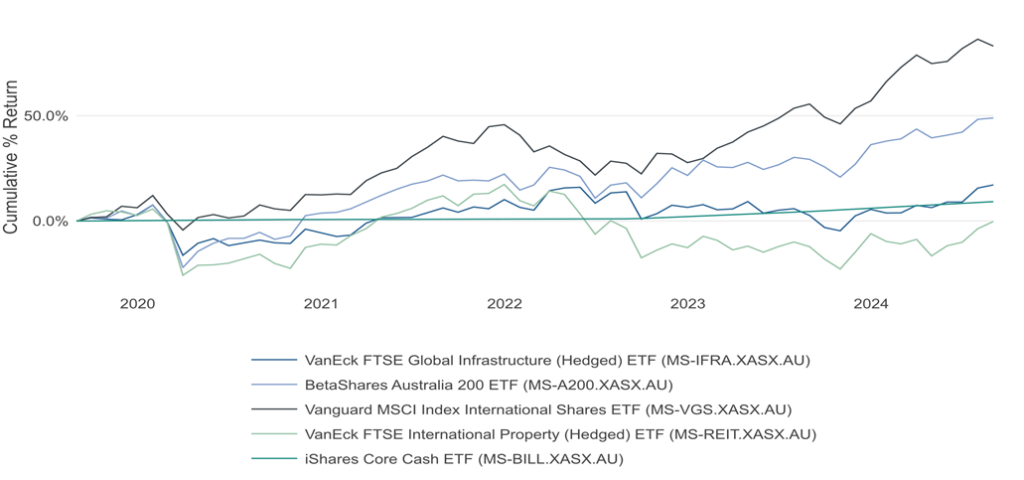

It has been a tough five years for both listed and unlisted Property and Infrastructure markets. The spike in inflation coming out of the pandemic and the subsequent steep interest rate hiking cycle led to a historically deep bear market in bonds, which in turn has had a major impact on those growth assets often viewed as bond proxies – in particular Property. Infrastructure, conversely, performed well on a relative basis in 2022 during the bond bear market, partly because of the direct CPI link for much of the income coming from Infrastructure assets. Either side of 2022, however, Infrastructure has struggled to keep up with strongly rallying equity markets. We can see this reflected in charts 1 and 2 below. Global REITS have had a slightly negative return over 5 years, and Global Listed Infrastructure has only slightly outperformed cash and has significantly underperformed equities.

Charts 1 and 2: 5 Year Underperformance of Global REITs and Listed Infrastructure Against Equities

Source: Mason Stevens OCIO, Jacobi Analytics, Morningstar

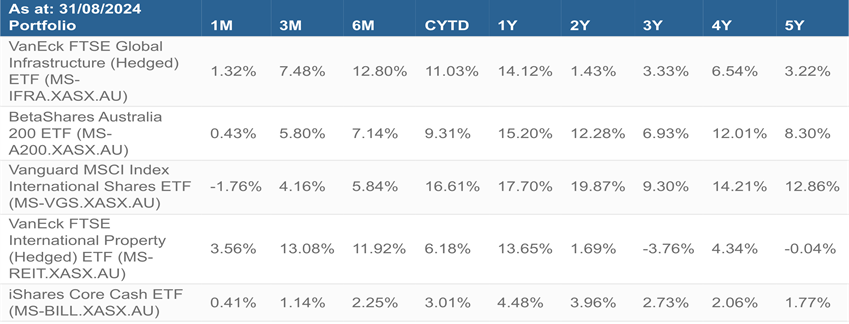

While there was a large correction in GREITS in 2022, direct asset valuations were not hit as immediately, but by 2023 significant write-downs in valuations begun to occur, as seen below in Chart 3, closing the gap between listed and unlisted market valuations.

Chart 3: Australian Direct Property Performance

Source: Lonsec

As we sit here in the second half of 2024, a key question is whether the large correction and/or period of underperformance for Property and Infrastructure is now over. With long term bond yields having fallen circa 100 bps in the past year, and many central banks having begun to cut interest rates, a case can be made that the worst is over and the forward-looking returns for these asset classes appear far more positive. In listed markets we are seeing that reflected in REITs and Listed Infrastructure, which have meaningfully outperformed equities in the past six months through to the end of August 2024.

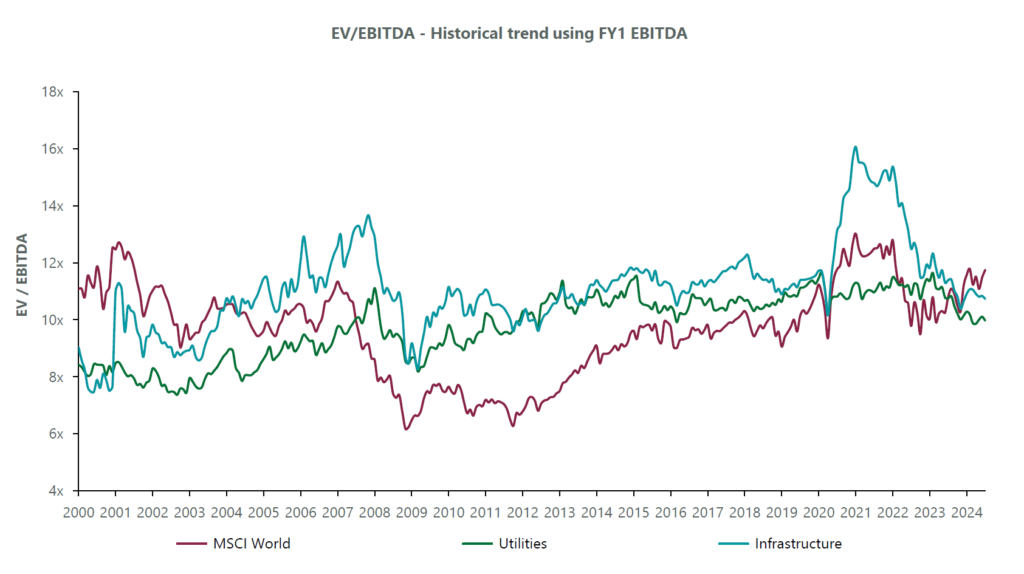

In considering the outlook, an important starting point is that these listed markets still look relatively inexpensive. Chart 4 below is a comparison of Infrastructure, Utilities, and the MSCI World on an EV/EBITDA basis. The MSCI World is currently dearer than both Utilities and Infrastructure, and the last time we saw that was in the early 2000s during the dotcom bubble.

Chart 4: Performance Comparison of Infrastructure, Utilities and MSCI World

Source: Clearbridge

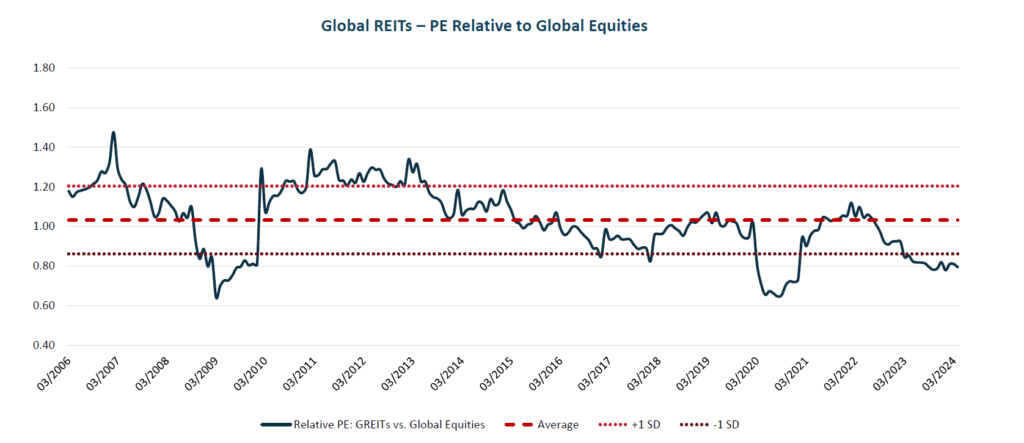

When we look at GREITS we see a similar story. Given the rally in the past 6 months, we have perhaps seen the market bottom already, but importantly they still look inexpensive vs Global Equities on a relative PE basis as shown below –

Source: Resolution Capital, UBS Research

When we look at direct Property and Infrastructure markets, we see a similar story, albeit with the lag to listed marks that is typical for direct assets. Unlike listed exposures, there has been no meaningful upturn up to this point, however there are early signs that we may be reaching something of a bottom. The NCREIF property index has been negative for the last 7 quarters (comprised of private commercial real estate properties held for investment purposes in the US). This is a longer downturn than the GFC, when this index was down for 6 quarters. This current quarter, however, may end up being the first positive quarter in almost 2 years, with the first two months having been positive as highlighted in Chart 5 below.

Chart 5: NCREIF Property Index Performance

Source: NCREIF

Across the board we can see that Property and Infrastructure look inexpensive at present, reflective of the 5 years of underperformance we have seen. These inexpensive valuations combined with a turn in the interest rate cycle present a real opportunity across real assets over the medium-long term.

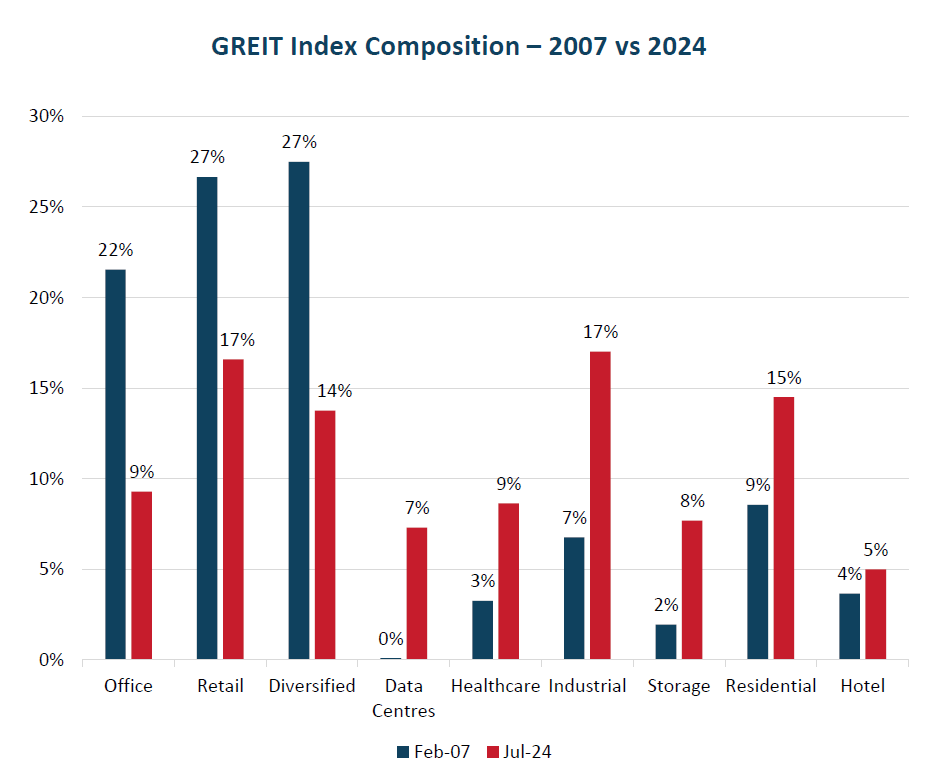

There are, of course, risks to this likely recovery in the near term. The possibility of recession in the US and in Australia in the next 6-12 months remains a key consideration. Relatedly, any economic downturn may put additional pressure on a troubled sector like office, which continues to be the most challenged space across Property and Infrastructure. It’s hard to find optimists for the office sector generally, given office occupancy is set to stay structurally lower post pandemic. Views typically range from a slow, grinding, rebasing of valuations, through to more bearish views on an additional downward spiral. While these assets look cheaper than they have in a long time, there remains the possibility of another leg down in valuations if we get a cyclical recession. With that said it’s important to put Office into context within the asset class, where it has gone from 22% of the index before the GFC to now less than 10%, meanwhile sectors like Industrial, Healthcare, and Data Centres have become much more important components as highlighted below –

Source: FTSE/EPRA, Factset

An investment in GREITS in 2024 does not have the office exposure it once did.

Choosing a Manager

If you’re allocating in this space, the good news, at least in listed markets, is that there is a small but consistent handful of managers adding value above and beyond passive options. Of ten well regarded GLI funds with track records in excess of 5 years, eight have outperformed the passive ETF option over 5 years. Similarly, of nine well regarded GREIT funds with a track record in excess of 5 years, all nine have outperformed the passive ETF option over 5 years. These two sectors are a great advertisement for the value of active management, particularly in areas where there is not a saturation of analyst coverage.

From a sector review perspective, this makes reviewing the managers easier in one sense, but also harder in another as you must make somewhat more nuanced, line ball decisions between managers that have obviously all added value over time. Nevertheless, we have identified the top managers for our High Conviction List on a go forward basis amongst a competitive field.

In terms of Direct Property and Infrastructure strategies, things become more challenging. The good news story is the increasing availability of Direct Infrastructure funds in the wealth space. This sector has typically been the preserve of institutional investors, or at best an allocation within a broader real assets fund. Now however, there are a small handful of capabilities that have come to market offering various forms of semi liquid structures (redemptions either monthly or quarterly) for the wealth space. We have identified one of these managers to add to our High Conviction List.

Direct Property is more challenged at present. There are several longstanding Direct Property funds that are having both performance and liquidity challenges. Performance challenges arise because of the already discussed valuation write-downs, then there are also strong liquidity demands as investors seek to exit an underperforming sector as well as re-orientate how they invest in property. The result is that there are very few evergreens, diversified property funds with strong track records that you could consider investing in at present. With that said we have identified one evergreen global property fund that has not been materially affected by any of the above issues, and provides clients with a high quality, diversified direct property exposure, and participation in the likely rebound in property in coming years. It’s worth noting also that there are some compelling opportunities in the wholesale, closed-ended space, as particular properties come to market, often having been sold at deep discounts by institutions because of these liquidity needs.

As highlighted above, we believe there is plenty of alpha available via managers in the Property and Infrastructure asset classes, particularly in the listed markets. As asset allocators, we now want the beta to come through to support overall portfolio returns. There are some encouraging signs, given valuations and the interest rate cycle, that the next 5 years will be far higher returning than the last 5 years.

If you are interested in finding out more, please contact your Relationship Manager.

The views expressed in this article are the views of the stated author as at the date published and are subject to change based on markets and other conditions. Past performance is not a reliable indicator of future performance. Mason Stevens is only providing general advice in providing this information. You should consider this information, along with all your other investments and strategies when assessing the appropriateness of the information to your individual circumstances. Mason Stevens and its associates and their respective directors and other staff each declare that they may hold interests in securities and/or earn fees or other benefits from transactions arising as a result of information contained in this article.