Platforms: Learning the language

14 July 2025

Published by the Financial Standard

Article Contributor:

Vien Luong

Chief Platform Officer

Mason Stevens

With the advancement of artificial intelligence, it isn’t exactly surprising platforms have quickly adopted solutions. But what can we really expect from the technology – and what are the risks?

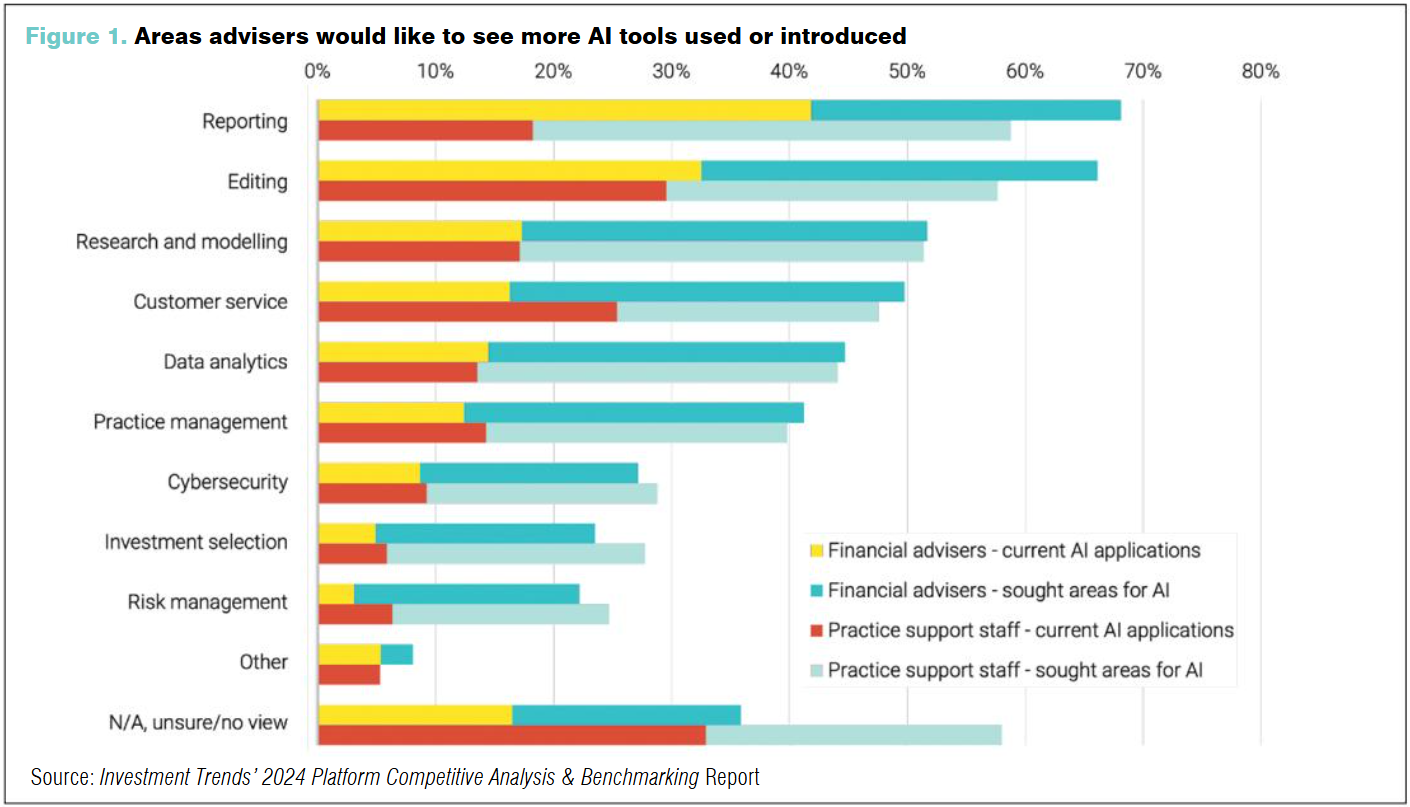

Artificial intelligence (AI) brings clear advantages across various channels, predominantly on platforms. Examples are seen throughout Investment Trends’ 2024 Annual Platform Benchmarking Report, showing that platforms are adopting AI to strengthen cybersecurity and fraud detection initiatives, machine learning capabilities, and portfolio review for better access insights.

Investment Trends finance and research director Paul McGivern highlights that technology can also streamline the documentation of client interviews, educate and train advisers on certain aspects, as well as create client report content and information retrievals, assist with software development, and more.

“In the 2024 report, we did include some Al-linked functionality, and the participating platforms gained additional points where they have implemented that functionality,” McGivern says (see Figure 1).

“Whilst the impact of Al functionality to their scores in 2024 was very limited, we do expect its importance to grow over the coming years.”

Although limited data may not demonstrate the true level of Al infiltration in the sector, DASH head of product adviser solutions Terri Ho says history has shown clear indications that those who are slow to adapt to the latest innovations will become the losers.

“History is pretty clear: in every wave of innovation – from electricity to the internet – businesses that moved either too slowly or too recklessly got left behind. The winners were those who made deliberate, strategic moves grounded in real use cases,” Ho says.

“With financial advice being highly regulated in the way information and advice is delivered to clients, basic use cases like using Al-powered tools for notetaking, meeting documentation, and client communications report saving over 10 hours per week on average. This equates to more than 500 hours per year.”

This also supplements a sector that is currently facing a critical shortage, with only 15,600 financial advisers active in Australia. Al can help in many ways, including playing a big part in digital advice for personalised advice as well as customer support.

However, with the abundance of merit comes the underlying threats Al also presents.

“Al is both the biggest threat and the biggest opportunity facing business today. The critical point: this isn’t a passing phase. The tension Al creates isn’t cyclical – it’s structural,” Ho continues.

“The real challenge is learning to operate within that tension and drawing crystal clear lines between where Al replaces us, where it augments human capability – and where we want to preserve and double down on the human elements of our business.

“Whether you’re excited by Al or wary about it, one truth cuts through: economics always wins. The moment a competitor uses AI to lower costs, boost efficiency, or elevate client ex-perience, the conversation shifts. It’s no longer about belief – it’s about economics.”

Holistic solutions

Many, if not most platforms currently used by Australia’s advisers are equipping themselves with the latest AI features.

Still, Mason Stevens chief platform officer Vien Luong says there are components of AI that remain insufficient.

Although the firm does leverage Al technologies to some extent, Mason Stevens prides itself on the fact that human interaction still edges over innovation, refusing to use any form of Al in the front office.

“When it comes to more principle-based or a grey area like regulation, Australia is very good at adopting principle-based regulation. Al technology today just isn’t able to provide holistic solutions for that segment, not yet,” Luong says.

“That’s one area I’d love to see advancements in because Mason Stevens’ philosophy here is ‘AI is not going to replace us’ – it is just going to enable and supercharge what we do.”

Mason Stevens operates as an investment platform and a deposit-taking institution that has a superannuation fund, meaning it is regulated by both ASIC and APRA – and that any use of Al must be stringently monitored.

“We are positioned in the market not only as a platform, but also as a provider of sophisticated investment services – not too dissimilar to an asset management business,” Luong explains.

“Hence, we use a lot of portfolio management and analytics tools internally, and the partners that we’ve used for that technology have rolled out certain AI features to help optimise those processes.”

Although Luong remains unsure about what Al regulation will look like in the future, he believes the firm’s “compliance-by-design” approach puts it in good stead.

“I don’t think anyone is sure where that’s [the regulation of AI across platforms] going to go for now. For us, it’s principle based. We as an organisation have a compliance-by-design mentality; everything we design, every solution we put in place, has a compliance lens – it is not just about ticking a box but to think through what regulations might be coming,” Luong explains.

“If we’re designing a solution, how do we future proof that, regardless of whether AI is involved or not.”

While Mason Stevens is looking to take a more considered approach, others are more gung-ho about capitalising on Al’s capabilities.

For example, Netwealth has overhauled several aspects of its business, following the adoption of Al tools in its platforms business.

“We’ve seen sound adoption and outcomes from Al already within the business and our contact and service area; we’ve implemented several significant Al projects, which have led to improved customer service, reductions in call waiting times, as well as broader efficiencies within the team,” Netwealth chief executive and managing director Matt Heine says.

“One [aspect] is around that back-office efficiency, and the other half is client-facing technology, where we can create new and different ways of interacting with the platform.

“Ultimately, the more that we can drive efficiency, increase accuracy, and also deliver better services to our customers, it’s a ‘win-win’ for everyone.” This includes a chatbot that Netwealth is planning to introduce, which has been in development over the past 12 to 18 months.

Netwealth has conducted rigorous testing and Heine says the chatbot, once introduced, will be able to handle well over half of all incoming enquiries before matters need to be shifted to a staff member. This would lift a considerable burden for employees whose time is spent answering and resolving simple issues.

“That’s really important from a chatbot perspective; we’ll be adopting a multi-layered approach, whereby we believe that moving forward, in the next two or three years the chatbot will be able to answer 60% to 70% of all inquiries,” Heine says.

“It’ll be able to answer a wide range of enquiries in real time with high levels of accuracy. However, we also recognise the importance of having the ability for customers to be triaged and directed to a human when help is needed. To make sure that we don’t end up frustrating our customers, we’ll be running AI sentiment analysis over the top of the chatbot interactions.”

Equally, Heine recognises that ethical overlays are critical, and notes that most of his employees are encouraged to learn how to use Al in some form.

“It can be difficult [to measure], because it is being adopted and used broadly across the whole business,” Heine adds.

“Some areas are getting much greater benefits earlier given the technologies that we’re working with however, we have a number of medium to longer-term projects and plans which I think will deliver very significant benefits.

“Whilst AI definitely isn’t the solution for everything… it’s supporting more and more automation as well as better customer experiences.”

Legacy troubles

It’s prudent to consider that not every platform is suited to ride the Al wave; sometimes, they may already be too heavily equipped to properly integrate new capabilities in a timely manner.

Avoiding this issue, Elemnta chief executive Shaun Green explains that younger companies are typically on the front foot, compared to their older counterparts, because they often have the right systems in place from the get-go.

“Our work with many financial services institutions highlights how legacy data systems, or stacks, are not ready for the full benefits of AI,” Green says.

“… due to legacy, some more mature institutions don’t have the data foundations in place to allow them to truly leverage the power of Al. They often need help to create clean, better organised, standardised data to deploy Al benefits, and it’s the core foundational integrations work that we are assisting them with.

“I can’t emphasise enough that the back-end data infrastructure inside a platform or institution should be the priority focal point when seeking to unravel historic technology systems built over previous time horizons and at different levels of cognisance regarding the power of properly integrated data.”

This also applies to consumer-focused platforms like Pearler, as it was able to incorporate the latest technologies during establishment.

“We’ve built on the most modern tech stacks available. So, Al has enabled our engineering team to increase our efficiency,” Pearler cofounder Nick Nicolaides says.

“As a modern company, I wouldn’t say that Al has had a material impact yet on back office, because everything in our back office is fairly automated and digital to begin with.

“Within our business, at every level, Al is already driving decision making and it’s not [about] us tearing everything down to insert AI; it’s involved in every decision, whether it’s re-sourcing, recruiting… and particularly how we are investing marketing budgets.”

As a trading platform, Nicolaides reiterates Al isn’t a “magical black box” for the best investment decisions but a catalyst in searching the most suitable content to learn.

“Rather than focusing on how someone can use Al to pick investments or manage money, we’re [understanding and testing] how it can cut down the decision-making process around how to utilise features like automation, optimising for saving rates, investment frequency, and more,” Nicolaides says.

The trading platform is orientated towards younger Australians that tend to be more self-directed.

“Al is putting itself in between that person and the endless world of general content such as blogs, videos, how-to guides, courses, forums, and more,” Nicolaides explains.

“Al is dramatically simplifying and speeding up a person’s ability to find the content… we don’t see Al as creating a new type of content, because people are already happy and used to existing content.

“Al is enabling people to find the content that’s most relevant for them… a young, self-directed person that wants to learn, wants to be hen in control and isn’t looking for this magic black box to tell them what to do.”

Al also assists Pearler in search engine optimisation (SEO) and organic forms of distribution, but for material impact he believes the industry needs to wait-and-see how the true benefits are going to play out as business continues to grow.

Detecting threats

As with any other software rollout, it is imperative to understand the strengths, weaknesses and risk factors of implementing AI tools.

Ho says some key risks can include the lack of transparency, security concerns and misinformation and manipulation.

“The rapid growth of AI does mean that laws and policies have not yet quite caught up with not providing proper legal frameworks,” Ho warns.

“As such when implementing Al, part of the strategic solution would be to incorporate strict policies around the use of Al, including developing guidelines for responsible use such as vetting AI tools and outlining which tools can be used, how they are used, and steps to protecting confidential data.

“Ensuring the risks are well understood is also key, with one of the main risks being trusting Al too much and over-relying on its outputs, hence overlaying its use with a review framework would help manage risks.”

Cybersecurity is also paramount.

According to Green, Al is commonly used to detect security threats.

“Our approach to managing security is, in a lot of cases, to use AI tools that help in the identification of threats. For example, anyone who’s housing data, important information or financial transactions are literally constantly defending against attempts to break into their environment,” he says.

It is a similar practice at Mason Stevens, where Luong also says AI is an integral guardrail in keeping data safe.

The firm outsources most of its AI capability to third-party service providers, as it aims to leverage mature technologies instead of inventing from scratch.

“There are a lot of Al or technology providers out there and we use a composition of our technology stack from a number of different providers. They aren’t Al specialists, per se, however most technology companies are now researching and developing Al technologies within their existing suite of products,” Luong says.

Its use in scams is also growing.

Green recalls a recent phone call where it took nearly eight minutes for him to realise he actually wasn’t talking to a human.

“It felt a little weird because I hadn’t been able to identify that it was AI; I thought it was a human,” he says.

“… you can see the power of it on what’s going on [with Al] – the rate of advancement of Al technology is faster than any technology in history, there’s no tapering off, which often is the case.”

The lack of disclosure around the use of AI could also prove problematic, and as features like chatbots become more common, examples like Green’s phone call will likely become more common.

Ultimately, the use of AI must be treated with caution, keeping an eye on, and ready to adapt to, any future regulation that may emerge.

“Use of Al to assist advisers in areas such as asset allocation and alignment of client portfolios within managed accounts is likely to have a growing level of importance in future years,” McGivern says.

“Whilst we didn’t see any specific examples of Al impacting advisers use of managed accounts in 2024, we do expect the increased adoption of AI to filter through to many areas of platform functionality.”

Unsure about the future, McGivern believes any changes to platform functionality because of Al, especially those exposed to personal information and investments, will attract regulatory attention.

“We are only just beginning to see the impact of Al in the lives of advisers and in the functionality of platforms. But driven by adviser demand we expect the retail platform market in Australia to be one of the most dynamic areas in investment markets,” McGivern says.

“We are very positive about the future for advisers, their clients and the platform market, and we look forward to showcasing Al’s adoption into platform functionality both now and into the future.”