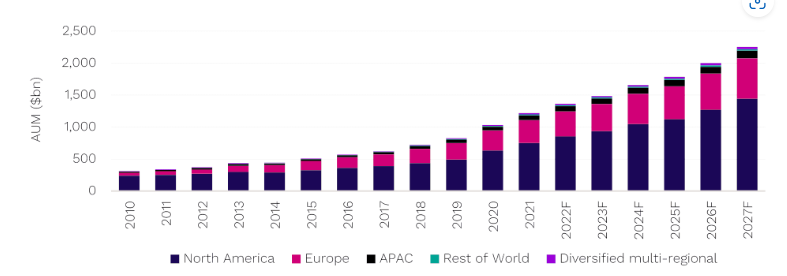

The Australian private credit market has continued to expand substantially, with estimates placing its value at approximately AUD $205 billion. We have seen a rapid growth in the number of domestic managers offering private credit funds, while many of the large US and European private credit managers have begun to establish a presence in the Wealth space. This growth has been accompanied typically by excellent risk adjusted returns that have been well above what has been available in public credit markets.

Private Credit Assets Under Management

Source: Preqin

At least in the short-term, however, this golden run has had a question mark put on it. At the end of February ASIC released a discussion paper1 on the dynamics of public and private markets, with comment on the need for greater surveillance of Private Credit offerings, particularly with regards governance, valuations, and conflicts of interest. At the end of March ASIC then asked 20 private credit managers to provide more details on their valuation policies. In the interim we saw a large licensee put a sell recommendation on the private credit funds on its APL, and a research house put the Private Credit as a sector on watch. What did all this mean and what should you be considering?

The first thing to highlight is that the issues that ASIC highlighted are very similar to what we highlighted in our Private Credit Sector Review that we published in May of 2023. In that report we highlighted the importance in this space of diversification, transparency, team experience, and good governance. Our recommendations at the time were for those managers that could clearly demonstrate these characteristics, and to be wary of strategies where some or all of these factors were lacking. This focus of ours remains, and all the managers on our High Conviction List (HCL) are those with strong, experienced teams, and highly diversified portfolios.

ASIC’s focus on this area is, in our view, a positive. Private Credit is a legitimate asset class that warrants a place in a diversified portfolio – no different in one sense to the rationale for allocating to Private Equity within the growth component of a multi asset portfolio. With the gold rush that has occurred in this space, however, there has in our view inevitably been some lower quality entrants. The sooner this is cleaned up the better.

Key Categories of Private Credit

With the aforementioned growth in Private Credit, there is now a good range of strategies in the Wealth space in Australia across the major styles of private credit investing. The main segments to consider include –

Senior Secured Lending:

This type of loan is secured by a company’s most valuable assets, such as real estate, equipment, or receivables. Senior secured lenders have the first claim on these assets in the event of default. These loans are typically lower risk and therefore offer lower returns relative to other sub-sectors.

Mezzanine Debt:

Positioned between senior debt and equity, mezzanine debt provides higher returns but also comes with increased risk. These loans are typically unsecured or backed by lower-priority claims to the company’s assets. Mezzanine debt is often used by companies that are growing and need funding for expansion but cannot yet secure more traditional forms of financing.

Real Estate Debt:

This category involves financing for real estate projects, and is common in Australia, but less so with international offerings. These loans are often secured by the property itself. Real estate debt can be used for commercial or residential developments. There is a degree of sector risk that needs to be considered with any offering in this space.

Asset Backed Securities:

This involves lending to pools of particular asset types – most commonly mortgages, but also areas such as equipment leasing, auto loans, and receivables financing. These loans often have shorter durations and are typically secured by the underlying assets.

Distressed Debt:

Distressed debt investments involve buying debt from companies in financial trouble, usually at a discount. The manager will seek to profit from the company’s recovery and/or with the restructuring of its debt.

Private Credit in a Recession

What are the considerations if we do get a global recession, particularly one triggered or exacerbated by the current trade war and aggressive tariff regimes. To start with, it’s worth noting the best market environment for Private Credit would be one where interest rates stayed elevated because of strong economic growth. In this scenario the absolute yield remains high, and defaults remain low. In the case of a recession, we will likely see the opposite effects including –

Increased Default Risk – Some private credit portfolios that have high exposure to cyclical sectors (e.g., retail, manufacturing, transportation) are especially vulnerable. Furthermore, individual companies may be significantly affected by the specific disruptions that Trump’s tariffs and a trade war bring on.

Pressure on Collateral Values – A recession often leads to asset write-downs, impairing collateral that underpins many private credit deals (e.g., real estate, receivables, inventory).

Liquidity Deterioration – in the event of a deep recession, where there is broad based stress, private credit’s intrinsic illiquidity becomes a pronounced challenge.

These risks are not an argument to exit a Private Credit allocation, but rather to ensure that any allocation you do have is a high-quality, diversified strategy that can withstand an economic cycle. More specifically, it is worth reviewing that you are:

» Tilted toward more senior-secured strategies with stronger covenant protections.

» Have reduced exposure to cyclical or trade-sensitive borrowers.

» Increase allocation to managers with deep restructuring experience and active workout teams.

» Maintain greater liquidity buffers across the broader portfolio.

Private credit remains attractive on a relative basis—but the margin for error is narrowing in the current environment, and manager selection remains key.

Private Credit Review outcomes

Two years on from our last review we have expanded the list of Private Credit managers on our HCL. Domestically we remain focused on those managers with highly diversified portfolios, and well resourced and experienced teams. We now have 4 differentiated managers as well as a trade finance specialist. In terms of global private credit there has been a significant expansion of options available as many of the large US and European players have launched offerings in the local market. A number of these are high quality options with excellent track records overseas and we now have 3 differentiated managers on the HCL.

The main hurdle with the international options in many instances are the fees, with the total cost expected to be circa 3% p.a. once all fees are tallied in a number of instances. While the after fee returns are expected to meet objectives, it is nevertheless something of a barrier for cost conscious portfolios. The main culprit here is a hurdle of 5% for the performance fees as a standard in the US market. This hurdle rate may have been reasonable when interest rates were close to zero, but with running yields often up around 9-10% p.a., it is a very low bar, and one we believe should be changed by managers to reflect a more normalised rate environment.

- https://asic.gov.au/regulatory-resources/find-a-document/reports/dp-australia-s-evolving-capital-markets-a-discussion-paper-on-the- dynamics-between-public-and-private-markets/ ↩︎

The views expressed in this article are the views of the stated author as at the date published and are subject to change based on markets and other conditions. Past performance is not a reliable indicator of future performance. Mason Stevens is only providing general advice in providing this information. You should consider this information, along with all your other investments and strategies when assessing the appropriateness of the information to your individual circumstances. Mason Stevens and its associates and their respective directors and other staff each declare that they may hold interests in securities and/or earn fees or other benefits from transactions arising as a result of information contained in this article.