Credit spreads represent the difference in yield between the relevant benchmark (usually government bonds) and the yield of another non-government debt security of the same maturity.

They reflect the risk premia which investors apply to the debt of the issuer, relative to government debt.

They make up one of the main components of fixed income markets – the other being the interest rates of benchmark securities.

Within equity markets, the focus lies primarily on the cash flows of a company, however, in credit markets, the focus is placed on the likelihood of that company being able to service interest payments and repay debt.

As a result, the underlying concerns are considerably different when compared to equity markets, with other factors such as levels of issuance also playing a role on relative valuations through the forces of supply and demand.

As interest rates have gone to record lows, investors have begun to allocate more funds towards credit, and in particular, investment grade (IG) credit.

This has been a result of the declining rates of return available within government bonds, which have historically been used by asset allocators as a vehicle to attain the diversification benefits offered by fixed income.

This has made credit increasingly more important within asset allocation discussions, with this importance likely to remain over the coming years given the intention of central banks to maintain current interest rate settings for at least the next 2-3 years.

In today’s note, we will cover how credit spreads function, their importance, and their performance since the onset of the COVID-19 pandemic.

How Do Credit Spreads Function?

Credit spreads reflect the difference in risk exposure when investors lend to corporate issuers, as opposed to the government.

Source: Mason Stevens, Bloomberg

They are influenced by multiple factors, including the credit risk (reflected through credit ratings), liquidity (those investing into more illiquid issues will demand a liquidity premium), and company-specific balance sheet and earnings metrics.

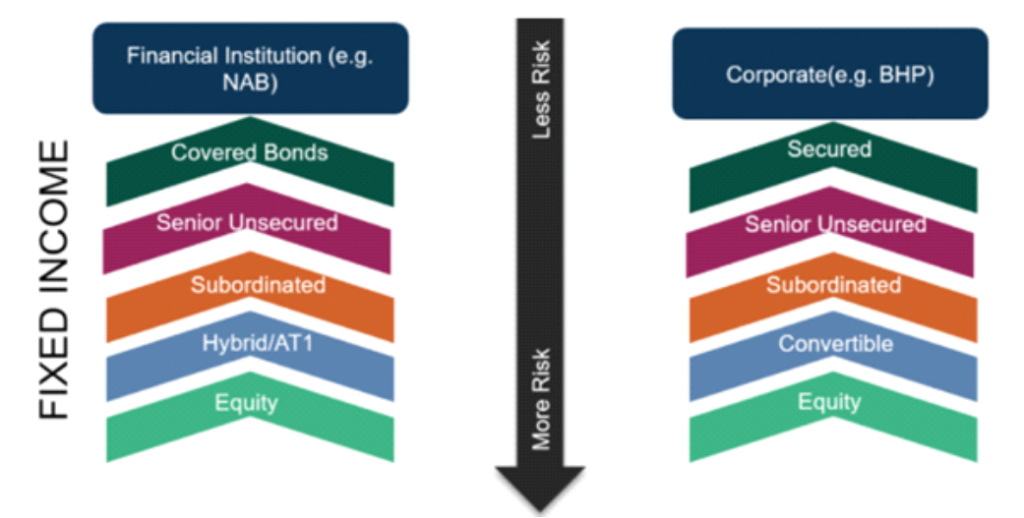

Levels of credit risk are also determined through capital structures – which signify the payment rank of a debt investor in the event of a default.

Investors in lower-ranking debt are compensated by an elevated credit spread, given their reduced likelihood of repayment in the event of a default.

Source: Mason Stevens

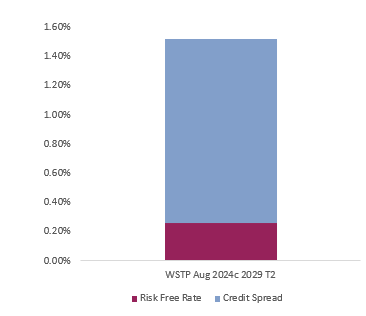

As interest rates have declined to all-time lows, credit spreads have taken on a greater proportion of fixed income returns.

In 2016, where the RBA Cash Rate was 2.25%, and 10-year government bond yields were 3.03%, investors were better able to meet return objectives merely through investing into government bonds, however this is less possible now with the RBA Cash Rate at 0.03%, and 10-year bond yields of ~1.35%.

As such, fund flows have increased into corporate credit, and particularly within IG issuers, which still offer diversification benefits, without taking on considerable additional risk.

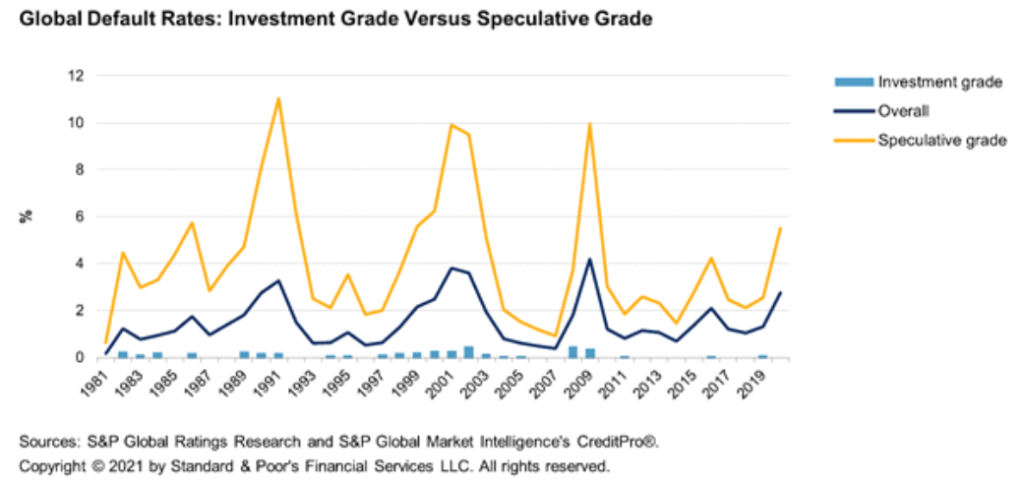

Their relative safety is highlighted through the diagram below, where default rates for IG issuers are very low, barely registering on the chart.

This is a result of debt servicing costs being at all-time lows (due to lower market interest rates), and the high credit quality of IG issuers.

When considering the risk of IG issuers, we can look at the Australian market where the largest issuers are the 4 major banks, who are highly unlikely to ever default given their world-leading capital ratios and implicit government guarantees should they ever be in a situation where they may default.

How Have Credit Spreads Performed Throughout The COVID-19 Pandemic

Despite the COVID-19 pandemic severely impacting the earnings profiles of many companies, credit spreads have tightened to near record lows – driven by accommodative monetary policy.

This is in part due to the favourable funding environment, where liquidity has significantly increased, and issuers are able to tap the funding market at size, and at record low rates.

For many corporates, this means that they have been able to lock in future funding requirements at rates below what they may have previously been able to issue at – strengthening their balance sheets and subsequently reducing the level of credit risk.

The strong performance of credit spreads is highlighted through the Mason Stevens Credit Fund, which has been able to deliver a 1-year return of 6.81% despite a declining interest rate environment.

The Fund primarily derives its return from relative movements in IG credit spreads, whilst taking minimal interest rate exposure.

As such, the Fund has been relatively unaffected by interest rate volatility, unlike other bond funds which derive more of their return from interest rate movements and those which invest into government bonds.

How Much Does Their Influence Spread?

Credit spreads often act as a leading indicator for market cycles, with fixed income investors generally focusing on more holistic elements of companies than equity investors.

Where equity investors may only focus on cash flow generating parts of a company, fixed income investors examine all facets, and most importantly, levels of indebtedness and the ability of these companies to service and repay these debts.

As such, fixed-income investors are generally better suited to sign a warning alarm should signals turn to the negative.

This is reflected through a widening of credit spreads – where investors demand a higher return for taking on credit risk.

Tapering and Credit Spreads

Both the Federal Reserve and the ECB have indicated that they will begin to consider tapering their asset purchase programs (bond-buying) within their September or October meetings, with the RBA likely to follow such a decision given the ramifications of a divergence in policy action against more influential global central banks.

The resulting increase in both short and long-term interest rates will have ramifications for fixed income investors, however, the effect it will have on credit spreads, in particular, is yet to be determined.

Fixed-income investors seeking to hedge out interest rate risk can elect to invest into floating-rate bonds – given the coupons of these bonds are not fixed and reset periodically (i.e. quarterly) at a specific credit spread above their respective benchmark (which are then linked to central bank interest rates).

Fixed-rate bonds are subject to interest rate volatility, with their capital prices decreasing with an increase in interest rates given the relatively lower rates of return these coupons would deliver when compared to other floating rate securities.

Credit Where Credit Is Due

Credit spreads carry significant relevance across asset classes – given their ability to indicate the health of corporate issuers.

Therefore, a knowledge of credit spreads and their dynamics are essential to those investors wishing to gain a holistic understanding of financial markets.

Moreover, as credit becomes a larger asset allocation within portfolios for the increased income and yield relative to government bonds, a working knowledge of credit bonds and their credit spreads will allow investors to assess the idiosyncratic risk/return profile of bonds, whilst still targeting income levels that are considered appropriate with investor return objectives.

As with most asset classes, policy actions look likely to be the most important catalyst in the coming years.

Upcoming central bank tapering will play a role in determining the trajectory of credit spreads, however, it looks unlikely that investment-grade issuers (particularly higher-grade issuers) will be affected.

The views expressed in this article are the views of the stated author as at the date published and are subject to change based on markets and other conditions. Past performance is not a reliable indicator of future performance. Mason Stevens is only providing general advice in providing this information. You should consider this information, along with all your other investments and strategies when assessing the appropriateness of the information to your individual circumstances. Mason Stevens and its associates and their respective directors and other staff each declare that they may hold interests in securities and/or earn fees or other benefits from transactions arising as a result of information contained in this article.