Yesterday morning, the US Federal Reserve’s Open Market Committee (FOMC) met and raised the US cash rate (called the Fed Funds Rate) from 0-0.25% to 0.25-0.50% – a target band rather than 1 specific interest rate.

The market had already priced in the 25bp hike, the first hike since December 2018, so there was no market reaction based on this news.

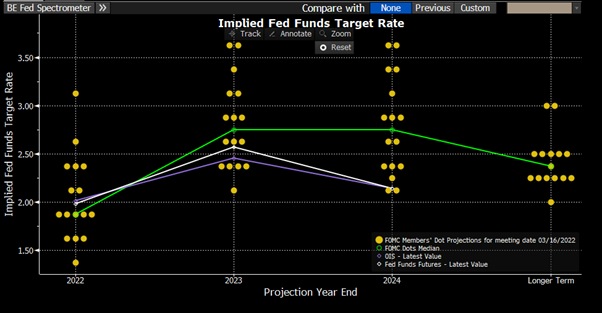

What did elicit a reaction, was the quarterly publication of the Committee member’s rate hike expectations – called the “dot plot” – which shows voting and non-voting Committee members’ latest views.

The dot plot was more hawkish than the market predicted, where the median dot is for another 6x25bp of rate hikes this year.

The way to read this chart is that each yellow dot is a FOMC member’s cash rate forecast, with the green line the median dot, and the purple line the current market pricing for the cash rate.

Chart 1: FOMC Dot Plot, with market cash rate pricing (purple line)

Source: Bloomberg, as at 17/March/2022

Because the purple line is below the green line from CY2023, it goes to show the Fed was more hawkish than market expectations, by ~25-50bp.

Furthermore, longer-run cash rate expectations of the FOMC are also higher than the market as well, which pushed US treasury bond yields higher.

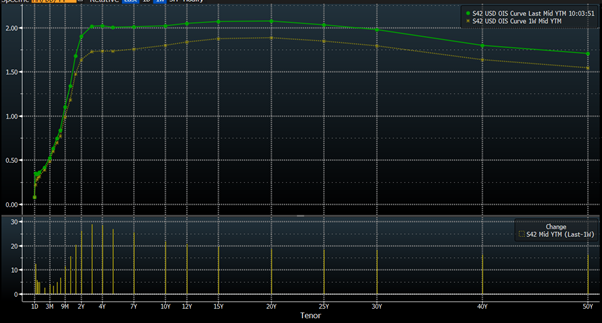

To highlight this move, we chart US rate hike expectations, where green line = current and yellow line = 1 week ago. Immediately after the FOMC meeting, 2-3y interest rate expectations jumped some 20-30bp higher.

Chart 2: US Cash Rate Expectations

Source: Bloomberg, as at 17/March/2022

Underlying Assumptions

The FOMC’s meeting statement noted that Russia’s invasion of Ukraine has added to inflation and will also weigh on economic growth.

As such, their economic forecasts were amended.

GDP is forecast to remain above trend through 2022-2023-2024 at 2.8, 2.2 and 2.0% p.a. respectively.

The US unemployment rate is forecast to remain around 3.5% throughout the 3-year forecast horizon, while growth is above trend, indicating that the Committee expects the participation rate to rise, providing more labour supply to meet demand.

I’d also surmise that there’s an expectation for surplus household savings to be spent over the time horizon as well, allowing GDP to grow above real income, which seems the only material way their economic growth forecasts can be as high as they are.

As for inflation; these were revised higher in the near term: 4.3% for 2022, 2.7% for 2023 and 2.3% for 2024.

Built into these views are the projected impact of Russia/Ukraine’s war, impacts on oil prices and global supply chains, though do not incorporate recent developments spawning from Chinese lockdowns of Shenzhen and Jilin.

Inflation Forecasts

The immediate thought that comes to mind now, in which we can compare their growth, inflation and cash rate forecasts, is that the FOMC are thinking the battle against inflation is going to take place this year up until the middle of CY2023 (hence the lower inflation forecasts), but they’ll still be continuing to raise rates even after that battle is projected to have been won.

This implies an outright contractionary policy bias, though inflation will be ever so slightly above their target (2.3% forecast against 2.0% target).

Likely, this has something to do with their switch to “average inflation targeting” in 2020, where the sample period for the average was never explicitly defined.

Actual Inflation

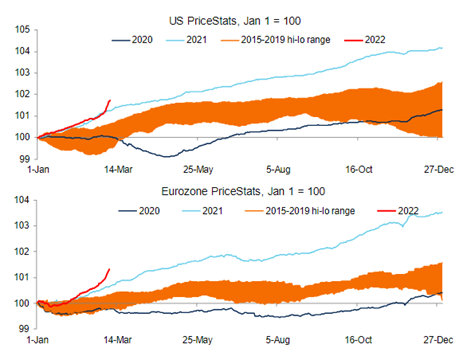

As for leading indicators for inflation such as PriceStats, the inflation measure is now starting to show the impact that surging oil prices has had since the Russia/Ukraine war began in February.

Before the invasion began, prices were tracking in line with 2021 levels, even before the 20% rise in oil prices, but now they’ve begun to surge higher.

Added onto this, we are yet to see the impact that spiking food prices will have on inflation, where wheat prices have risen >30% in the past fortnight.

Chart 3: US and Eurozone PriceStats Data – 2022 (red) spiking higher, above 2021 levels

Source: State Street Global Markets, PriceStats

Real Interest Rates

With this in mind, we can also contextualise the need for the Fed to keep raising rates past 2023 and into 2024, where their current – though higher – dot plot, may currently not be high enough.

Busting out one of my favourite charts to look at this year, we compare US 5y rate hike expectations versus 5y breakeven inflation expectations, our proxy for implied “real” policy levels (ex-ante of inflation).

The picture is clear, 5y cash rate expectations of 2.01% and 5y inflation expectations of 3.37% calculate real-interest rates still languishing at -1.36% p.a., very accommodative.

Top panel = 5y inflation expectations (red) vs 5y cash rate expectations (green).

Bottom panel = Difference.

Chart 4: US 5y Inflation Expectations vs US 5y Inflation Expectations

Source: Bloomberg, as at 17/March/2022

Fed Outlook

In the press conference held after the statement’s release, Fed Chair Powell fielded questions regarding the rate hikes, the chance of causing a recession given slower US growth, and financial markets factoring in higher borrowing costs.

Powell admitted a large swathe of factors are outside the Bank’s control, such as workers coming back to the labour force (and resulting productivity gains), as well as the ongoing nature of the pandemic and impact on spending habits, such as doing activities rather than buying products, which should assist stress on struggling supply chains.

On the topic of higher borrowing costs, Powell pointed out that higher inflation does typically lead to a slowdown in economic growth (called “demand destruction” as less people can buy the higher priced goods/services), but that US households would enter this scenario with stronger balance sheets as US household debt to disposable income ratios are at their lowest levels since 2001

Hence, implying that consumers have capacity to weather such an environment…

And that, “the probability of a recession within the next year is not particularly elevated.”

And that economic growth of 2.8% is still quite strong.

Walking a Fine Line

The Fed is walking a fine line, where they’re needing to raise interest rates to bring down forward looking inflation expectations, without crashing the US economy.

This is otherwise known as a “soft landing”, as opposed to a hard landing which would likely equal recession.

Thinking of this otherwise, the Fed’s going to keep tightening, quite likely in a predictable and slow manner once they get their cash rate to at least 1.5%, then tweaking it higher whilst not spooking the market and hurting economic activity.

This will be quite the balancing act with a higher chance of policy mistake – which is likely why the FOMC is keeping their options open and not fully committing to a Volcker-esque rate hiking cycle, a better term might be a “half Volcker”.

The views expressed in this article are the views of the stated author as at the date published and are subject to change based on markets and other conditions. Past performance is not a reliable indicator of future performance. Mason Stevens is only providing general advice in providing this information. You should consider this information, along with all your other investments and strategies when assessing the appropriateness of the information to your individual circumstances. Mason Stevens and its associates and their respective directors and other staff each declare that they may hold interests in securities and/or earn fees or other benefits from transactions arising as a result of information contained in this article.