Yesterday, I had the opportunity to speak on a panel discussion hosted by the Institute of Managed Account Professionals (IMAP) regarding what zero% interest rates mean for managed account investing, and how we should invest in defensive and income bearing assets going into the future.

The discussion was enlightening, as I was joined by two investment experts – Michael Karagianis from JANA Investment Advisors and Michael Frearson from Real Asset Management – and together, we were able to share our thoughts regarding the topic and remarkably with very little disagreement, though nuanced differences in opinion.

Where to begin?

As always, we must remember why fixed income is considered a defensive asset allocation.

Fixed income securities, those that pay scheduled income streams, have been a long-term component of multi-asset portfolios because of their:

- Liquidity

- Income

- Diversification benefits compared to equity risk premia

However, as central bank cash rates have neared zero%, the income component of “core bonds”, which historically referred to government bond holdings, has declined to levels below investor objectives.

For example, as the RBA Overnight Cash Rate (OCR) was decreased to 0.25% in March this year, with our 3y Commonwealth government bond yield also targeted at 0.25%, the income net of fees and taxation was near zero% or negative.

The liquidity and diversification benefits are still there, but the lack of income has seen investors take increased interest rate exposure (longer term bonds) or increased credit exposure to achieve similar return objectives.

Components of return

There are two main components of fixed income price movements – a bond’s sensitivity to:

- Interest rates

- Credit risk

As market interest rates – such as government bond yields – are near zero%, there is little capital upside for core bonds with the RBA explicitly stating they are unlikely to move the OCR to a negative rate.

This means we’re increasingly dependent on credit spreads – the premium demanded by investors to lend to corporates – as opposed to “risk free” government bonds.

I.e. how much extra compensation for lending to Westpac as compared to the Commonwealth Treasury.

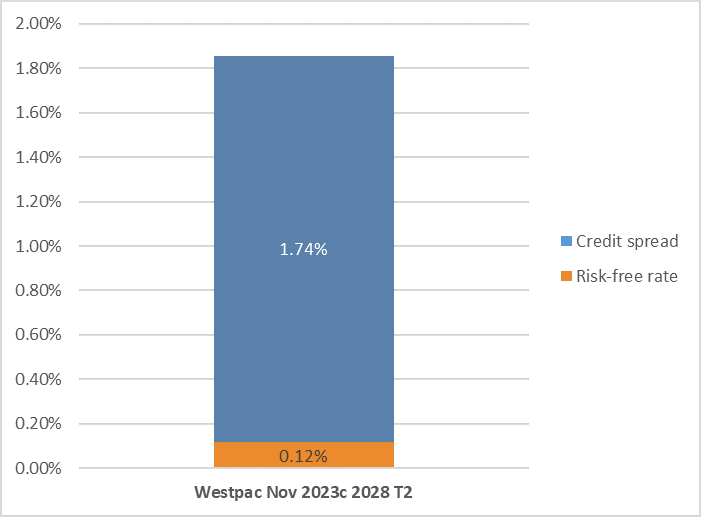

In the below chart, I depict the interest rate component in orange, and the credit component in blue of a Westpac AUD subordinated bond, 1st callable in November 2023.

The interest rate is based on our 3y government bond yielding 0.12%, and the credit premium for lending to Westpac is 1.74%, together totaling a yield to call (YTC) of 1.86%.

Source: Mason Stevens, Bloomberg

Credit, rather than Interest Rates

Credit is going to be the main source of future returns in fixed income investment, and we’re already seeing more and more money allocated to this area within the broader fixed income market.

However, we need to be wary of the trade-off.

As we seek to increase the income of our fixed income investments above government bond yields, we have a trade-off through diminished liquidity and lower diversification benefits compared to equity risk premia.

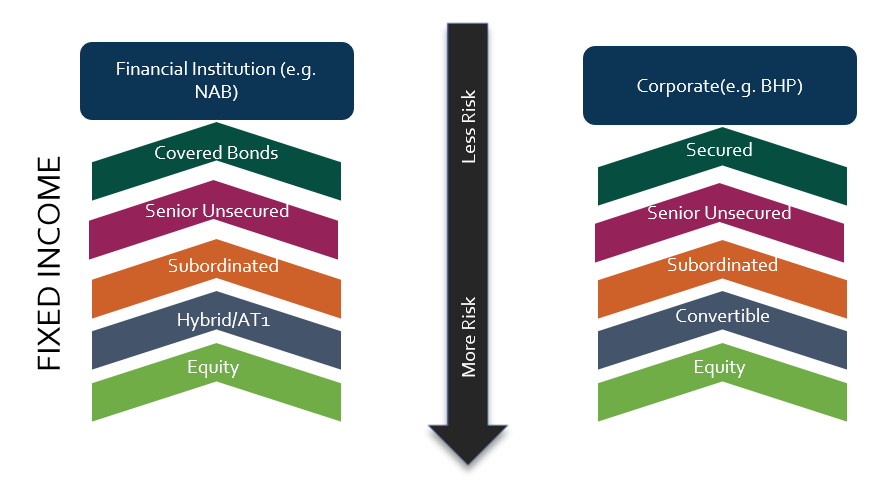

Below, I show what’s known as a “capital structure”, which depicts the different ranks of debt obligations within a corporate’s balance sheet.

Source: Mason Stevens

Higher-ranking bonds, such as secured debt and senior debt, have generally less risk and are less correlated with equity markets.

Lower priority bonds, such as convertible debt and bank issued hybrids, are more correlated with equities, thus losing the diversification benefits. They’re also generally less liquid due to less wholesale market participation as hybrids are generally not rated by credit rating agencies.

In the below chart, I show the change in a Westpac hybrid (WBCPF, in red) with a Westpac senior bond (in black) maturing in November 2023.

The WBCPF hybrid sold-off ~11% in March before recovering 6-7%, while the Westpac senior bond sold off 1% before rallying 4%.

Source: Bloomberg

What investors are doing is utilising these different fixed income securities of various capital status – senior, subordinated, hybrid etc – and blending portfolios to achieve their desired income goals, but with known reductions in liquidity and diversification.

Domestic opportunities

The lower for longer interest rate environment doesn’t mean there aren’t opportunities.

In fact, from an active point of view and quoting Top Gun – the current market is a “target rich environment” because the market dislocations from COVID have presented opportunities to asset managers such as us (Mason Stevens).

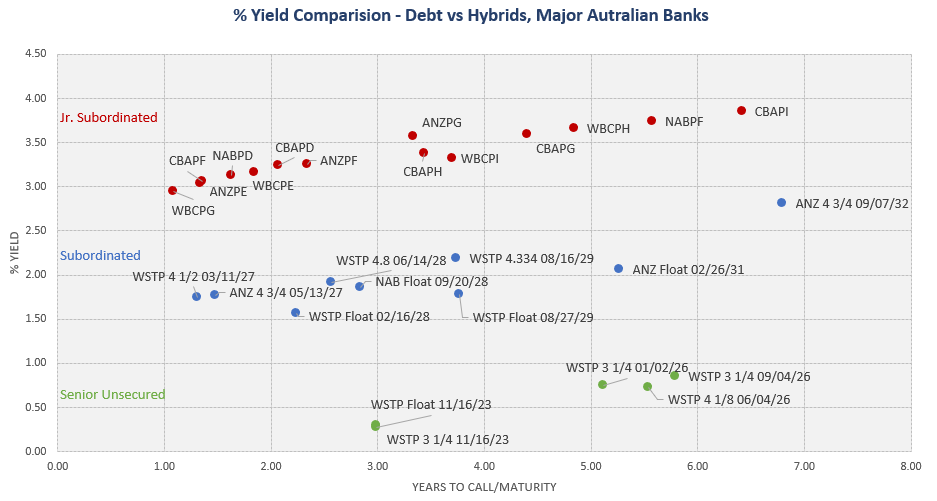

For example, the below chart categorises opportunities in the AUD credit market with a snapshot of Australian Major Bank issued bonds.

Red is their junior subordinated debts, or hybrids.

Blue is their subordinated debts, more senior than hybrids and with a higher rank.

Green is their senior unsecured debts, more senior than subordinated debts and with yet again a higher rank.

Senior major bank bonds have limited capital upside because of their proximity to zero% yield, even buying longer term bonds greater than 5 years to maturity presents little better opportunity with extra risks for making a longer-term investment.

Source: Territory Funds Management, Bloomberg

Therefore, the domestic opportunities are in specific subordinated and hybrid securities, where the risk-return profile is compelling.

In particular, we see value in major bank issued subordinated debt and hybrids, because of the strong and improving balance sheets boasting high capitalisations and entrenched businesses with stable market shares and revenue streams.

This doesn’t mean all subordinated securities or hybrids are favourable investments, but they’re a good place to start.

International opportunities

International fixed income is generally a currency hedged investment, where the currency can gyrate more than the capital price of the bond investment.

Assuming a stable currency, USD bonds compare well with AUD equivalents because of the broader participation of American corporates in their bond markets.

In Australia, our banking and insurance companies are well established bond issuers, but many of our non-financial corporates continue to prefer bank loans rather than bond issuance.

In the USA, in contrast, there is a much greater industry exposure through bond market participation of oil and gas, logistics, transport, telecommunications, technology and consumer cyclical companies, that create a well-rounded market.

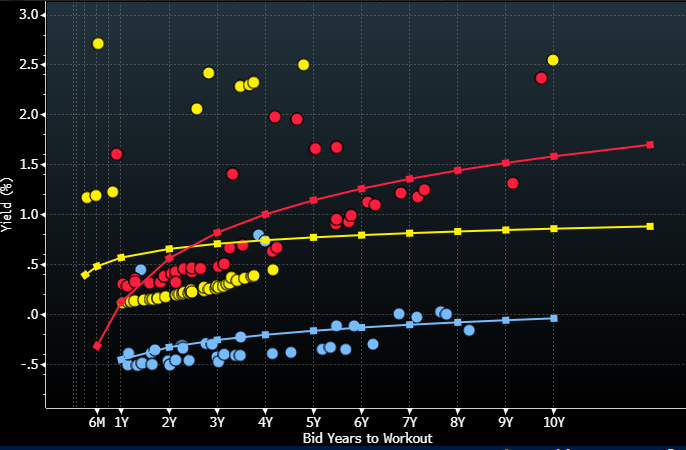

In the below chart, I again compare Australian major bank issued debts, this time in multiple currencies: AUD (yellow), EUR (blue) and USD (red).

Source: Bloomberg

There are opportunities to buy USD debts of comparable nature to AUD equivalents; as at various points along the yield curve, USD and AUD bonds differ in value.

AUD subordinated debt yields higher than USD, but USD senior debts yield higher than the AUD equivalents.

Summary remarks

We need to be increasingly aware of our fixed income exposures – of the intricacies of credit exposure, interest rate exposure and relevant macro-economic factors – so that we can position accordingly.

We also need to be cognisant of our capital status, so that we can build truly diversified portfolios that balance income, liquidity and defensive characteristics.

All in all, investors in fixed income have had more reason to pay attention to their allocation, to determine if their current holdings reflect their desired outcomes – and now is an opportune time to plan and invest for the future.

The views expressed in this article are the views of the stated author as at the date published and are subject to change based on markets and other conditions. Past performance is not a reliable indicator of future performance. Mason Stevens is only providing general advice in providing this information. You should consider this information, along with all your other investments and strategies when assessing the appropriateness of the information to your individual circumstances. Mason Stevens and its associates and their respective directors and other staff each declare that they may hold interests in securities and/or earn fees or other benefits from transactions arising as a result of information contained in this article.