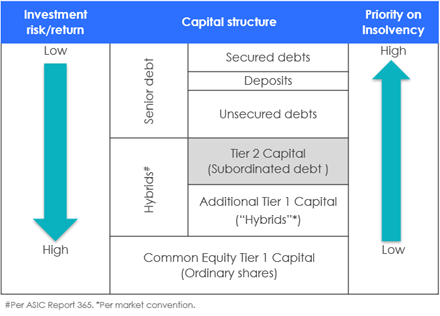

Banks and Insurers are funded by groups of distinct groups. The bondholders with the least chance of not being repaid should a bank get into difficulty are usually those earning the lowest returns and those with the highest likelihood of suffering a loss usually earn the highest returns. Australian banks typically fund themselves by offering the following in order from least to most risky:

- Deposits under 250k (insured under a Federal Government scheme)

- Covered Bonds (Issued in the Wholesale market with recourse both to the Bank and a pool of assets)

- Deposits greater than 250k

- Senior Wholesale Debt

- Subordinated Debt

- Junior Subordinated Additional Tier 1 or Hybrid Debt

- Common Equity

The Capital Structure from lowest risk to highest risk is shown below:

Banks can benefit from issuing Hybrid AT1 debt because it is treated as equity by their regulators meaning they are under less pressure to issue ordinary shares to fund balance sheet growth. In terms of cost of capital, AT1 hybrids can be significantly more efficient for a bank than issuing shares. In recent years as the Hybrid market in Australia has progressed banks have been able to buy back ordinary shares and partially replace them in their capital base with Hybrids.

For many investors the listed hybrid market is a convenient way of deploying cash where the borrower is a familiar issuer and the market for the debt is visible. The familiarity with this asset class is widespread which means even more than other types of debt securities this tends to trade quite homogenously. When investors are looking to buy, pricing is extremely tight and when liquidity is at a premium it can be very difficult to sell at spreads that are attractive.

Listed Hybrids issued by Australian Banks and Insurers in Australia tend to rely on franking for a portion of their returns. They can deliver franking credits to their noteholders because in a credit hierarchy they are the lowest ranked of all bank debt, however rank above common equity should the bank fail.

As the franking credits can take up to 22 months to be repaid by a tax refund (a coupon earned in July by a taxpayer who uses an Agent and lodges in the May following the end of the tax year on June 30), that delay may be relevant and could have a time value of money cost.

Hybrid Debt issued by the 4 Major Australian Banks meet a BBB-/Baa3 ratings threshold (S&P/Moody’s) but are not usually specifically rated as they are intended for retail investors. Other Australian hybrid issuance would not typically meet an investment grade threshold.

The increased uncertainty and volatility in equity markets combined with a significant increase in the RBA cash rate has seen investors increase their weighting to Fixed Income securities. Because of the limited Fixed Income securities readily available to most retail investors, much of this money was invested in listed Hybrids which saw a period where a number of these securities were trading comparatively tighter than other parts of the capital stack.

These spreads widened after recent events at Credit Suisse where US$17bil of AT1 debt was written off as it caused investors to reassess their risk premium for this part of the capital stack. In a rather unprecedented event, their AT1s were written off while common equity survived (even if it did receive a significant haircut) as the Swiss regulator stepped in to ensure financial stability. This brought into question the loss absorption hierarchy as Tier 1 debt is supposed to be converted to equity if the trigger ratio is reached and equity should be written off before AT1s.

Many central banks were quick to reassure investors that AT1s were behind common equity when losses occurred, but this did not prevent a widening of spreads in these securities. Whilst the hope is that this is an isolated event, it still highlighted the additional risks associated with this bottom rung of the capital stack. For this reason, many investors are looking one rung above at Subordinated or T2 debt.

It is worth nothing however that while Australian AT1s have been swept up in this selling, the securities in Australia have a few key points of difference. For starters the capital requirement ratios are considerably higher than Basel requirements with CET1 capital requirement set at 10.25%. For ADI’s they also contain a capital trigger and Australian instruments can allow for partial conversion.

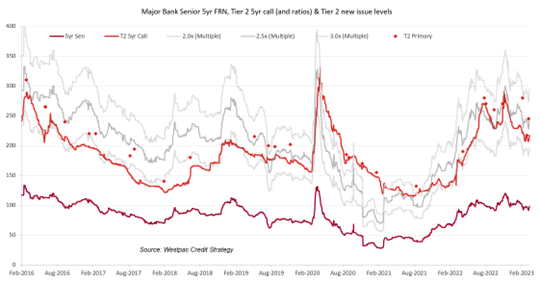

Tier 2 Subordinated debt is important for banks because regulators have determined that the senior debtors of a bank need to have a certain amount of subordinated stakeholders who would absorb losses before they do. These ratios are set based on the size of the banks’ total balance sheets and consequently need to be reissued on a regular basis. The amount of T2 on issuance is expected to rise for Australian Banks over the next 3-5 years.

Subordinated T2 bonds are typically issued into the wholesale markets but are more widely available after they have been on issue for 1 year. They do not rely on include franking credits as a portion of investor returns and are usually rated 2 notches higher than the Hybrid debt. In the case of the Major Banks this is BBB+/Baa1, comfortably investment grade. Although these bonds could suffer losses before senior debtors, the threshold for them to do so is higher than for Hybrids, however the margins they command can be quite similar. T2 debt credit spreads are most often issued at 2-2.5x times the credit spread for the issuer’s similar maturity senior debt.

One of the features of T2 bonds is they are usually subject to an issuer call between 5 and 10 years from their legal maturity. The calls are usually exercised by the issuer because as the bonds near their maturity date the amount of subordination that the regulator allows for the issuer diminishes. As these bonds are usually at higher spreads than unsubordinated debt there is an economic incentive for the issuer to call whilst they still deliver the most benefit for them. In addition the market operates on the understanding that the calls will be executed in the normal course of business whilst accepting that in exceptional circumstances the call may be delayed or never executed.

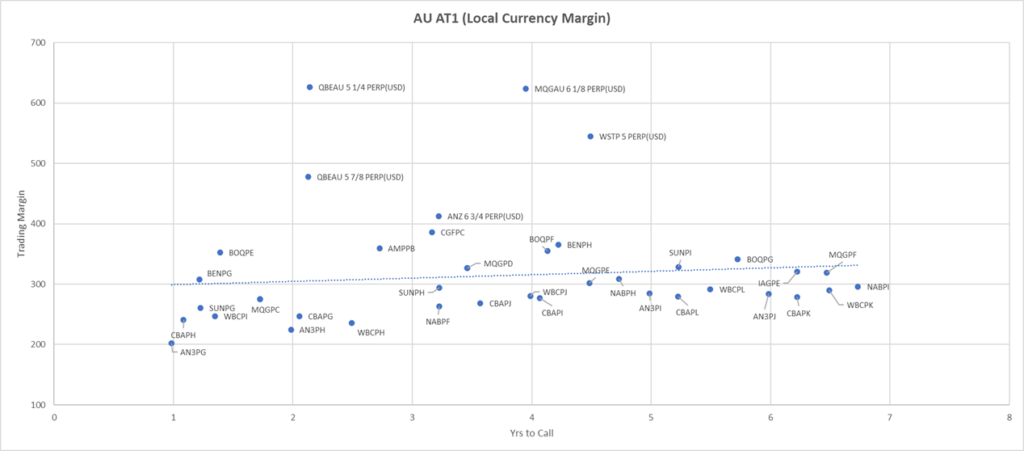

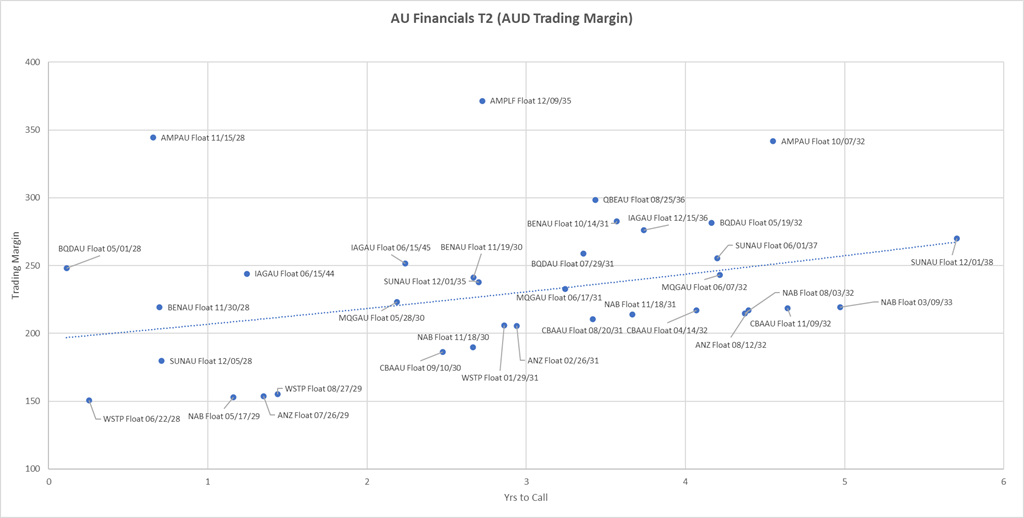

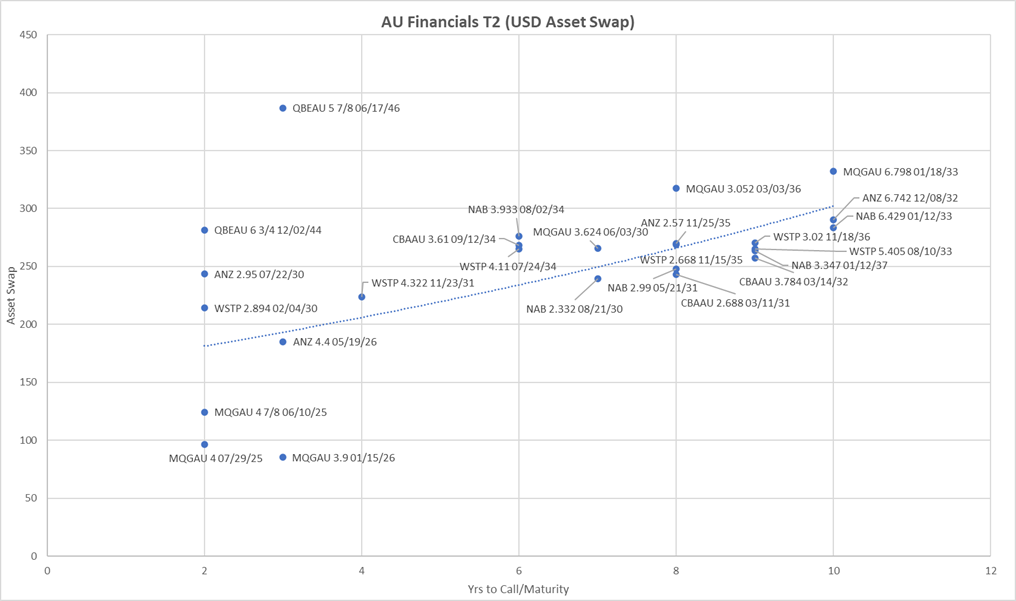

The charts below show the relative value of AUD AT1s and AUD and USD T2s.

The cheapest AT1s are currently the USD issues of QBE, Macquarie and Westpac, which were heavily sold off after the CS merger news with UBS.

The best value major bank AT1 in the listed hybrid space is the NABPH with a trading margin in the 300a.

Source: Mason Stevens, Bloomberg (As at 03/04/23)

The best value major bank T2 in AUD is the NAB Float 31 (Nov-26 call) with a trading margin in the 210a. Another name of interest includes QBE Float 36 (Aug-26) with a trading margin in the 300a for those that don’t necessary need a major bank.

Source: Mason Stevens, Bloomberg (As at 03/04/23)

Within Tier 2 (USD), the best value remains the QBE 5.875 46 (Jun-26) with an asset swap in the high 300s.

Source: Mason Stevens, Bloomberg (As at 03/04/23)

If you have interest in any of the above lines please don’t hesitate to contact us on bondorders@masonstevens.com.au.

The views expressed in this article are the views of the stated author as at the date published and are subject to change based on markets and other conditions. Past performance is not a reliable indicator of future performance. Mason Stevens is only providing general advice in providing this information. You should consider this information, along with all your other investments and strategies when assessing the appropriateness of the information to your individual circumstances. Mason Stevens and its associates and their respective directors and other staff each declare that they may hold interests in securities and/or earn fees or other benefits from transactions arising as a result of information contained in this article.