing funding costs to ADIs to reduce interest rates for borrowers

- To encourage ADIs to support businesses by lending to them during this period, as additional funding will be provided to the ADIs in future that lend to small- and medium-sized enterprises (SME)

On Tuesday, the RBA announced a “supplementary allowance” equivalent to 2% of the ADIs outstanding credit, on top of the existing facility, and a three-month extension to draw down on the facility (i.e. ADIs are now able to drawdown on the TFF until 30 June 2021 and have an additional 52bln AUD to borrow, taking the total TFF to $200bln AUD).

Less need to issue bonds

As banking institutions have more access to funding through the RBA, as well as the current increased deposit funding they are receiving, they have less need to issue new debt through the bond market.

There is approximately 21.8bln AUD of senior unsecured bank debt maturing before 30 June 2021.

With less forthcoming supply, we note that anecdotally, the secondary bond market (post primary tender) has seen increased demand for existing debt securities, underpinning the Australian credit market’s recent rally in June-August period.

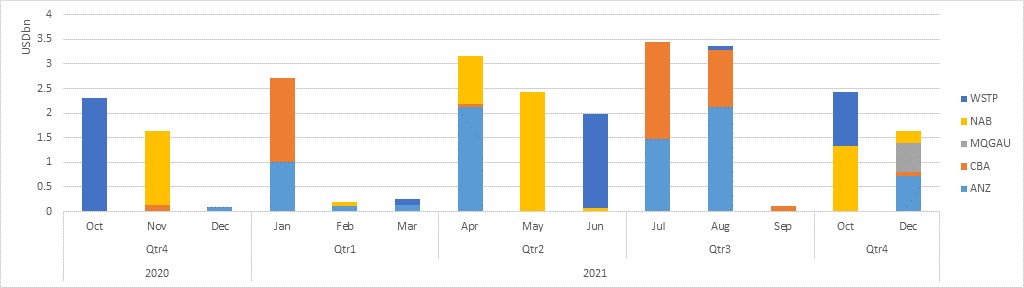

The below chart shows Major Bank + Macquarie senior debt maturities until 31 Dec 2021.

Source: HSBC

Closing remarks

All in all, no real surprises from the RBA or the ABS, with COVID-19 deeply affecting the domestic and international economy.

We continue to pay attention to monthly employment statistics and weekly/fortnightly household and business surveys that depict uncertainty/certainty levels.

When we begin to see a sustained turn-around in employment and those employed persons begin to deploy their savings, then we can price in a return to economic productivity and economic growth that will not be debt funded.

The views expressed in this article are the views of the stated author as at the date published and are subject to change based on markets and other conditions. Past performance is not a reliable indicator of future performance. Mason Stevens is only providing general advice in providing this information. You should consider this information, along with all your other investments and strategies when assessing the appropriateness of the information to your individual circumstances. Mason Stevens and its associates and their respective directors and other staff each declare that they may hold interests in securities and/or earn fees or other benefits from transactions arising as a result of information contained in this article.