Last week, I had the opportunity to speak at portfolio management conference held by IMAP – Institute of Managed Account Professionals, on the topic of “Embedding ESG in Fixed Income Portfolios”.

I was lucky enough to be joined by Shan Kwee, a senior portfolio manager at Janus Henderson, with our session moderated by Angela Ashton, founder of Evergreen Consultants.

It’s a bit of a treat to speak about ESG fixed income investing in the AUD landscape, because it’s still a relatively small market for ESG-bonds, certainly when compared to the EUR, GBP and USD markets, where their markets blossomed much sooner than the AUD version.

And it was a treat in that I had the chance to speak on a topic that’s close to my heart with the ability to voice both the frustrations at lack of progress to a functional ESG-bond market, as well as the positives that have developed in recent history.

What is ESG-FI?

ESG, referring to Environment, Social and Governance, is by no means a new concept in investing, though the acronym has received more popularity in recent years.

ESG is the new term that reflects collective psychology regarding responsible and sustainable investing practices, where there’s a growing trend towards qualifying and quantifying investment objectives and measuring impact towards these goals.

For many, the United Nations’ Sustainable Development Goals (SDGs) are the key criteria, though many have their own more nuanced, or refined, or short-listed goals they seek to meet through investing.

In the context of fixed income and debt capital markets, ESG is nothing new to lenders; as monitoring a business or government entity for environmental risks or governance issues is prudent lending, incorporating those risks into the price of a loan.

One step further, ESG-bond investing can be considered a pure play strategy to qualify or quantify responsible investing, where a bond buyer (lender of capital) can purchase bonds that actively finance green, climate, sustainability, social and other ESG-linked activities or agendas.

This contrasts with equity capital markets where there’s very little pure play ESG-linked companies.

AUD ESG-FI Landscape

As at 31-Dec-2021, there was 54bln AUD of outstanding ESG-linked bonds, across 60 different debt issuers, with more than 160 bonds outstanding.

These bonds were issued to fund various assets and ESG objectives, ranging from carbon abatement, other climate actions, sustainable housing and business, cleaner water, rural education as well as international programs to lower poverty rates globally.

These bonds – depending on the underlying assets – are called “green”, “social”, “climate”, “sustainability” bonds, where each bond and bond label is specific in its objective.

As is the case for the non-ESG bond market already, OTC bond issuance tends to only come from the largest corporates, governments or multi-national entities, where smaller companies, charities or government entities tend to use bank loans instead.

This is the case for ESG-bonds as well, but even more so, given the burden of documentation required to certify a bond as “ESG”, and the legal and accounting assurance costs to re-certify the bonds each year.

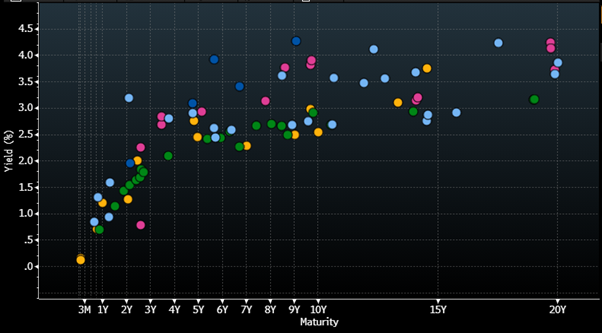

In the below graph, each dot represents a unique bond issued, where we’ve coloured the market by credit rating, and you’ll notice there are less BBB securities compared to higher rated AAA or AA rated bonds.

Chart 1: AUD ESG-Linked Fixed Income Securities

Source: Bloomberg, as at 11/March/2022

What do ESG-Bonds Finance?

As mentioned above, ESG-linked bonds can finance a range of objectives and must meet International Capital Markets Association (ICMA) guidelines, in order to be certified as ESG.

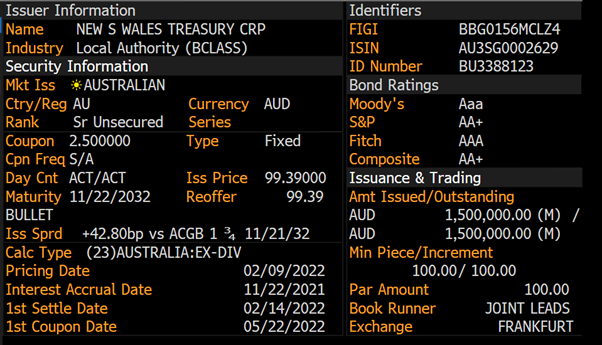

As an example, we can analyse NSW state’s debt issuance agency, NSW Treasury Corporation (“TCorp” for short).

TCorp has a “Sustainability Bond” programme, which they can use to finance bonds supporting environmental and social policy goals.

TCorp have a:

- Climate Change Policy Framework

- Resource Efficiency Policy

- Premier’s Priorities; and a

- Net Zero Carbon Emissions Plan

In order to reach the objectives of the above documents, TCorp issued 1.5 billion AUD of “sustainability” bonds on 9/Feb this year, maturing in November 2032, paying a 2.5% coupon semi-annually.

Chart 2: Screenshot Summary of TCorp 2032 Sustainability Bond

Source: Bloomberg

As for the proceeds of this loan, TCorp are funding projects such as:

- Public school infrastructure

- Social housing maintenance

- Johnston’s Creek stormwater naturalisation

- Parramatta and Sydney CBD light rail; and

- Sydney Metro Northwest link

Where each of these assets are eligible under the ICMA Green and Social Bond Principles of:

- Clean transportation

- Affordable basic infrastructure and housing

- Sustainable water; and

- Access to essential services

The nuance to these bonds is that bond issuers (such as NSW TCorp) can add or subtract assets from the designated pool each year.

For example, if NSW government privatised the Sydney CBD light rail and the assets moved off their balance sheet (and onto a private business’s), then they would remove the asset from the bond’s sustainable asset pool, and likely add in another asset (if possible).

This might then unalign with an investor’s objectives, depending, and they may need to sell the bond if so.

Come back to my earlier point about resources, the above example is but one bond from one issuer, which goes to show how much documentation investors need to be across, as well as periodically reviewing the updated assurance documents for any changes in the bond’s underlying assets.

ESG Policies

The rise in ESG-bond issuance, where over 20bln of the 54bln AUD outstanding has been inn the past 15 months, has seen bond fund managers increasingly publish their own ESG policies online, for the world to see what their objectives are (if that detailed).

For example, if you were to Google search any large fund manager and the keywords “ESG Policy” at the end, you’re likely to find their policy.

For example, I just googled “PIMCO ESG Policy” et voila!

Part of this transparency trend has been to promote visibility of ESG mandates, objectives and approaches, and partly to show bond issuers there’s ample demand for ESG-linked bonds from investor cohorts.

If I’m being fair, there’s likely a portion of investors using their ESG policy or public mandates to secure allocation of new ESG-linked bonds, as preference is given for ESG-investors compared to non-ESG aligned investors.

ESG Ratings

Tying my resource and expertise comments from the TCorp example together with the practical implications of this note; it’ll come as no surprise that the market has moved towards ESG ratings the same way it utilises credit ratings to assess probability of loss and probability of default (basically, credit risk).

But in this case, ESG risk or ESG merit.

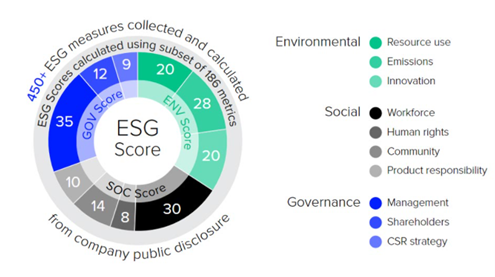

Below is a graph created by Refinitiv (formerly Reuters), about their ESG scoring system.

Chart 3: Example ESG Scoring Method

Source: Refinitiv

On this front, there are numerous global providers of ESG data, assessment and ranking methodologies; such as MSCI, S&P Global, Bloomberg, ISS, CDP that provide government entity or company level assessment, whilst there are also providers such as Evergreen Consultants and Zenith who rank fund managers and ETFs on their responsible investing practices, as well.

For example, when I search for NAB equity on my Bloomberg terminal, I can view an aggregation table across various ESG data providers, and a comparison against comparable securities (companies) such as BoQ, Westpac, CBA, ANZ, Bendigo and Adelaide Bank.

Chart 4: Bloomberg Aggregate ESG Scores Table

Source: Bloomberg, as at 9/March/2022

Where MSCI uses a methodology similar to a credit rating, where top rated entities have a AAA>AA>A>BBB>BB etc scoring, others such as S&P or Sustainalytics use a 1-100 scoring.

A Question of Alignment

We can foresee a big push for investors in using ESG ratings to assess their own investment holdings.

This won’t be just direct fixed income, likely this is all encompassing across FI, equities, managed fund holdings and ETF positions.

Hence, investors likely need 1 or 2 data providers or access points so that they can obtain ratings for both companies (direct investments) as well as investment vehicles (such as managed funds, ETFs, LICs, LITs).

This is a pathway I must emphasise is a difficult one to navigate, as there might well be no alignment between your objectives and the ESG rating agency’s methodology or approach.

As an example, one large provider of ESG ratings uses a methodology that focuses on ESG-related risk, and whether that risk will have an economic impact on the company.

For example, when a large global mining company destroyed an Aboriginal sacred site in 2020, that company saw no move in their ESG rating, because there was no economic impact on the company, only a social/political reaction.

For us, this highlighted the disconnect between that ESG rating methodology and our own investment objectives.

Looking Forward

For me, I’m looking forward to the development of many areas of the above, that’ll ultimately improve the function of our local sustainable capital/responsible investing market.

As a bond investor, we appreciate the greater disclosure and transparency we’re receiving from bond issuers, where there’s now some ~1400 new data points on ESG-related factors we can model against and find trends to better assess credit risk.

ESG-linked bonds also provide pure-play ways to provide positive capital as well, something that we can’t stress enough, where we’re able to then qualify and quantify the value of that capital’s impact on certain objectives.

Otherwise, we’re looking forward to the increased savvy of ESG rating approaches, where new tools are continuing to be built to allow investor objectives to be aligned to the way ratings are assessed.

The views expressed in this article are the views of the stated author as at the date published and are subject to change based on markets and other conditions. Past performance is not a reliable indicator of future performance. Mason Stevens is only providing general advice in providing this information. You should consider this information, along with all your other investments and strategies when assessing the appropriateness of the information to your individual circumstances. Mason Stevens and its associates and their respective directors and other staff each declare that they may hold interests in securities and/or earn fees or other benefits from transactions arising as a result of information contained in this article.